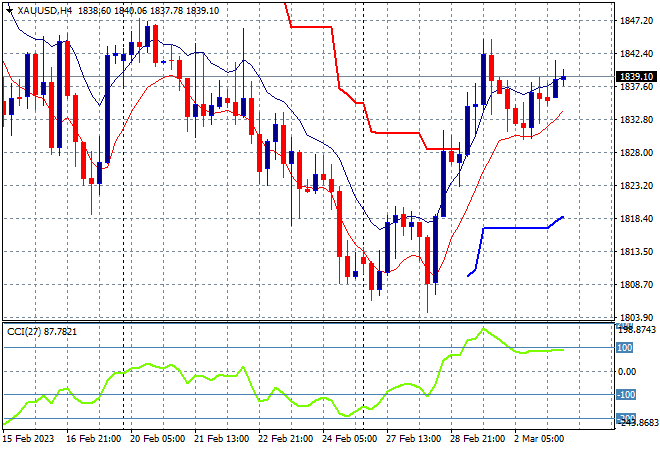

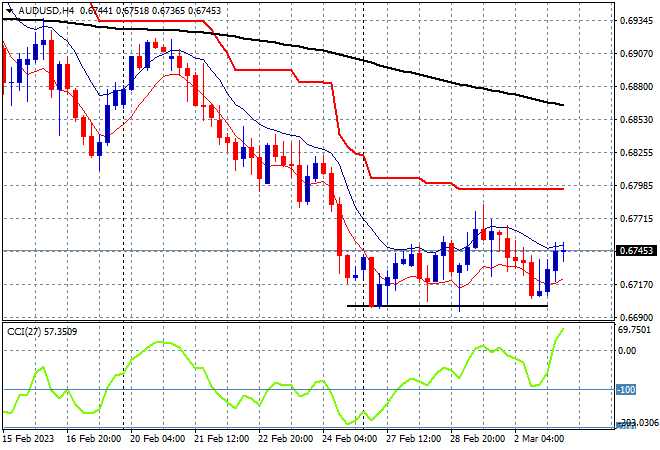

Asian stock markets are consolidating slightly higher across the region, with the real activity still in bond markets and as an aside, crypto with Bitcoin losing nearly 10% in afternoon trade. The somewhat solid lead on Wall Street overnight is being overshadowing by the continued selloff in bond markets which continue react to more hawkishness from both Fed and ECB talkfests. The Australian dollar has clawed back to the mid 67 cent level but remains in a weak state while oil prices are holding on to their overnight gains with Brent crude still above the $84USD per barrel. Gold has stabilised from its mid week surge, sitting just below the $1840USD per ounce level as it tries to get back to the previous weekly high:

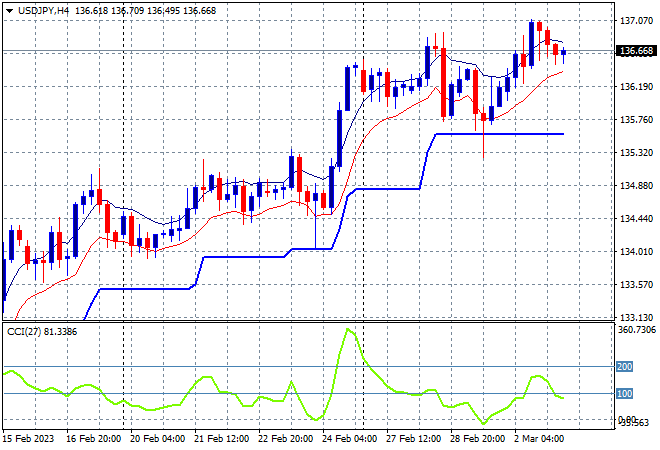

Mainland Chinese share markets are lifting slightly going into the close with the Shanghai Composite up 0.2% and still above the 3300 point barrier while the Hang Seng has rebounded from its previous loss, up nearly 0.8% to 20523 points. Japanese stock markets are soaring on the back of a strong employment print with the Nikkei 225 up more than 1.5% to 27949 points while the USDJPY pair has pulled back ever so slightly to be above the mid 136 level:

Australian stocks were finally able to put on some gains with the ASX200 closing 0.4% to remain above the 7200 point level at 7283 points. The Australian dollar is holding on to its meagre overnight gains in afternoon trade to almost reach the mid 67 cent level but is still nowhere out of trouble:

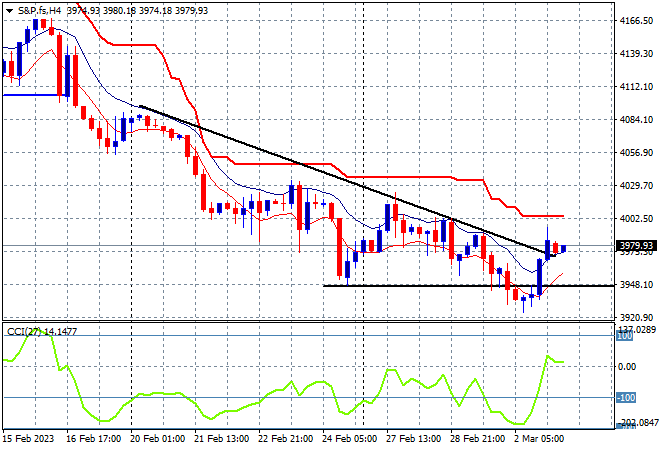

Eurostoxx and US futures are trying to hold on to their to pull back even further, with the S&P500 four hourly chart showing price action still trying to get back above the 4000 point level which remains a key resistance area. The possibility of a bottoming action is still forming here however:

The economic calendar finishes the trading week with a slew of PMI prints across Europe, culminating in the US services PMI plus quite a few Fed member speeches to keep an ear out for.