Below is an article I wrote for News.com.au:

Against the odds, Australian house prices are rising in the face of ongoing interest rate rises.

PropTrack’s dwelling values index recorded a 0.2 per cent rise in February, which followed January’s 0.1 per cent increase.

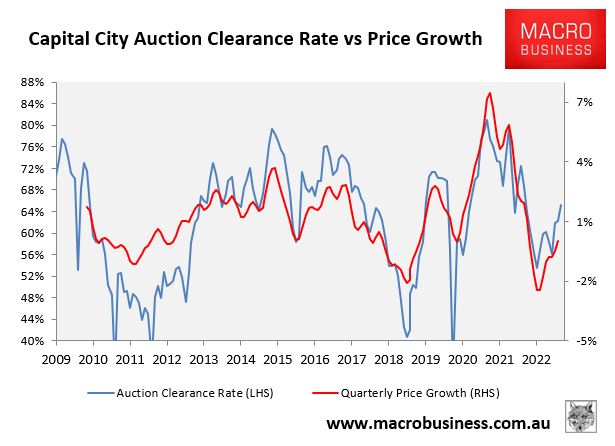

Based on the rebound in auction clearance rates this month, prices will increase again when March’s PropTrack results are released next week.

The rebound is extraordinary because it has arrived despite a 0.25 per cent interest rate hike in early February and another 0.25 per cent rise in early May.

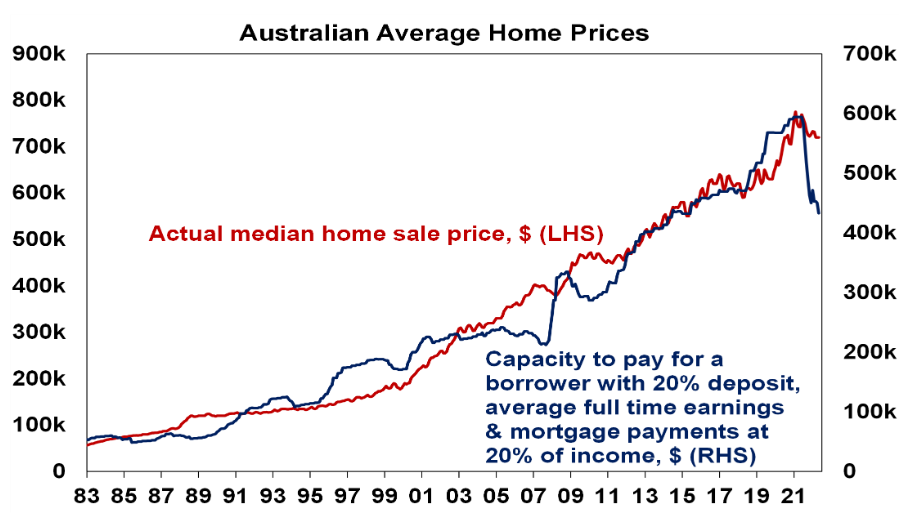

The 10 consecutive interest rate increases from the Reserve Bank of Australia (RBA) have roughly doubled mortgage rates and restricted borrowing capacity by around 30 per cent.

This represents the sharpest decline in borrowing capacity on record and would usually be associated with a significant fall in home values.

Why are Australian house prices rising?

An acute lack of listings, soaring rents, and record immigration are currently outweighing the RBA’s aggressive rate rises, driving the unexpected price rebound.

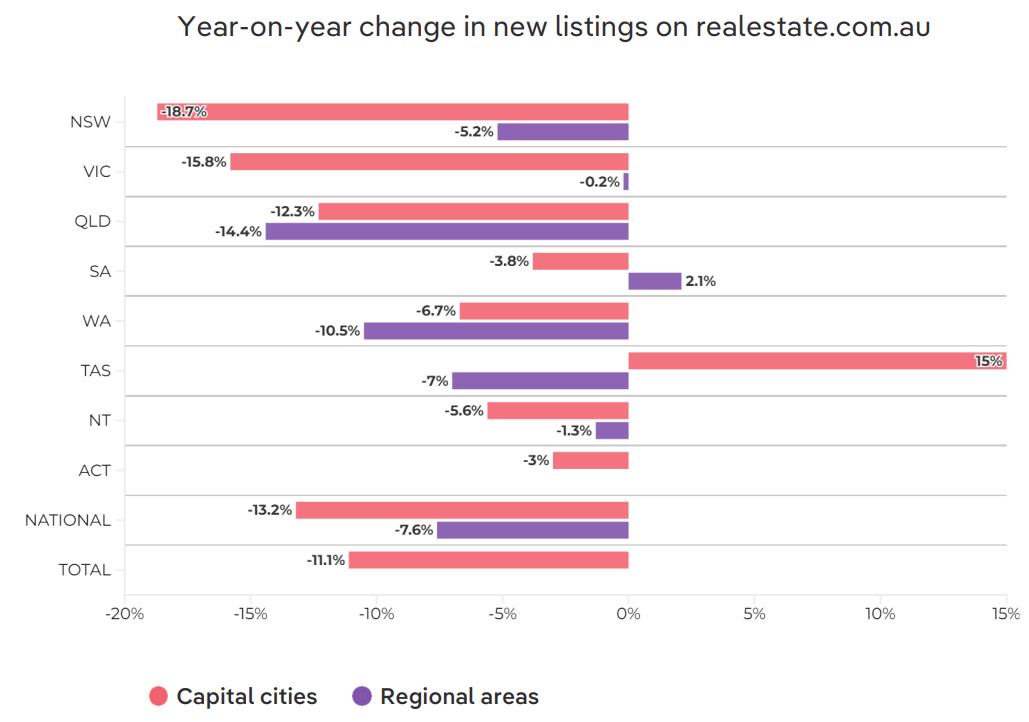

According to PropTrack, new listings were down 11.1 per cent nationally in the year to February, with the three largest capital cities experiencing the biggest declines in stock.

At the same time, rents across the combined capital cities are rising at double-digit rates amid record tight vacancies.

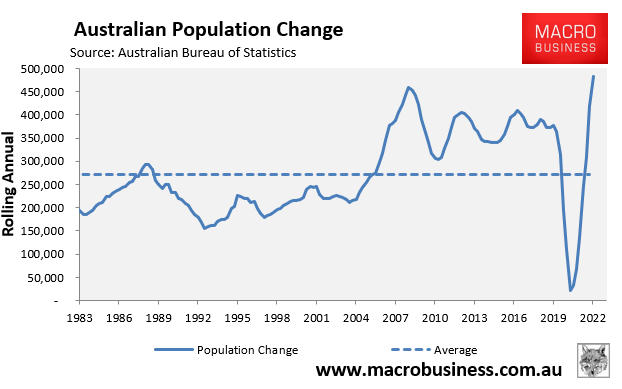

The market is likely to tighten further given net overseas migration is also running at record levels.

Australia’s population grew by an all-time high 482,000 in 2022, driven by net overseas migration of nearly 400,000 (also a record).

The early indications are that net overseas migration will surge even higher in 2023, given net temporary visa arrivals (excluding visitors) are booming on the back of unprecedented international student flows.

The above factors have created a ‘fear of missing out’ (FOMO) as Australians desperately try to escape the broken rental market.

A ‘dead cat’ bounce?

At the beginning of the month, I labelled the price rebound a ‘dead cat bounce’ and believed the home price correction will soon reassert itself.

This view was based primarily on the RBA’s uber hawkish commentary at its February monetary policy meeting, which flagged multiple rate hikes in the months ahead – a view that was supported by financial markets and most major banks.

Since then, the interest rate picture has changed amid the fallout from Silicon Valley Bank’s collapse.

Financial markets are now tipping no further rate hikes in the months ahead and cuts over the second half. Several major banks have followed suit.

The RBA has also adopted a more dovish tone in its commentary.

The upshot is that we are likely at or very close to the peak in the interest rate cycle, thus removing one major headwind for house prices.

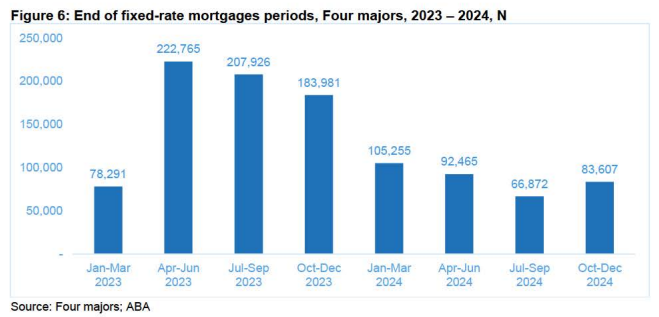

That said, a literal mountain of fixed rate mortgages will expire over the remainder of this year, which will see around 600,000 borrowers switch from rates of around 2 per cent to rates of between 5 per cent and 6 per cent.

The next chart from the Australian Bankers Association illustrates this fixed rate “mortgage cliff” as it pertains to the Big Four banks.

Around triple the number of mortgages will expire over the June quarter (222,800) than expired over the March quarter (78,300).

The September (208,000) and December (184,000) quarters will also see heavy volumes of fixed rate mortgage expiries.

Mortgage rates have already risen beyond 3 percentage points above the rates at which these fixed rate mortgages were originated, which is the minimum serviceability buffer required by APRA in assessing whether someone can repay their debt.

Therefore, a huge number of borrowers could be pulled deep underwater as their fixed rate mortgages expire.

This fixed rate “mortgage cliff” is, therefore, a material risk to Australia’s housing market and could see a material increase in forced sales that pull house prices lower.

House prices to boom in 2024

Whether the house price correction is genuinely over remains to be seen; although the signs are positive.

Regardless, 2024 is shaping up to be a boom for prices, given:

- The RBA is likely to cut interest rates, which would lift borrowing capacity;

- The Australian Prudential Regulatory Authority is likely to follow suit by reducing the 3 per cent mortgage buffer, which would further boost borrowing capacity;

- Australia will continue to experience rapid immigration;

- The rental market will tighten further; and

- Housing construction will be depressed, given high construction costs and widespread builder insolvencies.

There is genuine demand in the market. The only thing holding prices back is high mortgage rates and their impact on borrowing capacity.

Once that constraint is removed, you have the ingredients for the next house price boom.