How US financial crisis contagion reaches Australia

US regional banks are not stabilising:

Partly it is the bank run. But it is also this:

Upheaval across the global banking sector – from Silicon Valley to Zurich – has set alarm bells ringing on the stability of the global financial system and where the next area of weakness will emerge. Could commercial property, and in particular landmark office towers, be the next domino to fall?

Common to the challenges faced by both Silicon Valley Bank and Credit Suisse is their investment in long-dated bonds. Long-hold illiquid assets whose value has plummeted when marked-to-market: it’s a scenario which is familiar to the owners of commercial property including office towers, whose properties trade infrequently.

…If there’s a canary in the coal mine, a 17-storey office building standing prominently in Melbourne’s Docklands would be a candidate. It’s owned by industry super fund REST – among its tenants is Nine, the publisher of The Australian Financial Review – which offered it for sale with expectations of $490 million last year.

At 717 Bourke Street, the book value of the 42,000 square-metre building was in the order of $460 million when it was put up for grabs, industry sources say. The best offers came back around the $390 million mark. Rather than meeting the market, or at least closing the gap, REST withdrew the building from sale late last year.

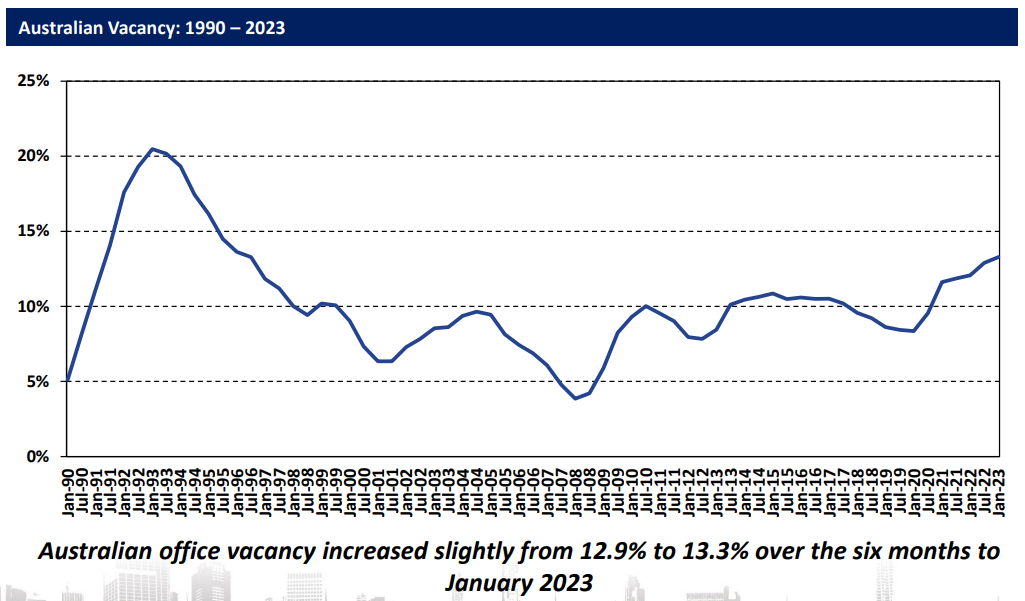

The office crash has been underway for several years and now it appears it is reaching critical mass in the US. All the signs are that Australian offices are in for it as well.

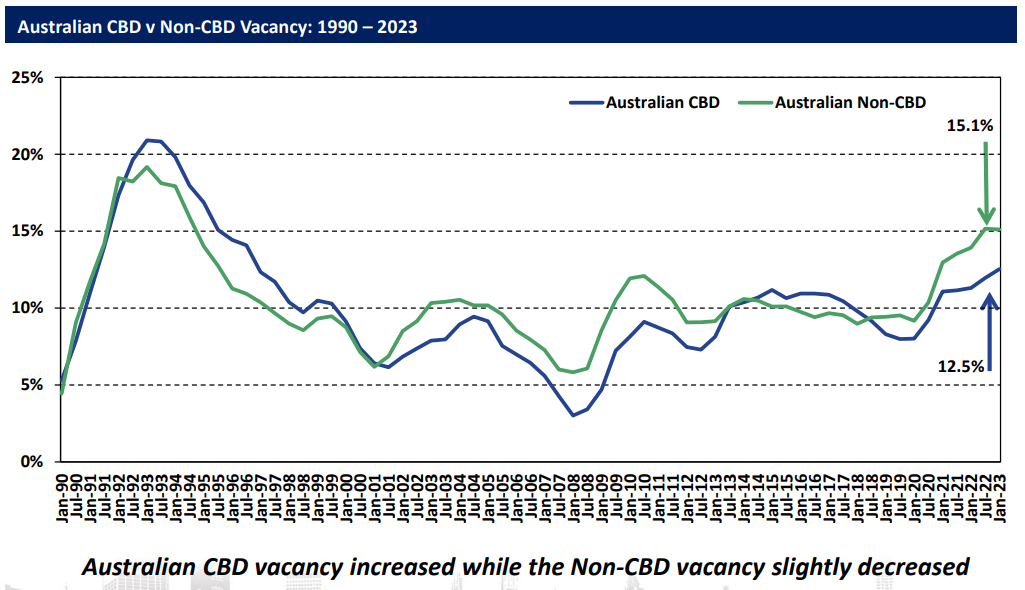

The obvious driver is work-from-home and vacancy rates are marching upward:

Everywhere:

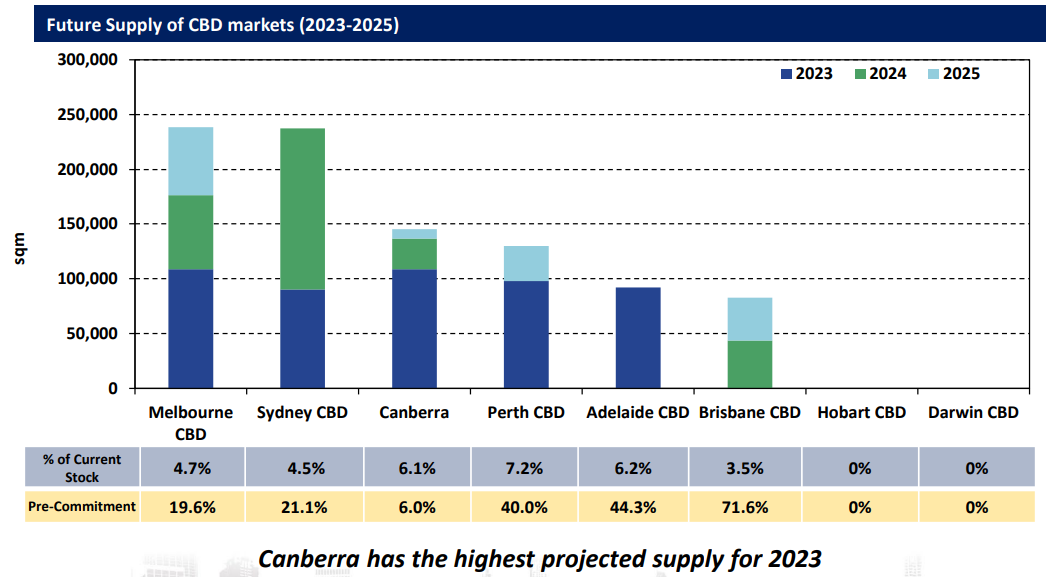

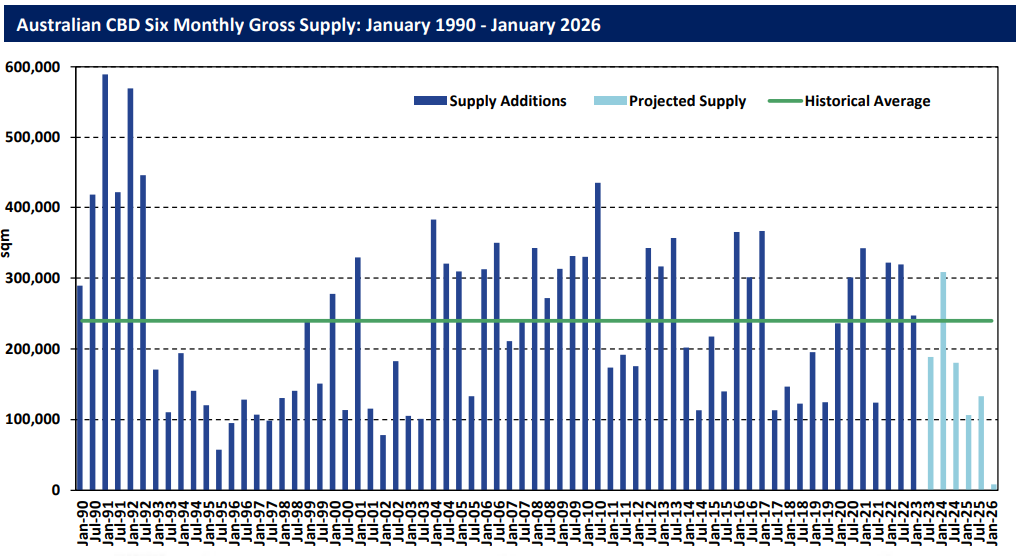

More supply is coming:

Who is exposed?

From the RBA’s last FSR:

Financial stability risks from weak leasing conditions in the retail and office sectors remain low, but would be expected to increase if economic conditions were to deteriorate substantially. The non-performing share of banks’ commercial property lending remains negligible and banks’ overall exposures remain low, at around 6 per cent of assets. Moreover, large listed Australian real estate investment trusts (A-REITs), which directly own around 60 per cent of retail shopping centre space and roughly 10 per cent of total office space, maintained healthy financial positions over the first half of 2022. Near-term increases in financing costs for A-REITs are likely to be manageable, as most have either fixed-rate debt or use interest-rate swaps to hedge interest rate exposure and only a small share of debt funding is due to roll off over the next year. While information on the financial health of smaller landlords is limited, liaison with banks suggests the vast majority of these borrowers will be able to meet higher debt payments, though some could struggle if their earnings were to decline significantly. Comprehensive information on the commercial property exposures of non-bank lenders is also not readily available, and so it is possible that impairment rates are higher in that part of the market.

Although declines in commercial property valuations are possible, risks to banks are contained.

Commercial property valuations are likely to decline in coming quarters given recent and prospective increases in interest rates; ongoing weakness in tenant demand in some segments could amplify the magnitude of falls. In this event, some leveraged investors in commercial property could realise sizeable losses. Some could be in breach of LVR covenants on their debt and, if they are unable to contribute more equity or renegotiate loan payment terms, could be forced to sell their properties. However, direct risks to the banking sector presently appear low.

The banking sector has significant protection against declining commercial property valuations, owing to their conservative credit policies. Commercial property loans typically have relatively low LVRs (less than 65 per cent) and impose a range of minimum requirements on borrowers’ debt-servicing capabilities (such as minimum ICRs and maximum debt-to-assets ratios). Moreover, banks’ direct exposures to commercial property are considerably lower than a few decades ago, when higher interest rates and an economic downturn last precipitated a large decline in the value of commercial property assets.

Whenever a central bank tells you a problem is “contained” it is time to worry. It is probably the case that the major banks have managed their commercial property books conservatively after the near-death experience of 1990.

But that means somebody else has been doing the lending. Non-banks and A-REITS are the local equivalents of US regional banks.

Somebody is going to blow up.