Goldman kicks us off with its usual best-case scenario.

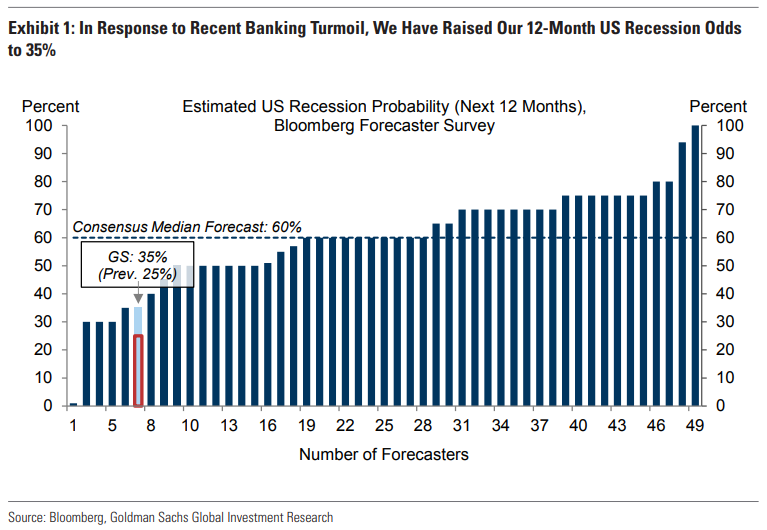

1. It is still too early to have a confident view on the implications of the current banking turmoil for the US economy. Our baseline expectation is that reduced credit availability will prove to be a headwind that helps the Fed keep growth below potential despite the support from rising real income and better global growth, not a hurricane that pushes the economy into recession and forces the Fed to ease aggressively. The risks are clearly skewed toward larger negative effects, and we have moved our subjective probability that the economy enters a recession in the next 12 months back up to 35% from 25%. However, this number remains well below the consensus of 60%.

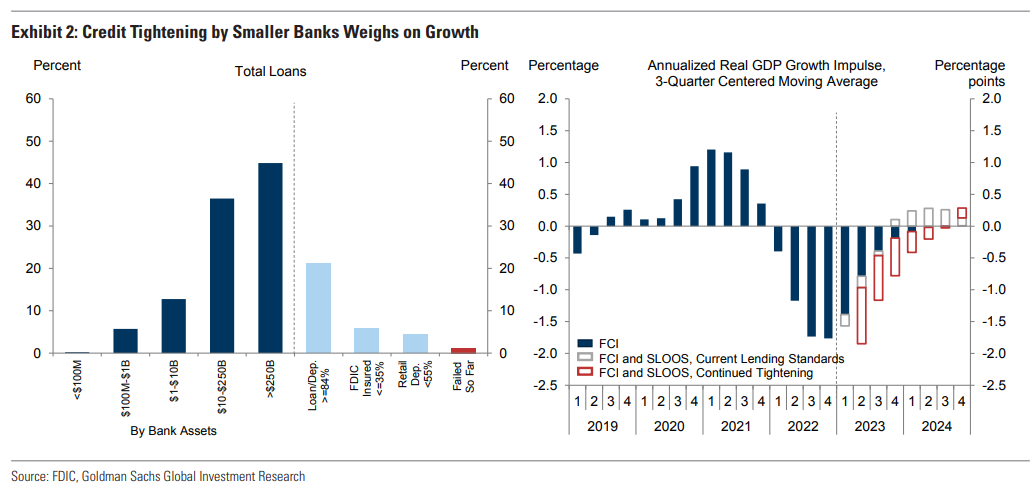

2. We have estimated the impact of tighter credit in three ways. The first is an accounting exercise that makes judgmental assumptions about new credit extension by banks with less than $250bn in assets and suggests a 0.25pp hit to growth. The second is an extension of our financial conditions impulse model that adds a role for bank lending standards and delivers a 0.5pp hit to growth. The third is a review of the academic literature on the effects of declines in both bank stock prices and accounting measures of equity capital on loan growth and GDP, which implies a 0.3-0.5pp hit to growth. On the back of these estimates, we have reduced our Q4/Q4 growth forecast by 0.4pp (from 1.5% to 1.1%).

The full text of this article is available to MacroBusiness subscribers