The 10 consecutive interest rate hikes from the Reserve Bank of Australia (RBA) are a double-edged sword for first home buyers.

On the one hand, borrowing capacity has shrunk by around one-third, which has made it far more difficult for first home buyers to purchase a home.

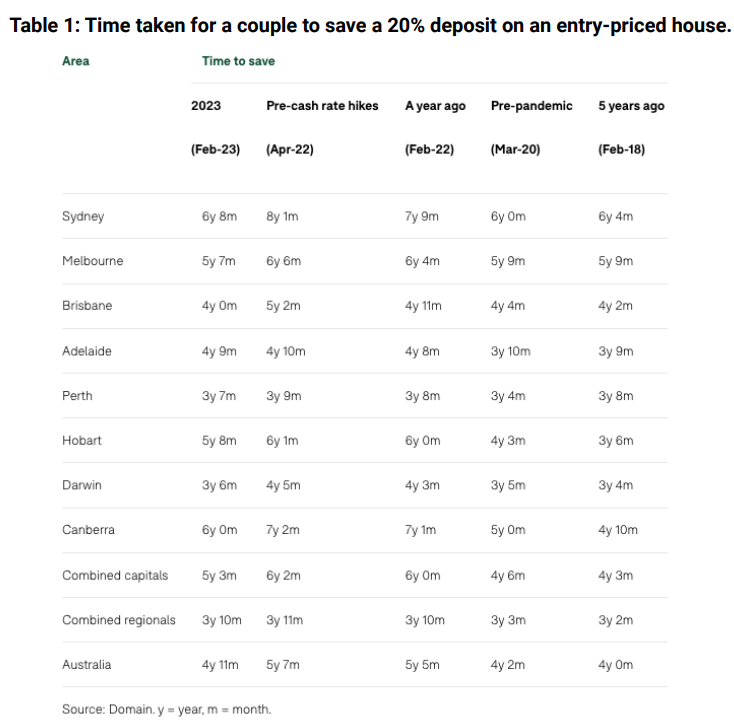

On the other, the circa 9% decline in national dwelling values has reduced the time needed to save a deposit by eight months nationally for houses, and by 13 months across Sydney, according to new data from Domain:

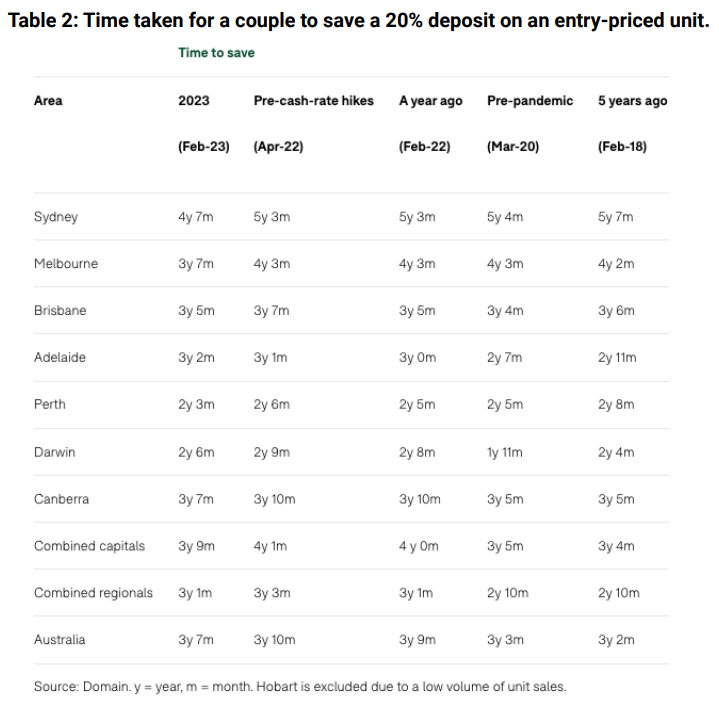

For units, the time taken to save a deposit has fallen by three months nationally and by eight months across Sydney:

Commenting on the result, Domain notes that “falling property prices in certain cities, higher interest rates accrued on savings and wage growth have aligned to reduce the time to save for an entry-priced property deposit”.

“Previously, rock-bottom interest rates greatly benefited mortgage holders, making it cheaper to borrow and repay a home loan. However, it was a key driver of property price growth, making time to save a deposit longer”.

“This narrative has flipped since the Reserve Bank of Australia embarked on one of the most aggressive rate hiking cycles in history, escalating the cash rate to over a decade high”.

“Now in 2023, first-home buyers are facing less competition and softer prices, reshaping the affordability conversation”, the report notes.

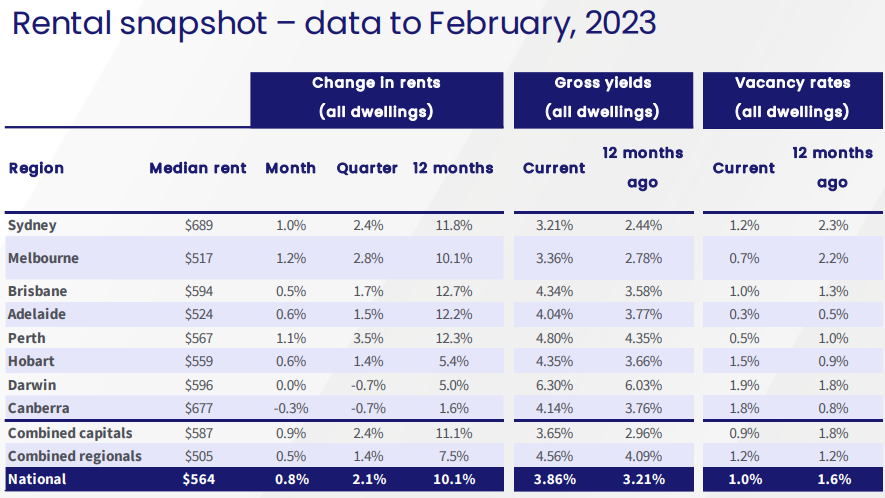

While the time taken to save a deposit has fallen, it is arguably more difficult for first home buyers to save for a deposit given rental costs are growing at a record pace:

Therefore, on balance the situation facing first home buyers is tougher, in my view, than it was a year ago.