Goldman with the details.

Bottom line:

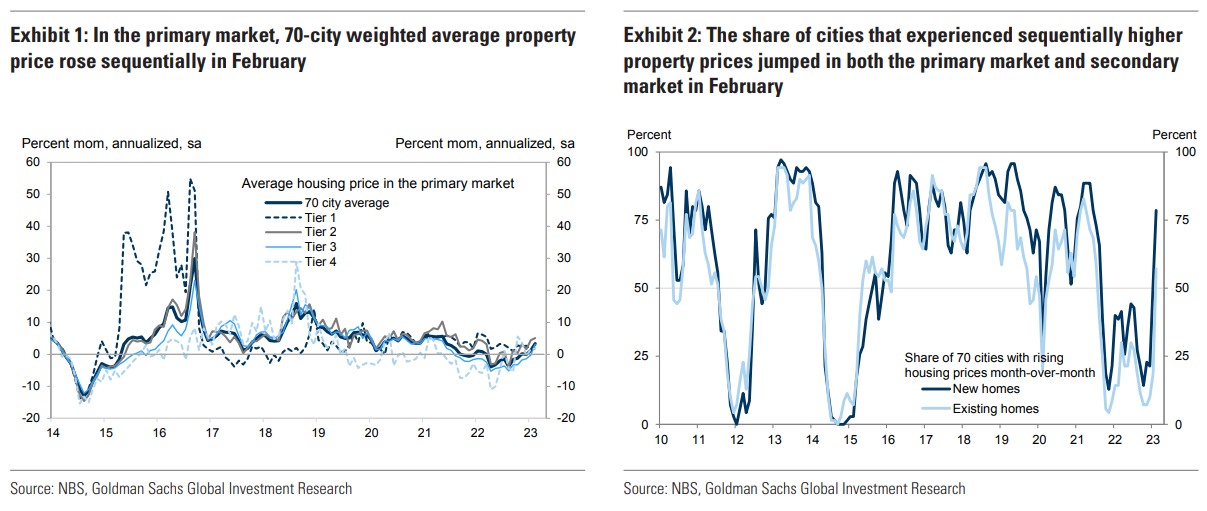

The National Bureau of Statistics’ 70-city house price data suggest the weighted average property price in the primary market rose sequentially in February after seasonal adjustments. The increase in house price was broad-based among all city tiers. The proportion of 70 cities that experienced sequentially higher property prices rose sharply in both the primary market and secondary market.

Key numbers:1 NBS’ 70-city primary-market weighted average property price change in February: +3.4% mom annualized (seasonally adjusted by GS), -1.0% yoy. January: +1.2% mom annualized, -1.3% yoy.

Main points:

1. After seasonal adjustments, weighted average house prices in the primary market rose by 3.4% mom annualized in February (vs. +1.2% in January; Exhibit 1), thanks to the improving property sales amid the ongoing government policy support. The proportion of cities that experienced sequential house price gains rose sharply in both the primary market and secondary market in February from January (Exhibit 2). Year-on-year change in weighted average new home prices edged up to -1.0% in February from -1.3% in January.

2. By city tiers, Tier-1 and Tier-2 cities continued to outperform, with house prices rising sequentially by 1.9% and 5.1% mom annualized in February (vs. +1.3% and +4.4% in January), respectively. House price also increased sequentially by 3.1% and 1.8% mom annualized in Tier-3 and Tier 4 cities (vs. -0.2% and +1.6% in January), respectively. Despite more local housing easing measures in recent months, we believe the property markets in lower-tier cities still face strong headwinds from weaker growth fundamentals than top-tier cities, including net population outflows and potential oversupply problems.

3. Under China’s new mortgage rate adjustment mechanism, cities that have experienced three consecutive months of new home price declines (in both month-on-month and year-on-year terms) are allowed to set mortgage rates for first-time home-buyers below the official floors. Based on our estimates, 9 cities in the NBS 70-city sample (12.9% of total) have met the conditions for setting below-floor mortgage rates as of February (vs. 21 cities, or 30.0% of total, in January; Exhibit 3).

4. Property-related activity data improved broadly in January-February, especially for new home sales and property sales. Our high frequency tracker suggests that 30-city new home transaction volume rose by 24.8% yoy month-to-date in March (vs. -13.0% in January-February). Major cities’ inventory months (sellable gross floor area divided by 12-month rolling gross floor area sold) rose to 24.4 in February from 23.5 in January, with the increase led mainly by Tier-1 cities.

5. Thanks to continued housing easing and solid credit supply, average interest rates on new mortgage loans moderated to 4.04% pa in February from 4.10% in January, the lowest data print since 2019, according to Beike’s estimates. February money and credit data also suggested growth of household medium-to-long term loans, which are mostly mortgages, improved somewhat in February, in line with improved property transactions. We expect more housing easing in the months ahead, but maintain our view that the property sector recovery should be gradual and bumpy, due to the challenging demographic trend, still-tight financing conditions for troubled developers and policymakers’ long-held stance that “housing is for living in, not for speculation”.

The question is: has the nexus between rising prices and wasteful construction been broken? Probably. The latest sales numbers for new property have softened:

Note that rebar steel production is VERY weak as well.

Could China adopt a new regime of rising house prices and falling construction to rebalance to consumption?

It’s been done before…