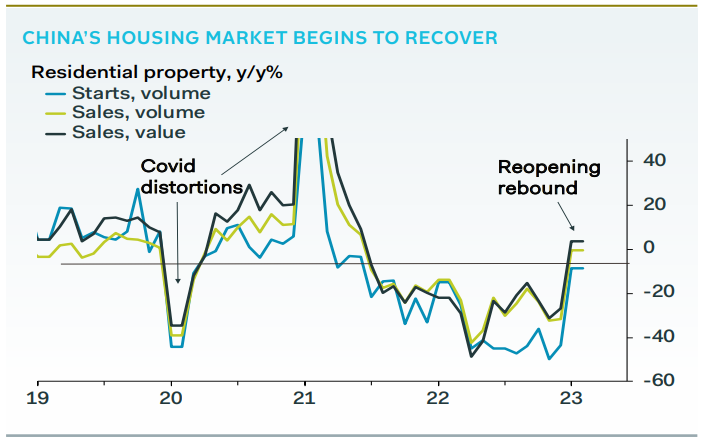

Pantheon with the note.

The two millstones around the neck of China’s housing market last year were zero-Covid policy and the dire state of developer finances. Since November, China has relaxed Covid restrictions and offered liquidity support to high-quality developers. Policymakers have also signalled that domestic demand expansion is the top policy priority this year, including property market stabilisation, alongside consumption and business investment growth. As a result, the housing market is beginning to recover. Home sales value rose 3.5% year-over-year in January/February, for the first time since mid-2021.

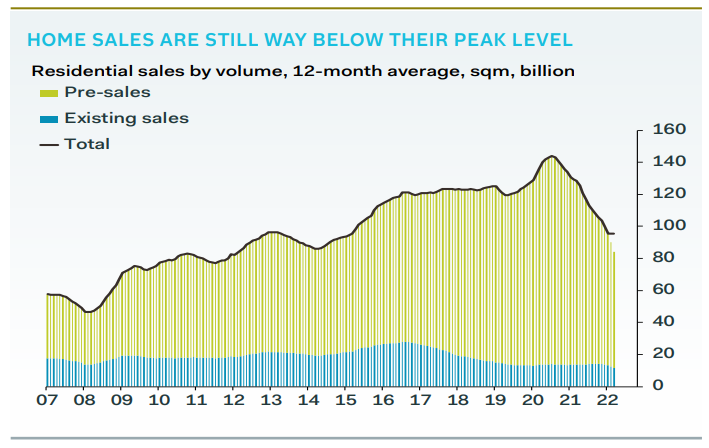

Home sales volume fell slightly, but is also on a clear recovery trend, as shown in the chart below. The volume of home sales is still way down from its peak, but the direction is positive. The national data mask vast variations across China’s 600-odd housing markets. Tier one and select tier two markets are likely to lead the recovery, owing to stronger demand conditions and little supply of land permitted for residential development. These cities are magnets for top graduates and skilled workers from across the country, leading to population growth.