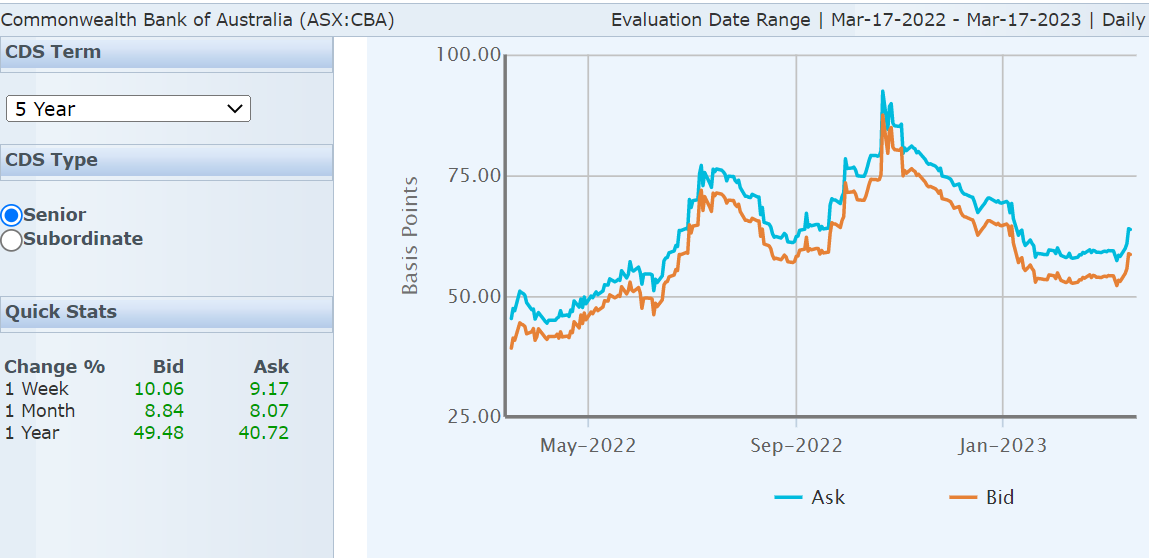

Is it any wonder? The US and European banking crises are coming to Australia via funding costs and collapsing commercial property. Followed by another blow as recession feeds back as bad loans:

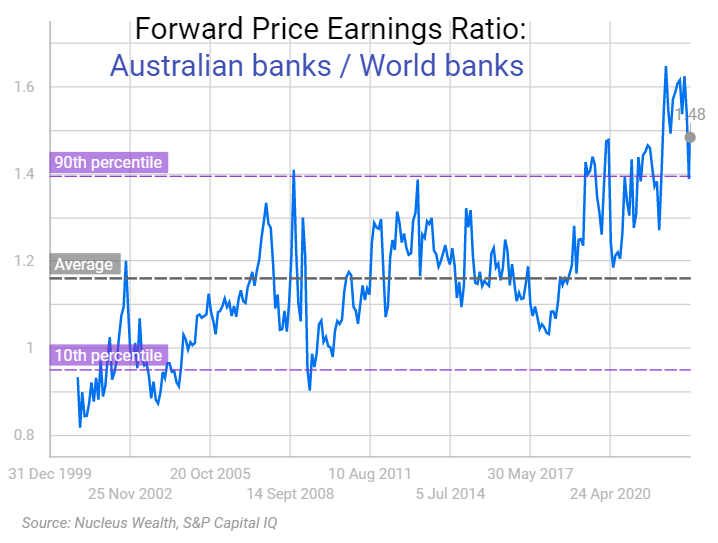

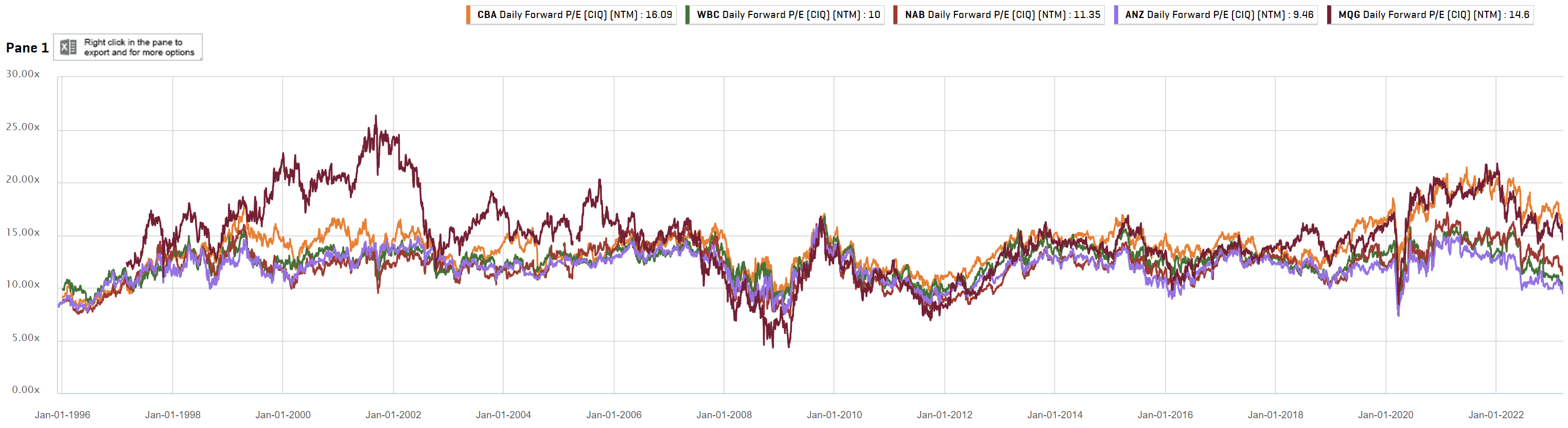

A global derating of banks is underway, and Aussie versions have some catching down to do:

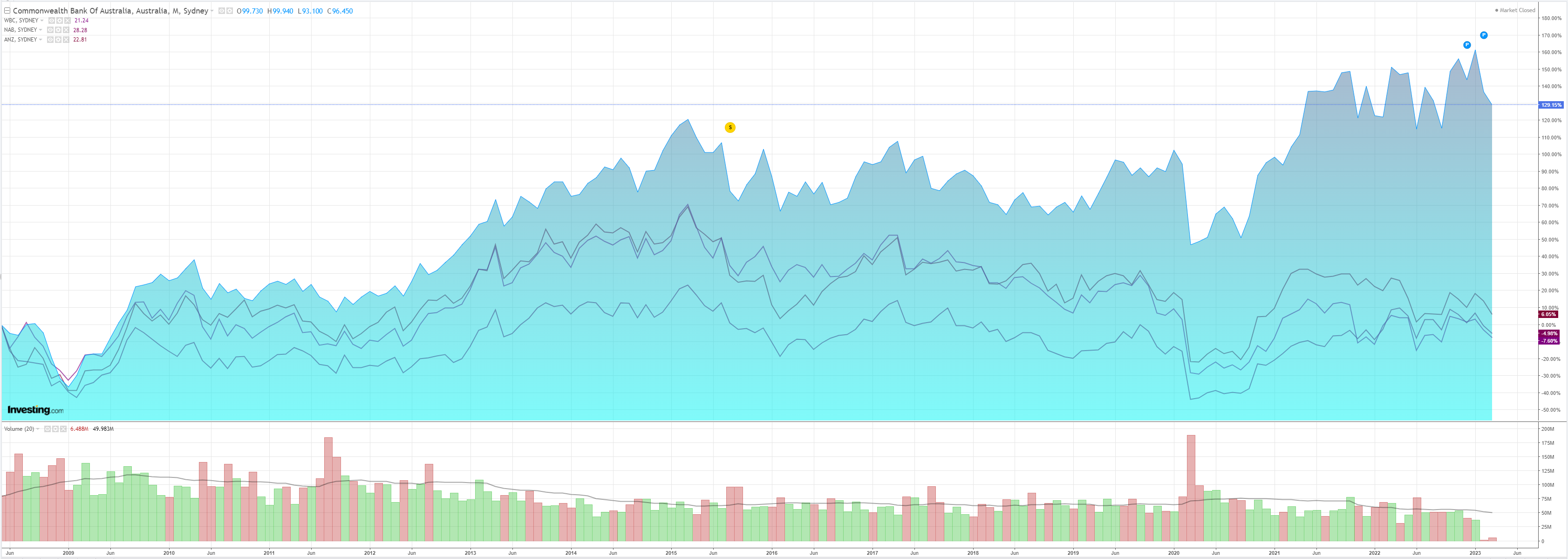

Of particular interest is the CBA which is driving so much of this bubble. Its price outperformance since the GFC has been startling:

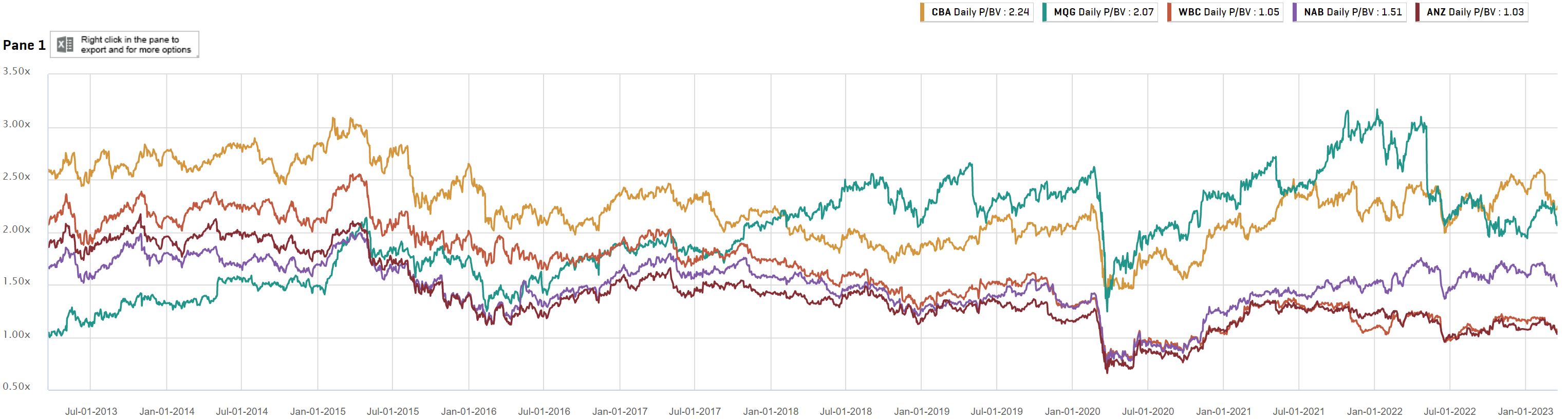

Which now has it worth more than double versus ANZ and WBC on a price/book basis:

One reason why appears to be that the market sees it as the only bank capable of competing with Macquarie as the latter morphs into a fifth mortgage monster. Perhaps there is a structural element in this:

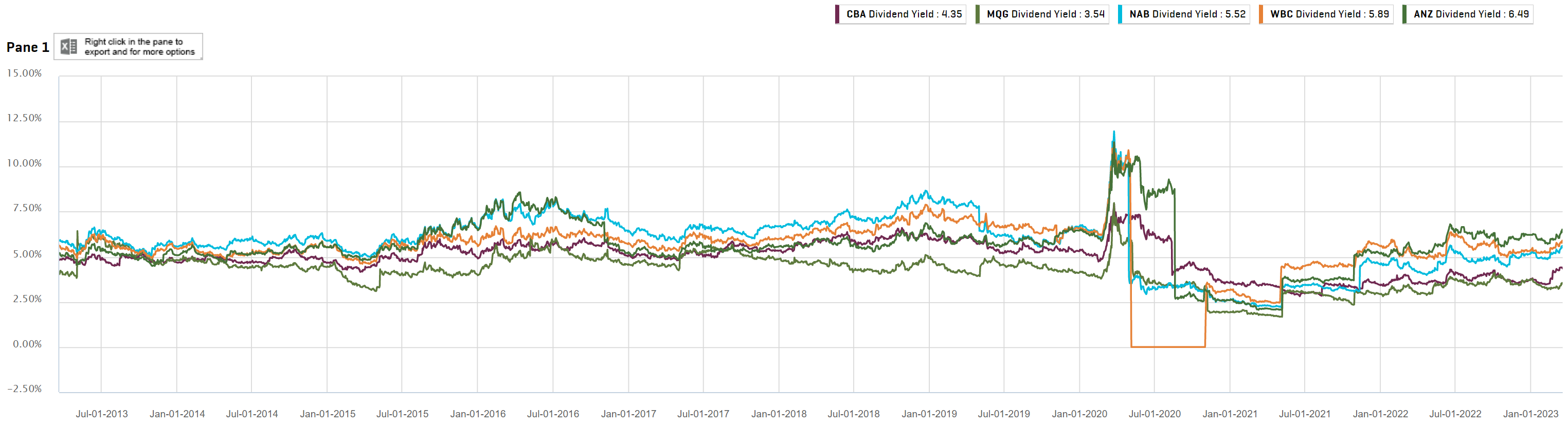

But does a 16x NTM make sense as the cycle comes to end? After all, you can currently get a zero-risk, higher-yielding term deposit at the CBA than you can from its dividend (unless you enjoy tax benefits):

The CBA bubble has some more popping to do.