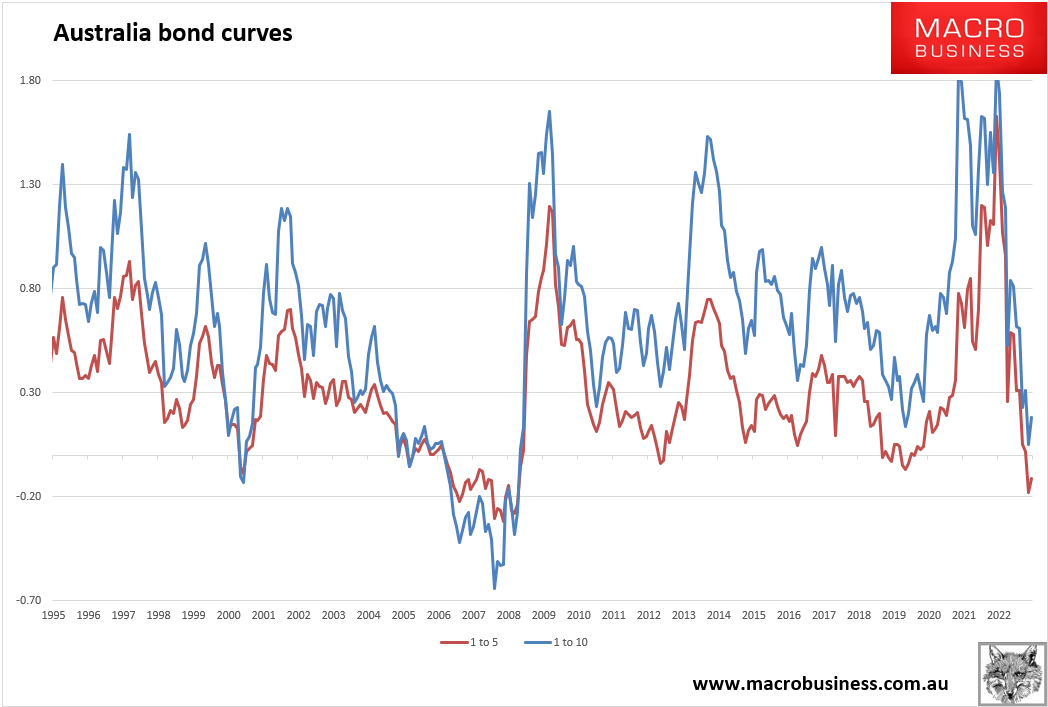

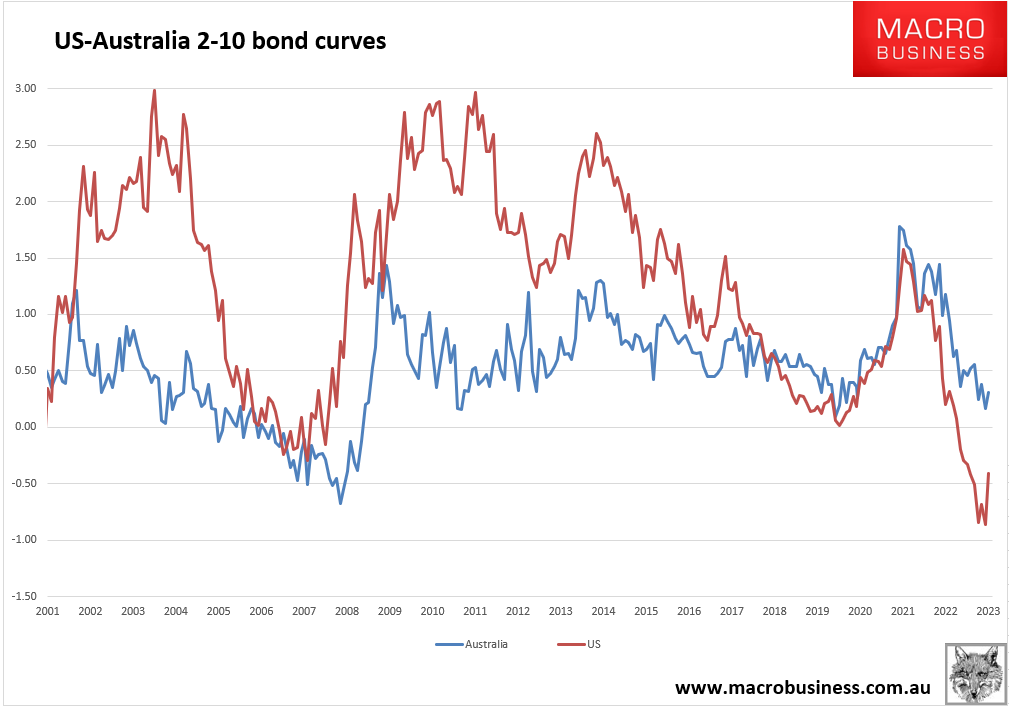

The one thing that is worse for the growth outlook than an inverted yield curve is the sudden steepening of the same as markets realise that the downturn is imminent. They buy bonds, especially at the short-end of the curve, in anticipation of central banks pivoting dovish.

We are there in the US:

And, increasingly, Australia too: