DXY fell and EUR rose Friday night:

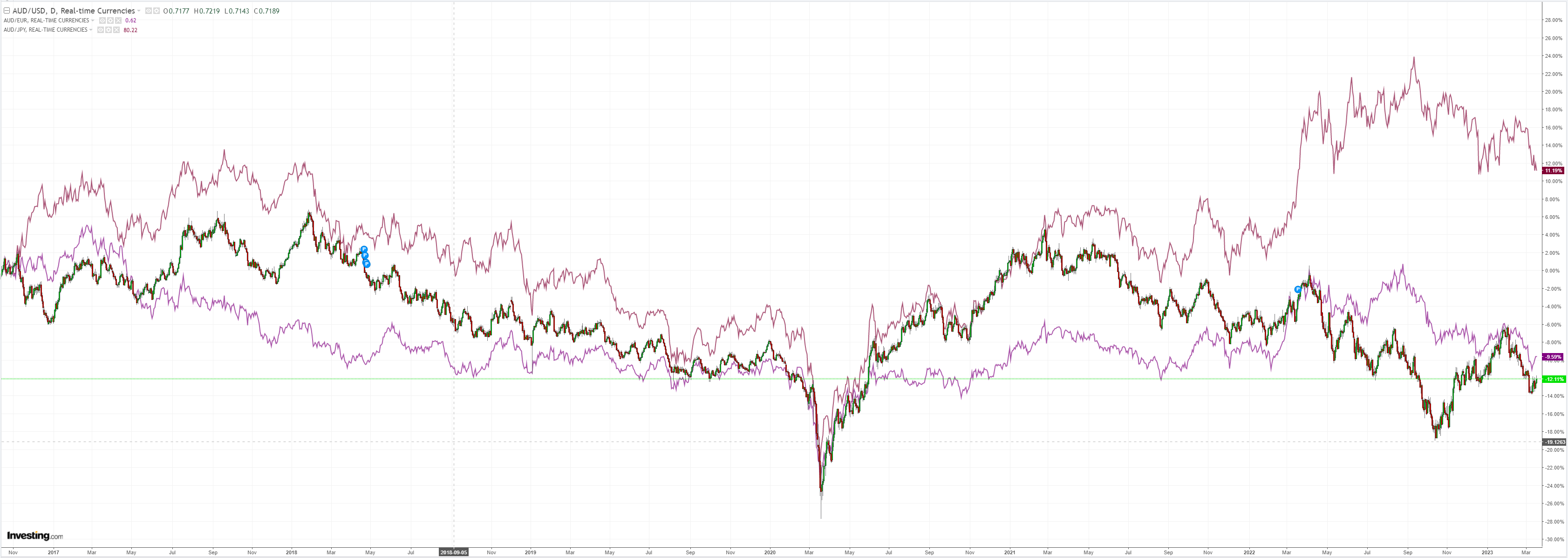

AUD popped:

Oil is beginning to price global recession and gold a new GFC:

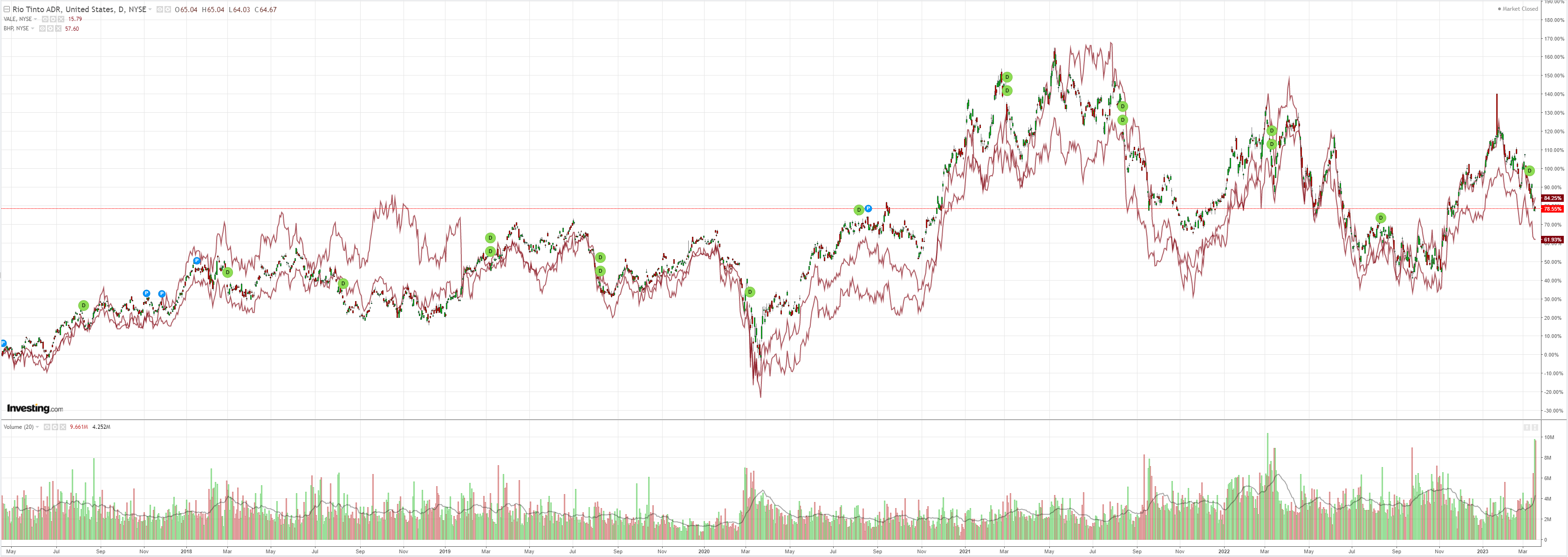

Dirt did better:

Miners held:

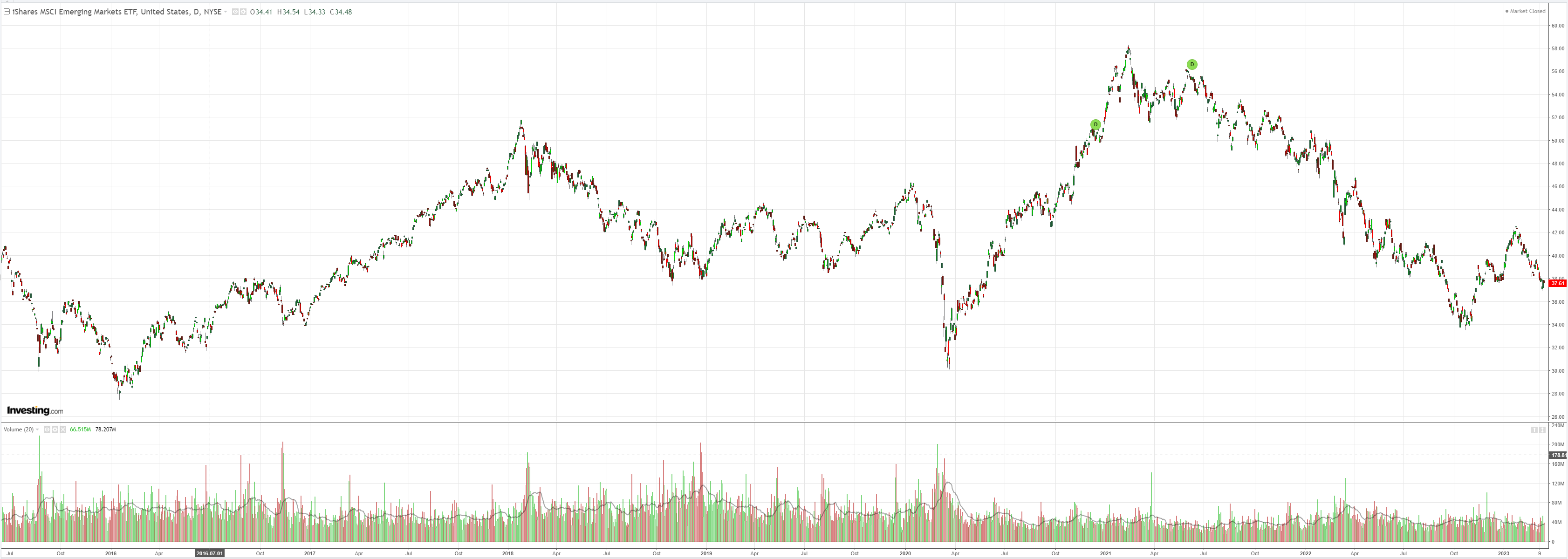

EM stocks too:

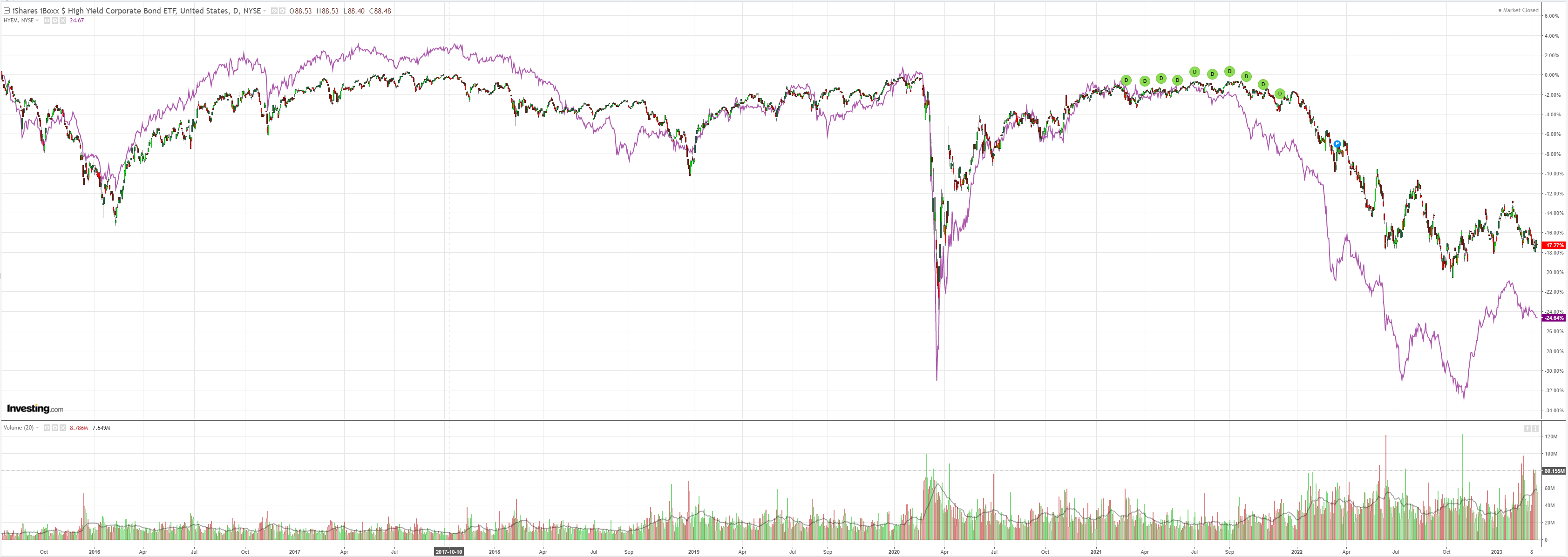

Junk is bleeding out slowly:

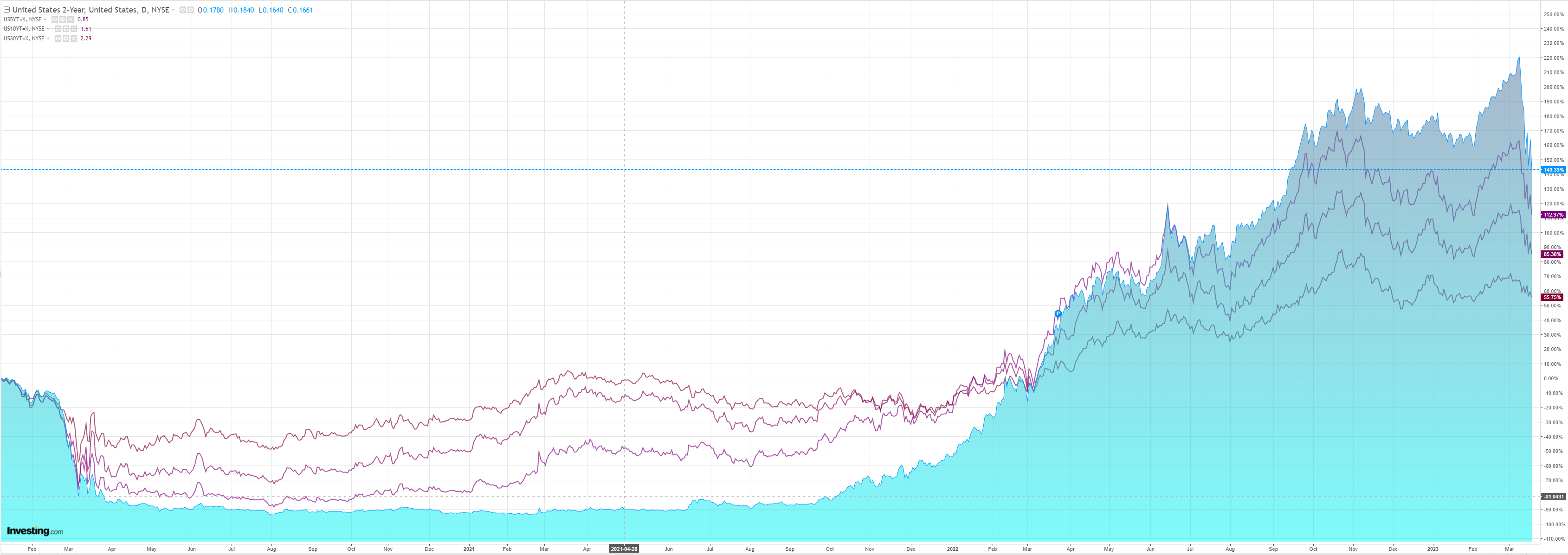

Treasuries were bid bigly:

Stocks fell anyway:

Credit Agricole wraps us up:

The SVB and Signature Bank failures as well as the turmoil surrounding Credit Suisse seem to be the result of idiosyncratic factors, but they could nevertheless signify a watershed moment in the global monetary tightening cycle. Indeed, these developments have become a focal point for market fears about the detrimental economic impact of the hawkish central bank policies and thus the risk of recession in North America and Europe. Furthermore, the central bank response so far has been to boost the banks’ liquidity position and thus ‘undo’ some of the previous tightening as well as to adopt a more data-dependent approach to future tightening in an attempt to soften the blow on the real economy.

If not dealt with properly, the banking sector problems could precipitate the end of the global tightening cycle. That said, global central banks also remain laser-focused on containing inflation and are aware that any rate-hike pause or liquidity injections could prolong the period of above-target inflation and may necessitate further aggressive tightening in the future. As the March ECB meeting has shown, the central banks’ overall stance could remain rather hawkish as a result, in a blow to market hopes for a meaningful recovery in risk sentiment in the near term.

Ahead of next week’s Fed policy meeting, we think that the immediate policy rate decision remains very uncertain and will depend on the performance of global bank stocks in the lead-up to the meeting. At the same time, however, we also believe that the Fed’s forward guidance will remain hawkish with the updated dot plot continuing to push against the renewed aggressive pricing of rate cuts by the markets in view of still-sticky US inflation and the resilient domestic economy. We expect the outcome of the Fed meeting to strengthen the credibility of its monetary tightening and thus give US real rates and the USD a boost.

SVB and CS are not idiosyncratic. They are canaries in the tightening coal mine as 15 years of loose money runs headlong into a pandemic fiscal splurge resilient economy and the fastest rate hiking cycle in history.

Central banks don’t even need to keep tightening for this to run. US regional banks are leading all DM banks into a run on deposits, a commercial property bust, and a credit crunch:

Nor is it going to stop at US borders. It’s coming to Europe next. And Australia.

As this anvil drops on the real economy, 15 years of QE-protected business models and three years of COVID bankruptcy moratoriums are going to jackknife into bank balance sheets for a second round bust.

This is an end-of-cycle shock and a rising AUD does not compute.