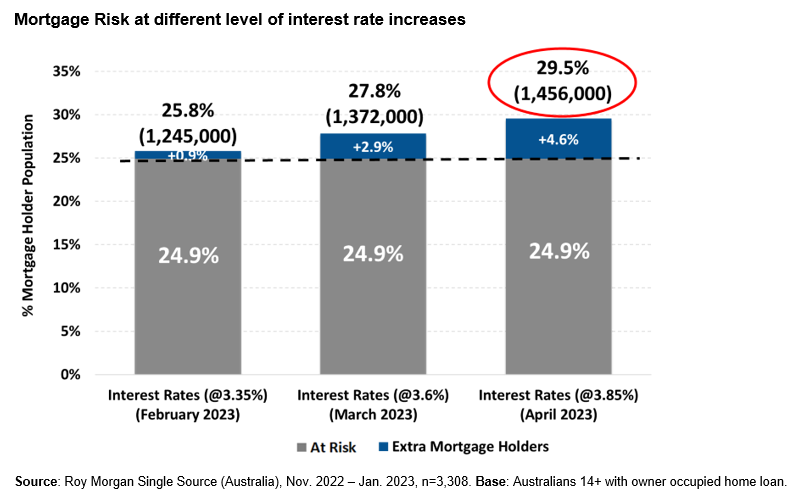

Roy Morgan Research has modelled the direct impact of the existing 3.25% jump in the Official Cash Rate (OCR), as well as two further 0.25% rate increases in March and April.

This modelling estimates that one quarter (24.9%) of Aussie mortgage holders (1.2 million households) are already classified as ‘At Risk’, defined as their mortgage repayments being greater than a certain percentage of household income (i.e. 25% to 45% depending on income and spending).

This is the highest share of mortgage stressed households since April 2012.

Moreover, mortgage stress would lift to nearly 1.5 million households (29.5% of mortgage holders) if the Reserve Bank lifts the OCR in March and April by 0.25% respectively:

Roy Morgan warns that “this is a conservative model, essentially assuming all other factors remain the same. And of course we are already seeing an increase in unemployment”.

“The greatest impact on an individual, or household’s, ability to pay their mortgage is not interest rates, it’s if they lose their job or main source of income”.

“If there is a sharp rise in unemployment during his period mortgage stress will rise precipitously towards the highest levels experienced during the Global Financial Crisis in 2007-08-09. At that time a peak of 35.6% of mortgage holders were considered ‘At Risk’ in May 2008”, Roy Morgan said.

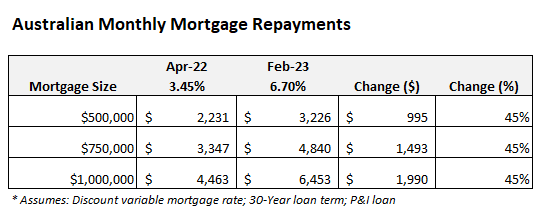

Average variable mortgage repayments have already soared by 45% following the RBA’s 3.25% of rate hikes:

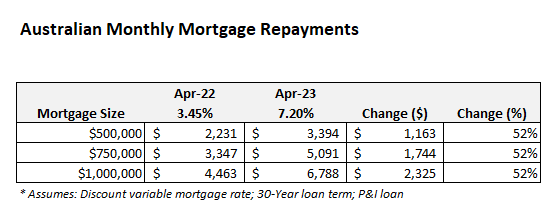

If the RBA hikes rates another 0.5% over the next two months, then it would lift average variable mortgage repayments by 52% against their April 2022 pre-tightening level:

For a borrower with a $500,000 variable mortgage, this represents a $1,163 increase in monthly mortgage repayments since April 2022.

Moreover, there are nearly 900,000 mortgage holders that will this year switch from cheap pandemic fixed rates to variable rates that are more than double current levels:

In short, many more Australian mortgage holders will be pushed into stress this year.