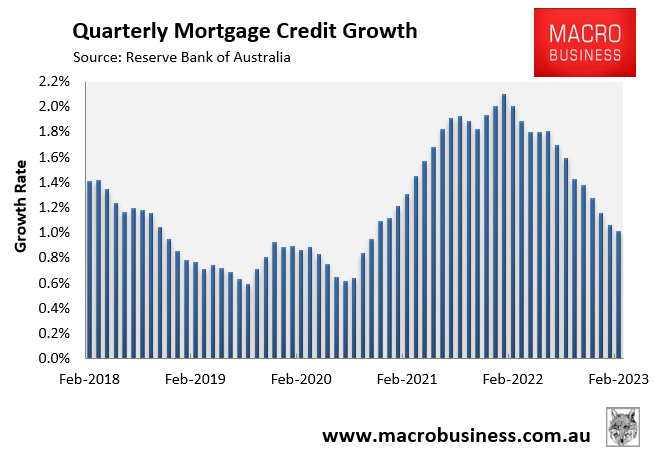

The Reserve Bank of Australia (RBA) has released data on the value of mortgages outstanding, which shows that mortgage growth fell to just 1.0% over the February quarter.

This was the slowest rate of growth since October 2020:

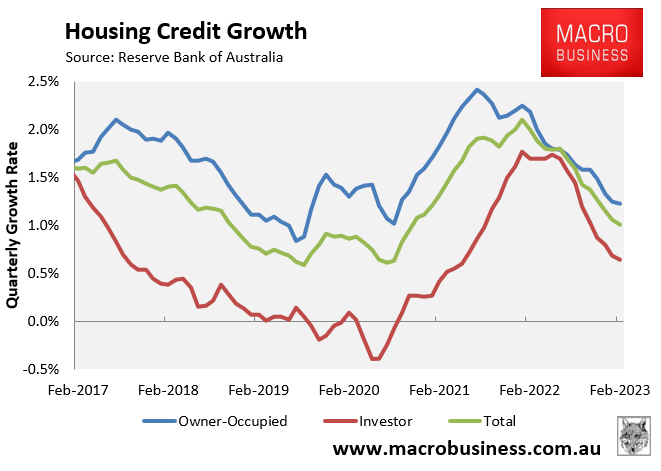

Mortgage growth has tanked across both owner-occupiers (1.2%) and investors (0.6%):

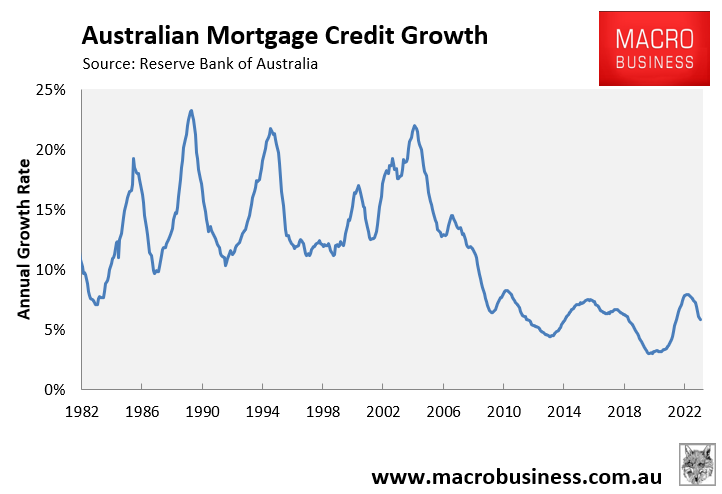

Annual mortgage growth has also fallen to 5.8%, which is the slowest pace of growth since July 2021:

The decline in mortgage credit growth makes sense since it captures the first nine interest rate hikes from the RBA, which reduced borrowing capacity by around 30%.

However, the this data should be viewed with caution with respect to their impact on house prices.

Mortgage credit growth measures the addition to the mortgage stock from new mortgages taken out by borrowers (increases the stock of debt outstanding) and the repayment of mortgage debt by existing borrowers (reduces mortgage debt), which are two distinct things.

Only the first factor — new mortgages — has any real effect on home values.

The second factor, mortgage payments made by current borrowers, has no bearing on prices and does not represent the demand for new homes.

Moreover, given interest rates are at decade highs, we are likely seeing mortgage holders reduce the amount of payments above the scheduled amount.

This would have the impact of lowering mortgage credit growth without impacting house prices.

Next week’s Australian Bureau of Statistics’ lending indicators release will track new mortgage originations to February, and will provide a far better indicator for house prices.