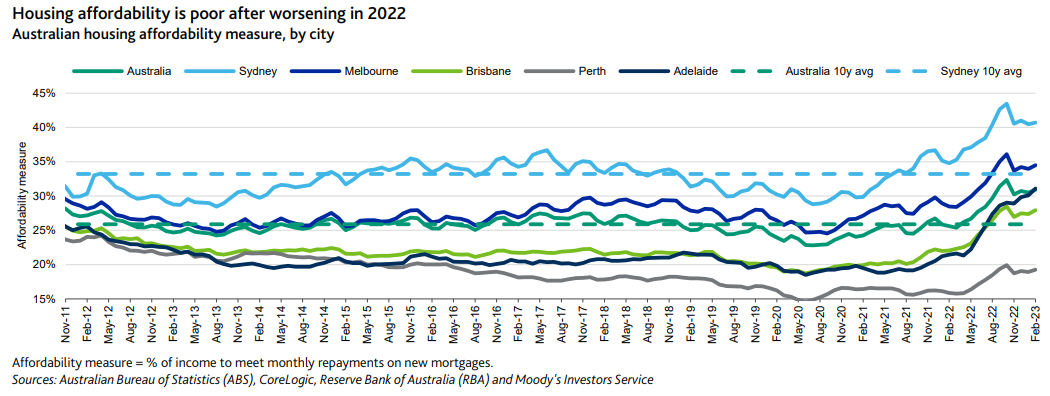

Moody’s Investor Service has published a new report on Australia’s housing market, which contends that housing affordability has worsened materially despite the sharp fall in house prices.

It measures housing affordability as the proportion of household income borrowers need to meet repayments on new mortgages.

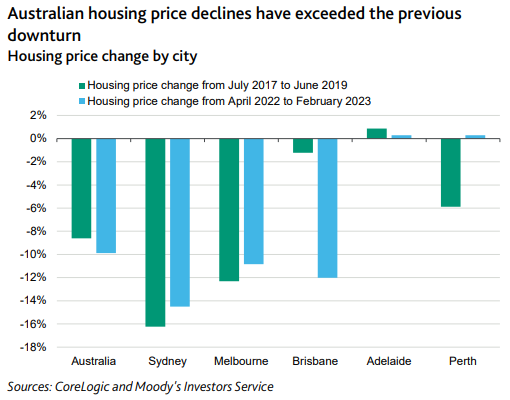

Moody’s notes that dwelling values nationally have declined by around 10% since April last year, led by the three main capital cities:

Yet, housing affordability has worsened over the same period.

In February, new home loan borrowers needed an average 30.9% of monthly income to meet monthly mortgage repayments, up from 26.4% in May 2022, when interest rates began to increase:

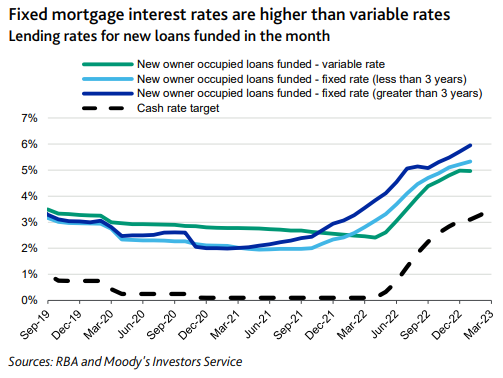

The reason why housing affordability has worsened is obvious: the RBA’s aggressive interest rate hikes have more than offset the fall in dwelling values.

“Housing prices declined and household incomes increased slightly, but these factors were not sufficient to improve affordability for new mortgage borrowers over 2022 given sharp rate rises”, Moody’s notes.

“The RBA has increased the cash rate by 3.5 percentage points to 3.6% since it started its rate rise cycle in May last year”, which has driven mortgage rates sharply higher:

Looking ahead, Moody’s expects housing affordability to remain poor in 2023 as rising mortgage rates are roughly matched by falling prices.

“More interest rate rises by the RBA will further push up mortgage lending rates and weigh on housing affordability for new borrowers”, the report says.

“Over 2023, we expect that ongoing housing price declines and further interest rates rises will broadly balance out in terms of their effect on housing affordability”.

“We therefore expect the share of income that borrowers need to meet repayments on new mortgages will hold at around the February level”, Moody’s concludes.