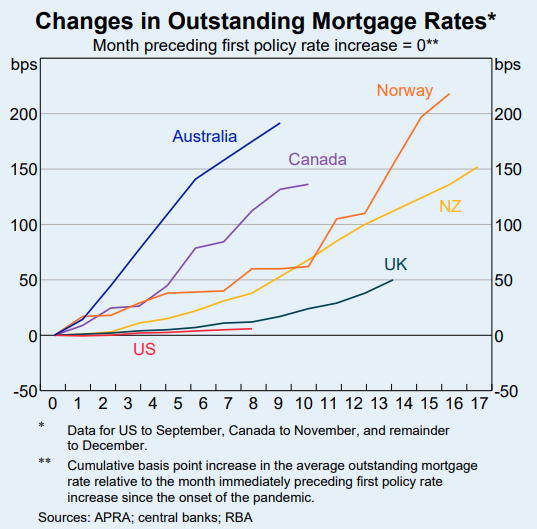

February’s Statement of Monetary Policy included the below chart plotting the rise in mortgage rates across key developed nations since central banks began lifting interest rates:

As you can see, before March’s 0.25% rate hike, Australian mortgage holders had experienced nearly 200 basis points of tightening, which is more than other English-speaking nations.

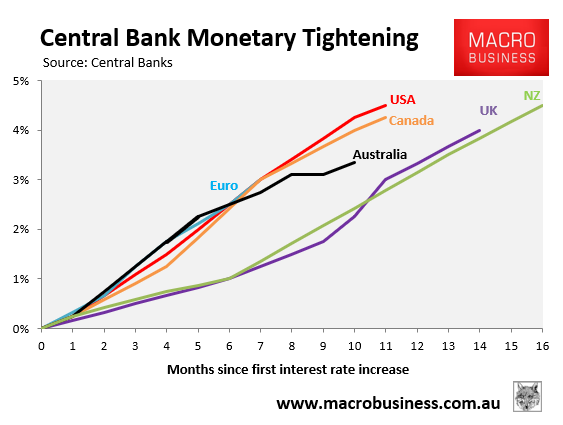

This is despite the Reserve Bank of Australia (RBA) lifting rates by less than these nations, as illustrated below:

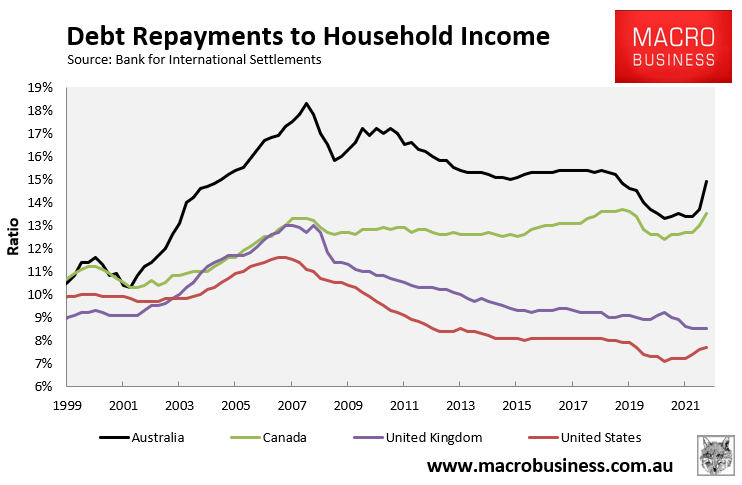

The latest debt repayments data from the Bank for International Settlements, current to the September quarter of 2022, likewise shows that principal and debt repayments as a share of household income has increased further in Australia than elsewhere, with Aussies also spending the highest aggregate share of income (14.9%) on repaying debt:

The reason why Australia’s debt burden is so much higher than those other countries is because:

- Australia’s household debt load relative to GDP is the second highest in the world (behind Switzerland); and

- Australia has a much higher share of variable mortgages than most other nations, which means increases in interest rates are passed on more quickly to Australian borrowers.

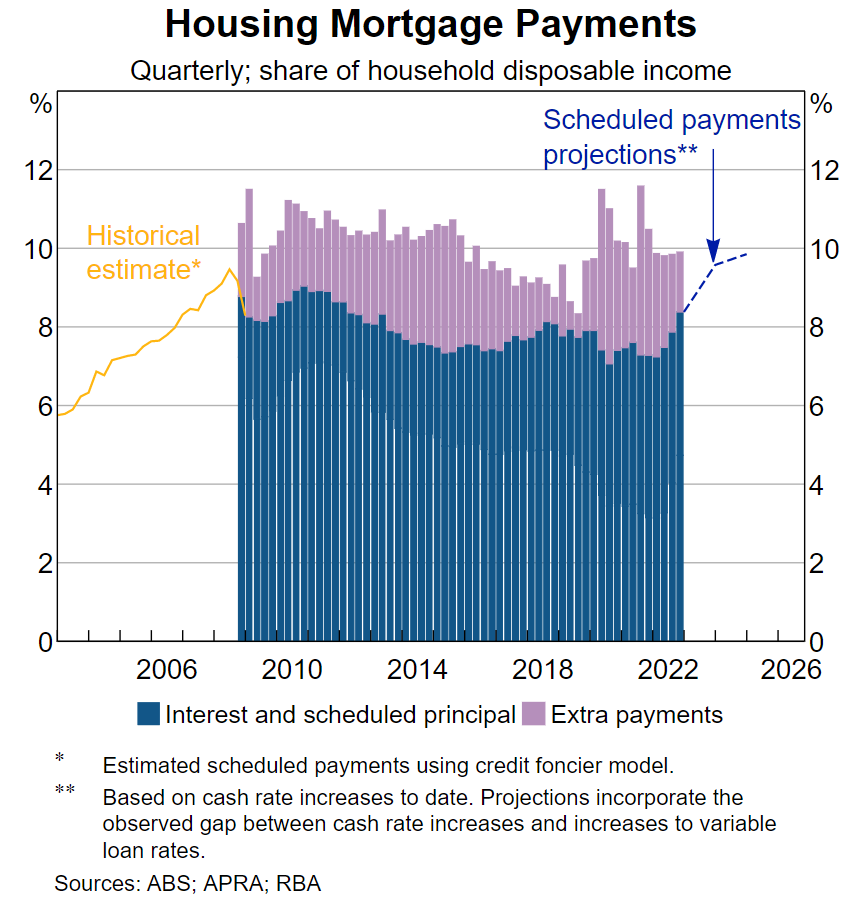

The official Australian cash rate was only 2.35% in September 2022. Therefore, the above chart does not include an additional 1.25% of official rate hikes, which will obviously have increased debt repayments much further.

In fact, this week’s speech from RBA assistant governor Chris Kent showed that scheduled mortgage repayments will lift to an all-time high share of household income once the fixed rate mortgage reset runs its course:

The above chart also highlights why the RBA does not need to continue hiking rates, as there is already significant tightening ‘built-in’ to the pipeline owing to the upcoming fixed rate “mortgage cliff”.