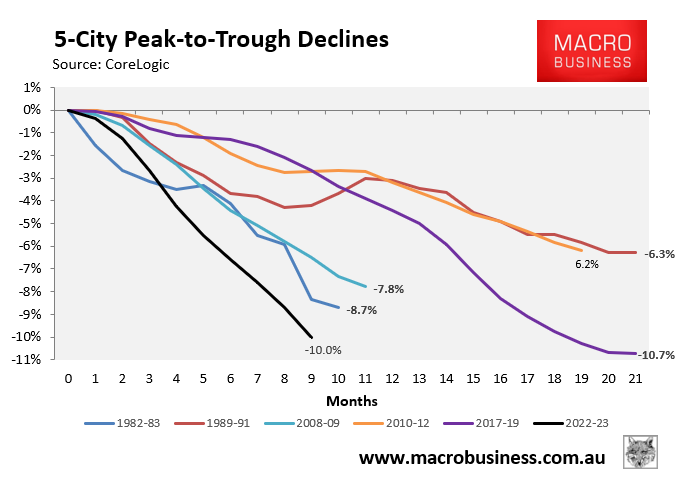

With Australian home values falling at their fastest pace on record, alongside the sharpest lift in mortgage rates on record, vendors are pulling their homes from the market.

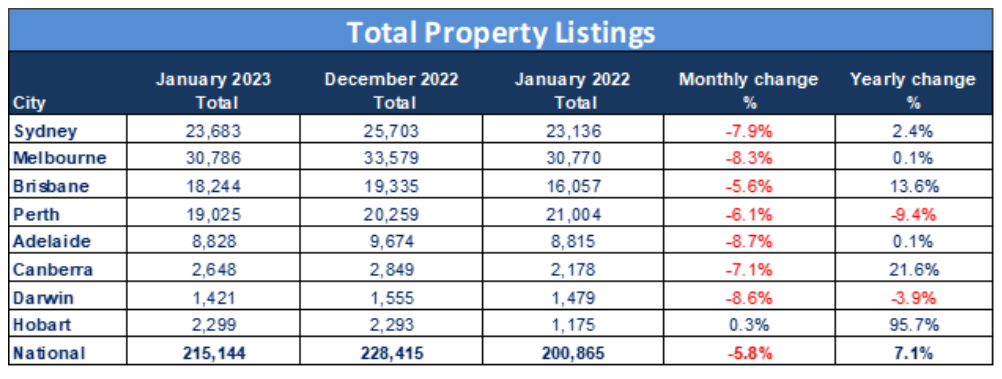

According to new data from SQM Research, total property listings plunged 5.8% in January but were still up 7.1% year on year:

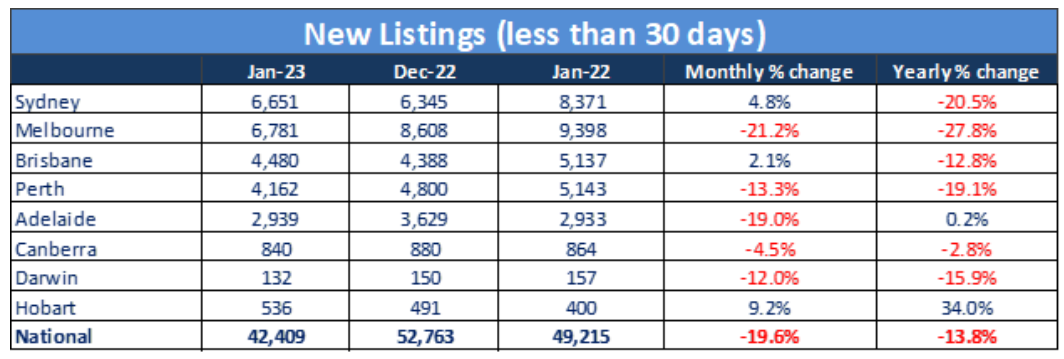

New listings (less than 30 days) plunged 19.6% in January to be down 13.8% year-on-year:

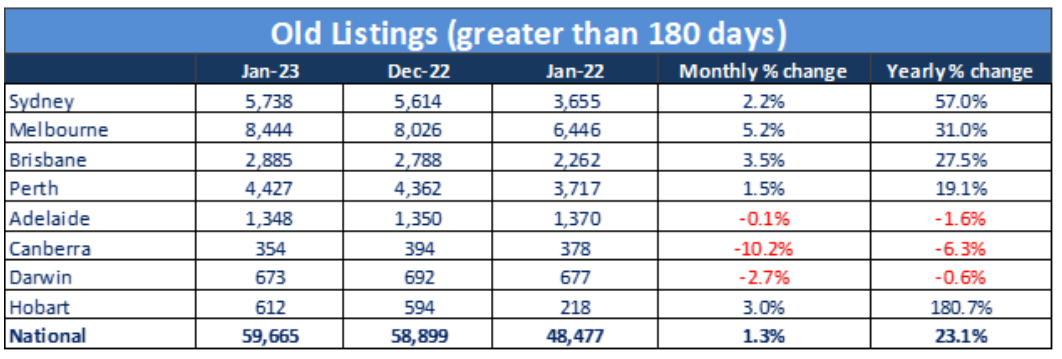

This was offset by old listings (greater than 180 days), which actually rose 1.3% over January to be 23.1% higher year-on-year:

Commenting on the result, SQM Research Managing director Louis Christopher noted that “the January holiday period is traditionally a quiet time for listings so it is no surprise we recorded a fall in activity over this month”.

“However, attention should be given to the new listing counts, whereby there has been a 13.8% fall in new listing activity compared to this time, last year. Most property owners believe it is a bad time mot sell right now and so are holding back, waiting for a housing market recovery”.

The slump in new listings is preventing home values from falling more sharply given buyer demand has crashed in response to reduced borrowing capacity arising from the RBA’s aggressive rate hikes.

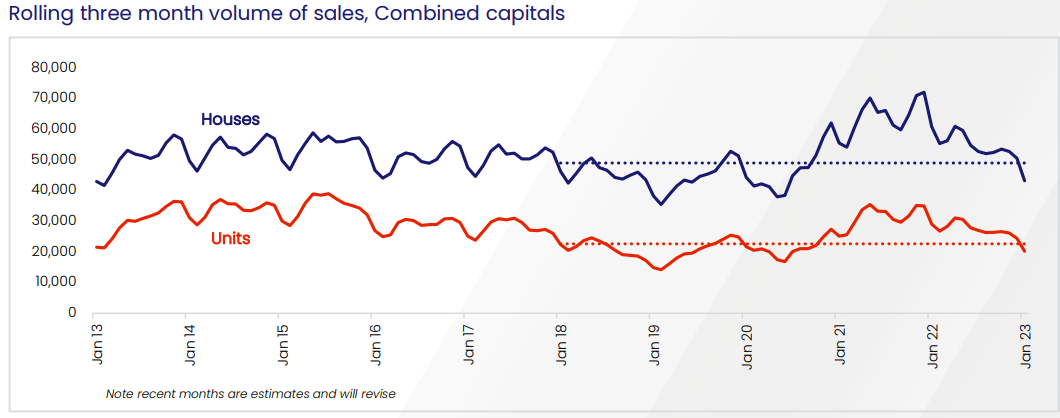

According to CoreLogic, actual sales volumes across the combined capital cities have fallen below average:

Thus, the reduction in new listings is helping to match vendor supply with buyer demand.

The big thing to watch in 2023 is whether ongoing RBA rate rises, alongside the fixed rate mortgage reset, causes a sharp lift in forced sales.

If this occurs, then home prices will fall more sharply.