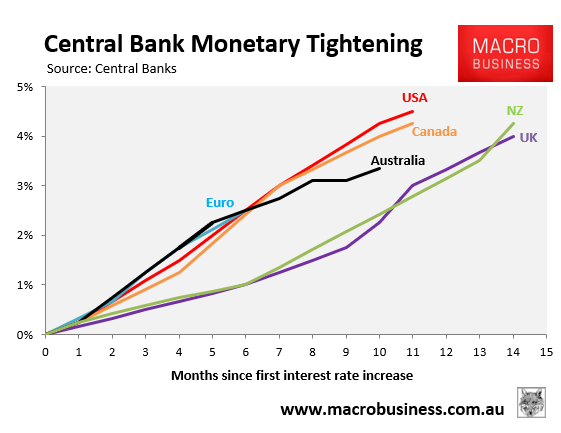

The Reserve Bank of New Zealand (RBNZ) has been one of the world’s most aggressive central banks, lifting interest rates earlier and by more than most other jurisdictions:

The RBNZ has also explicitly forecast a further increase in the official cash rate to 5.5% (from 4.25% currently), alongside a 20% peak-to-trough decline in house prices and a recession.

Interestingly, most New Zealand mortgage holders are yet to be impacted by the RBNZ’s aggressive monetary tightening. This is because the overwhelming majority of mortgages in New Zealand are fixed rate.

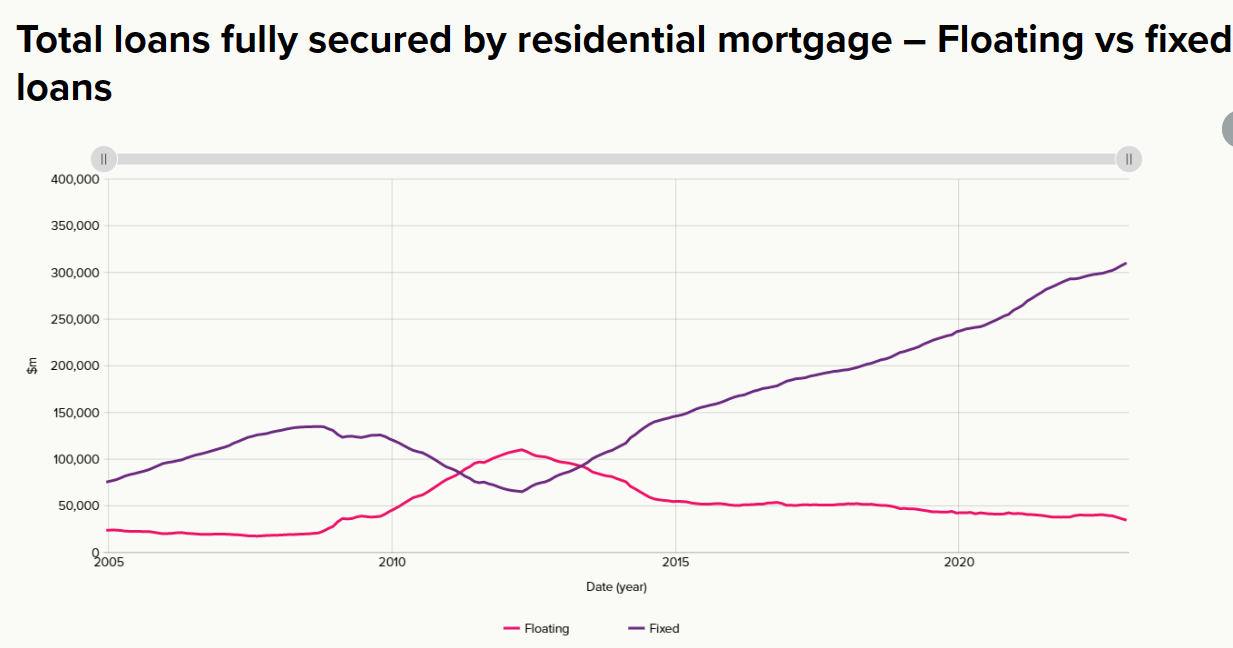

As illustrated in the next RBNZ chart, the overall stock of outstanding mortgages in New Zealand rose by around $6 billion to $344.9 billion in the last six months of 2022.

Yet, the amount on floating rate mortgages dropped by nearly $5.7 billion (14%) to $34.7 billion. That’s the lowest figure since January 2009.

In fact, the share of the total mortgage stock on floating rate mortgages is now at a record low of just over 10%:

The situation will change this year with Westpac recently warning that “more than half of all mortgages will come up for re-fixing in the next twelve months, and many borrowers will face large increases in their debt servicing costs”.

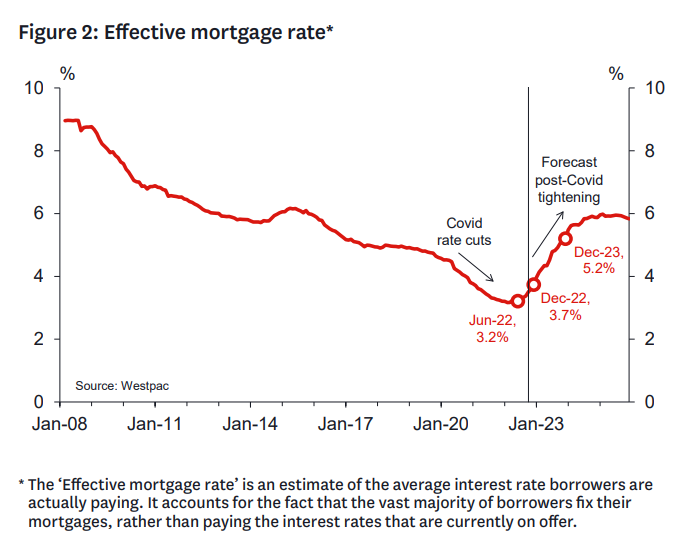

Westpac estimates that the ‘effective’ average mortgage rate New Zealand borrowers are paying will roughly double in 2023 as these fixed rate mortgages are repriced:

“For example, a borrower who fixed their mortgage at 2.7% in 2020 will now face refixing at a rate over 6%”, according to Westpac.

As similar, albeit less extreme, situation will unravel in Australia where nearly one quarter of mortgages by value will reset from their current cheap pandemic fixed rates to more than double current levels.

That is when the aggressive rate hikes from both Reserve Banks will truly be felt across both economies.

If you are looking to shave thousands of dollars off your mortgage repayments, try the MacroBusiness Compare n Save mortgage comparison tool. It takes less than a minute. And if you wish to refinance, the process is easy.

Compare 100s of loans in seconds, hassle free…..

and when you’re ready to apply, we’ll manage the process for you.

I Want To Refinance

I Need A Loan