In his preview of next week’s monetary policy meeting, Bank of New Zealand (BNZ) economist Stephen Toplis argues below that the Reserve Bank may have “already done enough” monetary tightening given around half of all mortgages this year will transition from cheap fixed rates taken out over the pandemic to rates that are at least double current levels.

Nevertheless, Toplis is still tipping another 0.5% rate hike next week, followed by another hike at the following meeting in April.

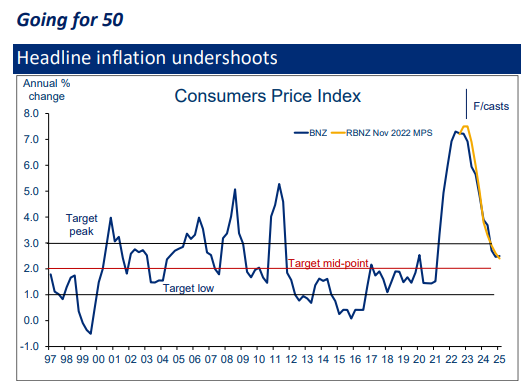

Toplis also believes the Reserve Bank should lower its expected terminal rate by 25 basis points to around 5.25%.

In a formal sense, we have moved from a 75 call to a 50 call but our conviction is not strong. We have long said market pricing on the day could be the deciding factor for the Reserve Bank given the line-ball nature of the decision. Current market pricing is headed toward 50…

We remain in the camp that says the Reserve Bank should now be moderating the pace of increase. Indeed, with the long lags between monetary policy setting and the economic reaction function, it is conceivable the Bank has already done enough.

In particular, it is worth noting that a significant proportion of past tightening is still to hit mortgage holders’ cash flows. It will, in due course.

Monetary policy settings are extremely tight. The Reserve Bank has its foot firmly planted on the brake. There comes a time when such restraint is no longer necessary. We are definitely approaching that time.

Be that as it may, we recognise that financial markets are very keen to price in a near-term reduction in rates. The RBNZ will not want to encourage that sentiment so will be “forced” to keep tightening.

Given this, we think the best approach for the Bank would be to raise the cash rate 50 basis points to 4.75%, signal 25 to 50 basis points further thereafter and then move to a data watching framework accompanied by a strong warning that it expects interest rates to stay elevated for an extended period of time…

In addition to moderating the pace of the tightening cycle, we think the RBNZ may well lower its expected terminal rate by 25 basis points to around 5.25%. We doubt it would feel comfortable reducing it by any more than that, at this juncture.

However, we remain of the view that the ultimate peak may be as low as 5.0% rather than the 5.5% the Reserve Bank currently forecasts and the market currently is giving a nod to.

Whatever the case, we think that the peak will come relatively early in 2023, rates will stay there for around 12 months before trending lower starting in calendar 2024.