In 2019, the Australian Prudential Regulatory Authority (APRA) loosened mortgage assessment rules, replacing the requirement for lenders to assess borrowers at a 7% mortgage rate with a 2.5% buffer above the loan’s interest rate.

In October 2021, APRA raised the mortgage repayment buffer to 3.0% in response to “growing financial stability risks from ADIs’ residential mortgage lending” amid rapidly increasing home prices.

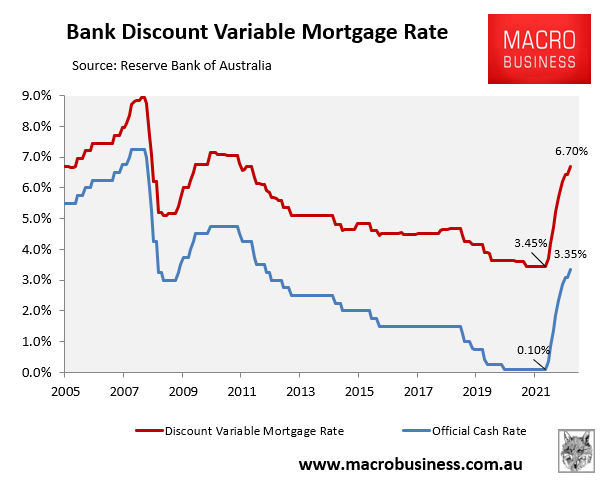

Tuesday’s 0.25% increase in official interest rates by the Reserve Bank of Australia (RBA) has lifted the official cash rate (OCR) to 3.45%, which is an increase of 3.25% from its April 2022 pre-tightening level:

In the process, average variable mortgage rates have risen by a similar amount.

Thus, APRA’s mortgage repayment buffers have well and truly been breached, meaning most households that borrowed in 2021 or early 2022 at rock bottom mortgage rates are now ‘in the red’ from the RBA’s aggressive rate hikes.

Moreover, for every rate hike from now on, there will be increasing numbers of mortgage borrowers who are required to make higher repayments than they were tested for when they originated their loan.

ANZ Bank CEO, Shayne Elliott, encapsulated the problem in an interview on Wednesday morning on radio 3AW.

Elliott said ANZ had yet to see people lose their homes. But the impact following Tuesday’s rate hike was critical because the buffer they built into home loans was now gone.

“The lowest rate we ever gave anyone was 1.94% as a fixed rate”, Elliott said.

“We assumed rates could go up to 5.25%, so we built a buffer which is about where we are now, so that buffer has worked”.

But now “we are at a very difficult pivot point”.

“Up to now people have been managing Okay. But it’s really from here on it gets very difficult because we are over that buffer, and it starts to really bite into people’s savings”.

Borrowers that took out ultra cheap fixed rate mortgages at around 2% are particularly exposed, as are those who borrowed to their maximum limit.

Loosening the mortgage repayment buffer was the key policy maneuver that lifted house prices out of the Hayne Banking Royal Commission funk.

Now it is coming back to bite amid the sharpest increase in mortgage rates in Australia’s history.

Compare 100s of loans in seconds, hassle free…..

and when you’re ready to apply, we’ll manage the process for you.

I Want To Refinance

I Need A Loan