KPMG’s economics team recently estimated that more than 800,000 fixed-interest mortgages that were taken out in recent years will transition to variable rate loans in 2023. The RBA puts the figure at 880,000.

Accordingly, a household with a $600,000 mortgage will face a $16,500 increase in their annual repayments when switched from a fixed-rate loan to variable rates.

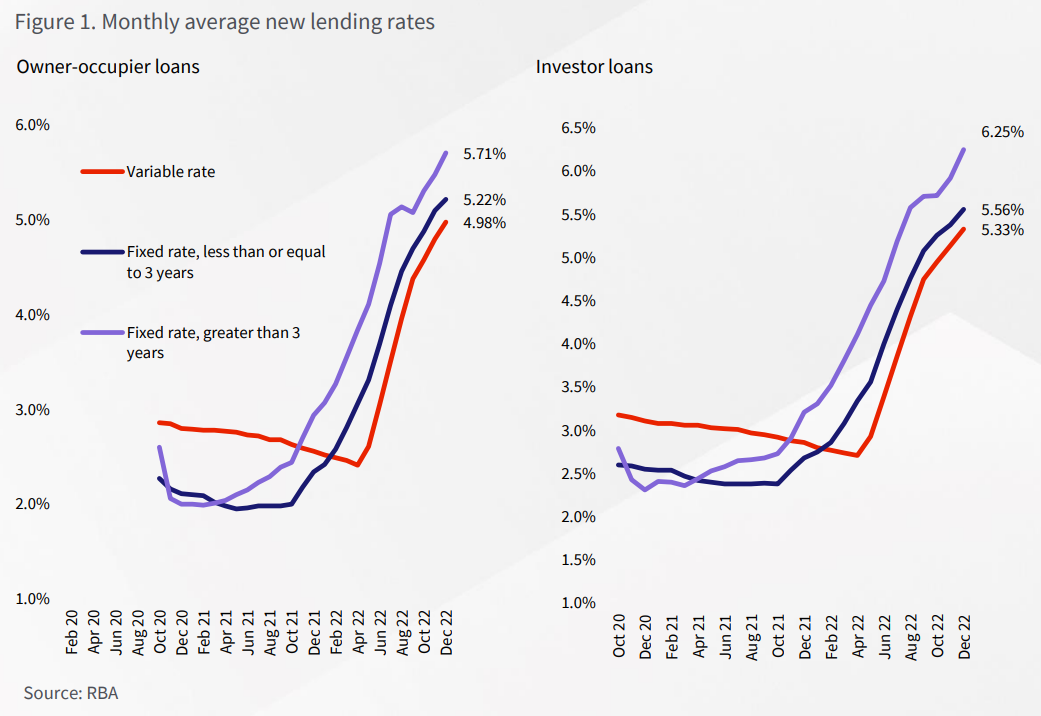

CoreLogic’s Head of Research, Eliza Owen, has published analysis of the fixed rate mortgage cliff bearing down on Australia, which “has emerged as one of the biggest potential risks to housing market values, and overall stability in 2023”.

Owen notes that “short-term fixed loan rates averaged as low as 1.95% in May 2021 for owner-occupiers, as bank funding costs plunged in line with the RBA’s temporary Term Funding Facility and fierce competition among lenders”.

“Banks financed around 1.2 million new home loans between January 2020 and October 2021 based on ABS data, when fixed rates were falling and stayed low”, of which around 40% were fixed rate loans.

This year, “around 23% of all outstanding mortgage debt will be re-priced over the course of the year, and re-priced at a much higher rate”.

The below CoreLogic chart illustrates the fixed rate “mortgage cliff” bearing down on Australia:

“The pain will be felt most acutely from April 2023”, notes Owen.

Eliza Owen summarises the risks as follows:

“Interest rates have risen beyond 3 percentage points for many borrowers, which is the minimum serviceability buffer recommended by APRA in assessing whether someone can repay their debt”.

“Stretched serviceability could be compounded by an increase in the unemployment rate this year along with higher than budgeted household costs due to high inflation”.

“A rise in distressed sales could also put added downward pressure on property values. If people are forced to sell their home in a declining market, there is the added risk of being unable to recover mortgage debt from the sale of a home”.

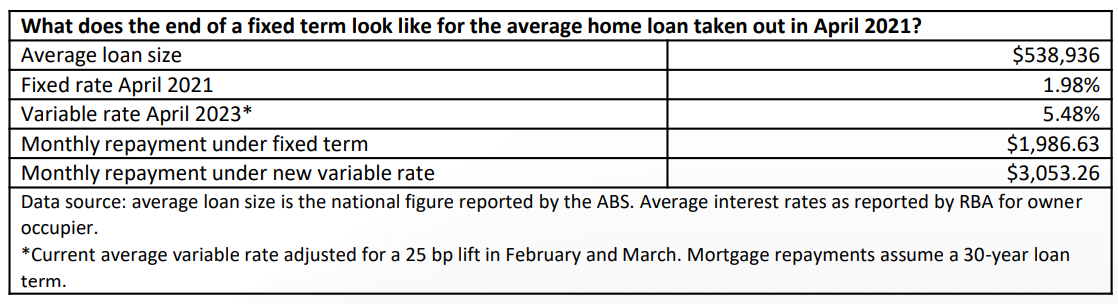

Owen has also compiled the below table highlighting the huge lift in repayments facing recent fixed rate borrowers:

As you can see, somebody with an average sized $538,936 mortgage that resets from their cheap pandemic fixed rate to the current variable rate is already facing a $1,066 increase in monthly mortgage repayments.

This figure will obviously continue to rise as the RBA tightens further.

Owen concludes by stating “there’s no escaping that Australians with fixed-rate loans are about to see a painful adjustment”.

“So far, listings data and arrears data suggest there is minimal impact on the housing market from defaults. However, the true test of the market will be over the next ten months”.

A lot will depend on what happens to the unemployment rate. If it rises sharply, so too will defaults and forced sales.

The RBA is walking a tightrope lifting rates so aggressively.

If you are looking to save thousands of dollars in mortgage repayments, try the Compare n Save mortgage comparison tool. It takes less than a minute. And if you wish to refinance, the process is easy.

Compare 100s of loans in seconds, hassle free…..

and when you’re ready to apply, we’ll manage the process for you.

I Want To Refinance

I Need A Loan