Late last year, the Reserve Bank of New Zealand (RBNZ) forecast further increases in the official cash rate to 5.5% (from 4.25% currently), alongside a 20% peak-to-trough decline in house prices and a recession.

In a new report, ANZ Economics has also tipped a recession in 2023, based on a forecast peak in the official cash rate to 5.25%.

A policy-induced recession is looming. While it’s going to hurt some households more than others, we’re hopeful this slowdown will turn the tide on domestic inflation, and set the broader economy on a more sustainable path over the longer run…

This time last year we were forecasting a peak OCR of 3% – and as we go to print the OCR is at 4.25%!..

Macroeconomic policy will find balance in 2023

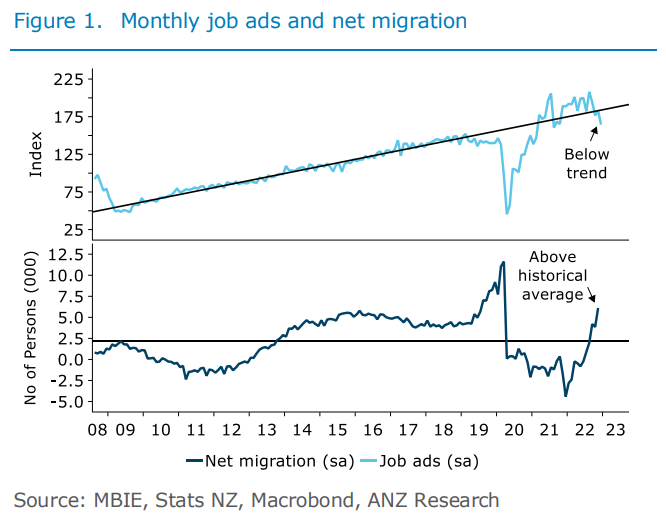

Monetary tightening is clearly getting traction: the housing market is firmly in retreat, both consumer and business confidence are in disarray, households are tightening their belts, and labour demand is falling (just as imported labour supply appears to be lifting sharply, figure 1).

At some point over the coming months, the RBNZ will become convinced that the OCR is sufficiently high to guide inflation back to the 2% target midpoint in an acceptable timeframe, and that ‘sticky’ inflation risks are balanced against downside activity risks. In other words, the RBNZ’s strategy will change from a full-on counter-attack against inflation to ‘watch, worry, and wait’ mode…

Unless downside (deflationary) economic risks materialise, we think that the job of getting domestic (non-tradables) inflation down could prove harder than some realise – this kind of inflation tends to be sticky! That’s why our forecast is for the OCR to remain on hold at 5.25% from May through to the end of our forecast horizon. Of course, that peak could easily be 5% or 5.5%, depending on how the

data evolve over coming months. But wherever the RBNZ decides to park the OCR while they wait for core inflation to slow and the labour market to transition to sustainable levels, unless something left-field occurs, it could be there for quite some time…

Perhaps the biggest challenge the RBNZ will face this year will be the optics around maintaining contractionary monetary conditions while the economy is in recession. It’s going to be difficult times ahead for those feeling the brunt of rate hikes, and the bad news stories are only set to become more frequent as highly indebted households continue to roll onto higher mortgage rates. But this is the unfortunate reality of how monetary tightening works, pulling demand out of the economy by squeezing those with debt, and encouraging others to save…

However, inflation will slow; the RBNZ ‘just’ needs to tighten monetary conditions sufficiently. If they overcook it, cuts will come sooner than otherwise; if they undercook it; the OCR will end up going higher than otherwise. But OCR hikes can get the job done, there’s no doubt about that. Where the question does lie is in how much short-term damage to the housing market and labour market might be incurred, by necessity or not, along the way…

Our outlook in detail

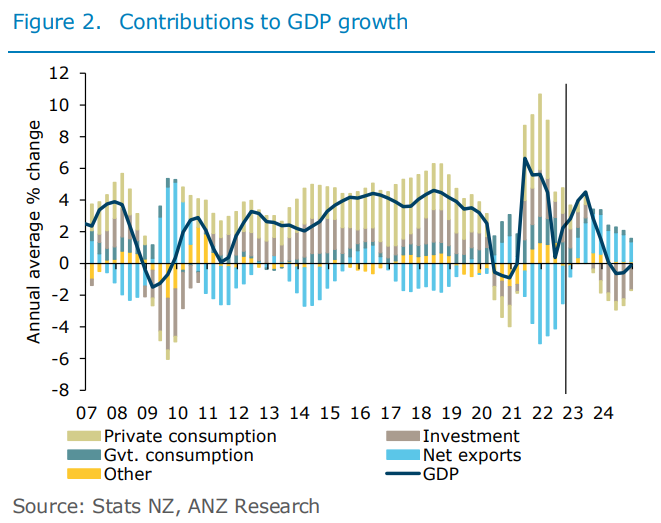

The broad story around our outlook hasn’t changed a lot over the past few quarters, but we have had to think hard about data volatility, timing and magnitude. Overall, domestic demand is poised to contract, but the ongoing recovery in services exports (chiefly international tourism and education) and softer demand for imports will provide a sizable offset (figure 2).

But the RBNZ has signalled that in order to get inflation down they need the domestic downturn to dominate (resulting in recession), and they have the tools to make it happen…

Our forecast has the economy entering recession in Q2 2023, but the GDP data are currently very volatile. If this volatility persists, recession could easily end up occurring sooner than expected or not at all, if one focuses on the technical definition of two quarters of negative GDP growth in a row…

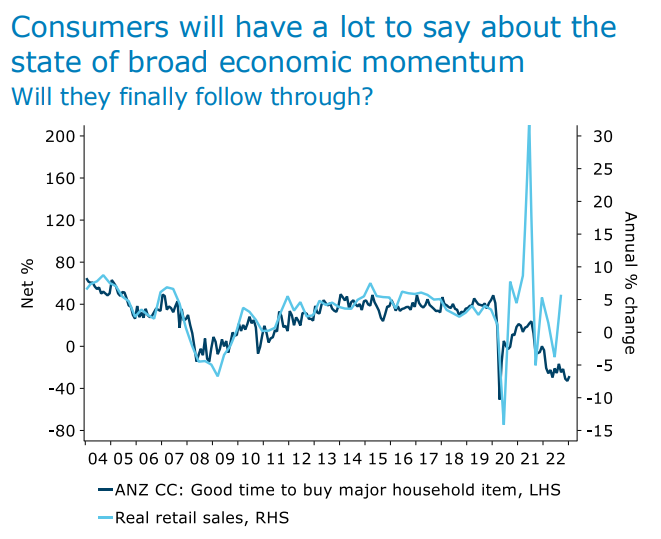

Given its sheer size, private consumption expenditure always has a lot to say when it comes to broad economic momentum. And the mix of rising interest rates, falling house prices (we maintain our forecast for peak-to-trough decline of 22%), and a softening labour market is expected to see households tighten their belts further. While continued data volatility seems like a very real possibility over the next few quarters, the signal from our consumer confidence survey suggests some softer retail spending ahead…

That said, the recent experience has been consumers reporting that it’s a terrible time to buy a major household item, but then going out and spending anyway.

However, we think this dynamic has turned. Indeed, consumer wariness in an environment of high income growth and strong job security is one thing, but wariness against a backdrop of a slowing economy and deteriorating job security is quite another…