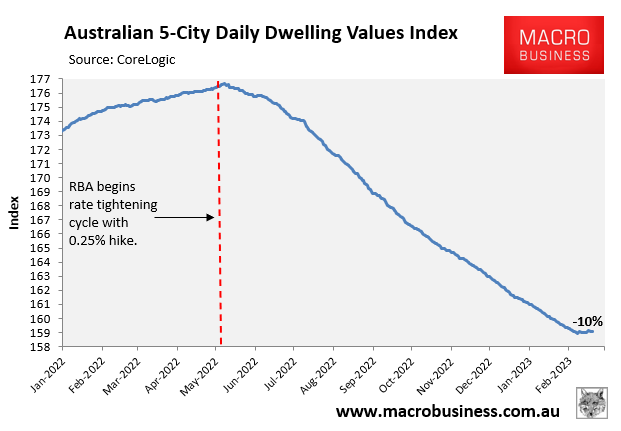

CoreLogic’s daily dwelling values index has recorded an unexpected rebound in capital city dwelling values, which have risen 0.1% over the past 12 days.

This has broken a nine-month run of falling dwelling values:

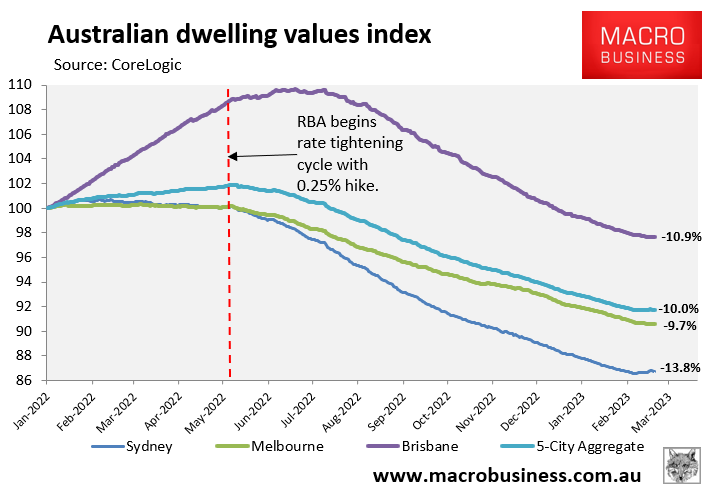

The rebound has been driven by Sydney, where values have rebounded 0.2% over the same time period:

The reversal of fortunes naturally raises the question of whether Australia’s housing correction might be coming to an end.

In his weekly market update, AMP Capital chief economist, Shane Oliver, explained why he believes we are witnessing a ‘dead-cat bounce’ that will inevitably revert back to falling dwelling values.

Oliver notes that it is possible that the cycle “is now turning up again” given “the return of immigration and the tight rental market”.

But he believes it more likely “reflects the return of bargain hunters and a bit of ‘fear of missing out’ demand helped along by low listings and optimism coming into the year that interest rates were close to peaking”.

Moreover, “with the RBA signalling several more hikes to go, the capacity to borrow and pay being well down from year ago levels and the combination of the fixed mortgage cliff which will see 880,000 mortgages face more than a doubling in their interest bill this year and the increasing risk of recession with much higher unemployment, we continue to see more weakness ahead”.

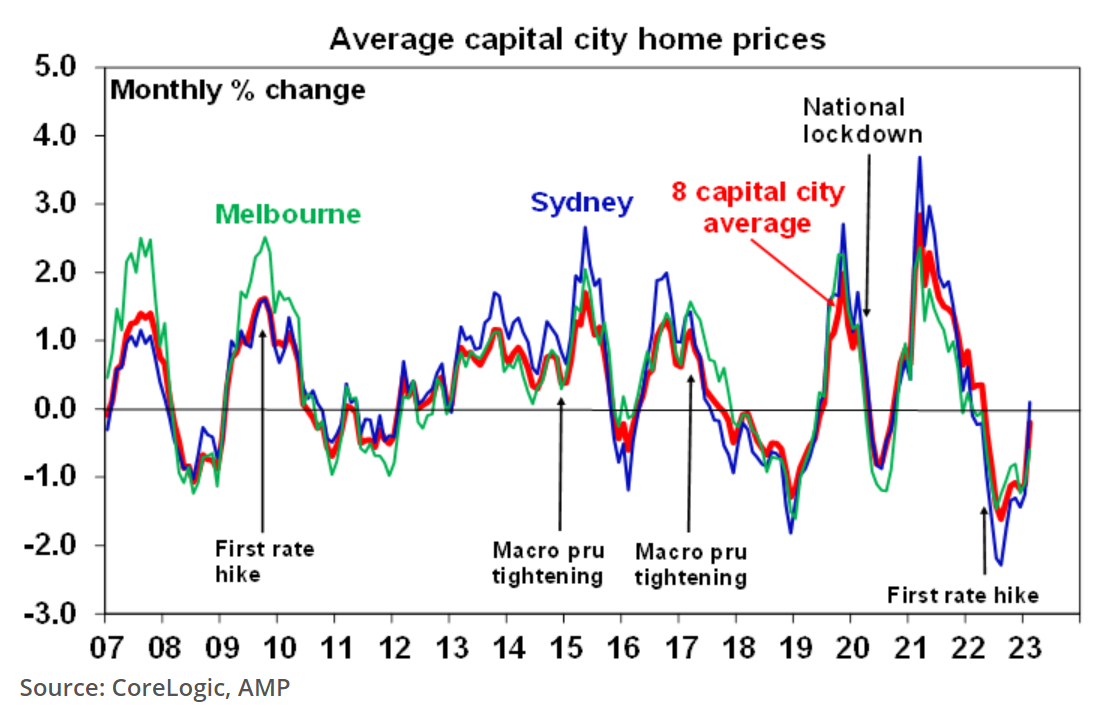

Oliver also notes that “the 2010-12 and 2017-19 price fall cycles saw periods where falls moderated or partially reversed only to resume falling”:

I made similar arguments last week.

To cut a long story short, this month’s 0.25% rate hike from the RBA will not be properly reflected in CoreLogic’s daily dwelling values index. The RBA has also given strong guidance that it will lift interest rates further in the months ahead.

These rate hikes will reduce borrowing capacity and, therefore, drive further falls in home values.

There are also more than 800,000 fixed rate borrowers who will reset to variable rates this year. And according to KPMG estimates, a borrower with an average mortgage of $600,000 will face a $16,500 increase in their annual repayments once they revert from their cheap pandemic fixed rate mortgages to variable.

Therefore, in addition to borrowing capacity continuing to shrink, there is also likely to be a material increase in forced sales, which should send prices lower.

I still believe house prices will rebound late this year after the RBA starts cutting rates.

There is also a decent likelihood that APRA will this year reduce the mortgage repayment buffer, thereby increasing borrowing capacity and helping to drive a late 2023 house price rebound.