The US Federal Reserve raised rates 25 basis points overnight but its was Fed Chair’s Powell quite dovish comments that sent risk markets higher and the USD pushed down considerably against the currency majors. Euro was pushed almost through the 1.10 handle while the Australian dollar matched its recent high above the 71 cent level. US bond markets were somewhat volatile with 10 year Treasury yields pulling back sharply below the 3.5% level while the commodity complex saw oil prices retrace as well despite the weaker USD, with Brent crude finishing just above the $83USD per barrel level. Gold put in a new monthly high to finish this morning just above the $1950USD per ounce level in a one way session.

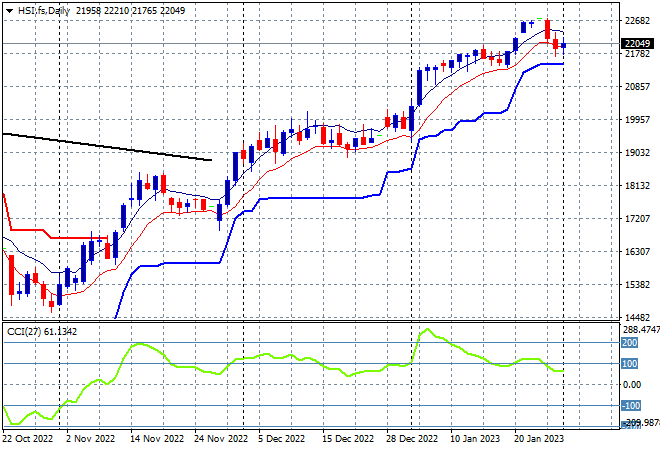

Looking at share markets in Asia from yesterday’s session where mainland Chinese share markets were a bit over the place but finally gained momentum to the upside in afternoon trade with the Shanghai Composite up nearly 1% to 3286 points while the Hang Seng followed suit, gaining 1% to get back above the 22000 point level. The daily chart had shown a clear breakout after building up a series of steps with daily momentum well overbought and ready for new highs but the 23000 point level maybe yet be far to reach. Keep an eye on ATR support next:

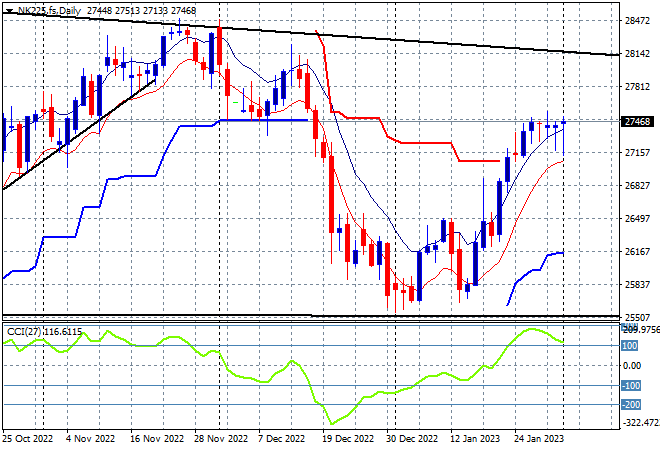

Japanese stock markets also went nowhere again, with the Nikkei 225 closing nearly dead flat at 27346 points. After bottoming out at the 25000 point level the recent positive correlation performance with Wall Street was helping lift price action back to the November highs, but not yet above as resistance builds at the 27500 point level. Clearing daily ATR resistance and getting daily momentum back into overbought mode should set up a further move higher to the 28000 point level next, but price action is tightening up here: