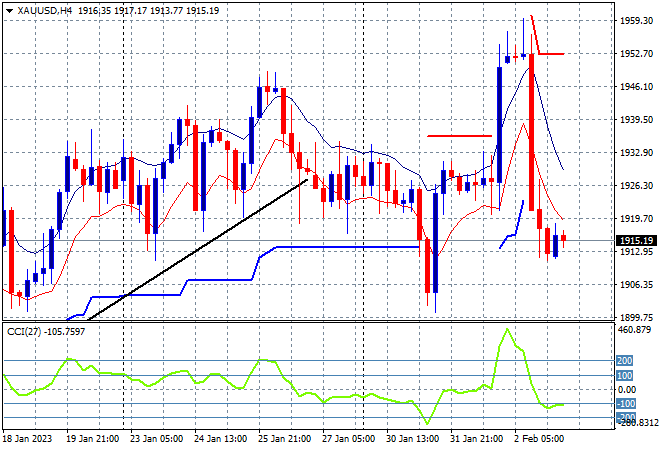

Outside of China, Asian stock markets are putting in a solid finish to the trading week, although hesitation abounds as we head into the US jobs print later tonight. Currency markets are still reacting to the overnight rate rises by the BOE and ECB with Euro pushed below the 1.09 handle while the Australian dollar is looking to put in a new weekly low as the RBA meeting beckons next week. Meanwhile oil prices are slipping as the OPEC+ meeting gets underway with Brent crude about to cross below the $82USD per barrel level as gold also consolidates after its big reversal overnight, currently hovering above the $1915USD per ounce level:

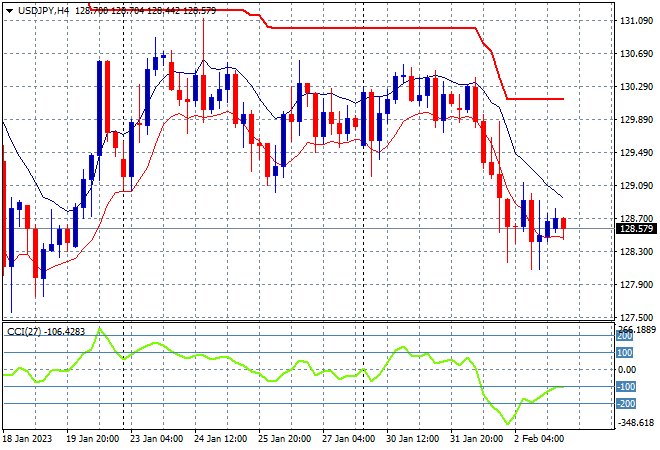

Mainland Chinese share markets are falling into the close with the Shanghai Composite down 1% to 3250 points while the Hang Seng is doing worse, off by more than 1.6% to be at 21604 points. Japanese stock markets are ending the week in a more positive mood with the Nikkei 225 closing 0.3% higher at 27438 points with the USDJPY pair consolidating somewhat from its recent losses, hovering at the mid 128 level:

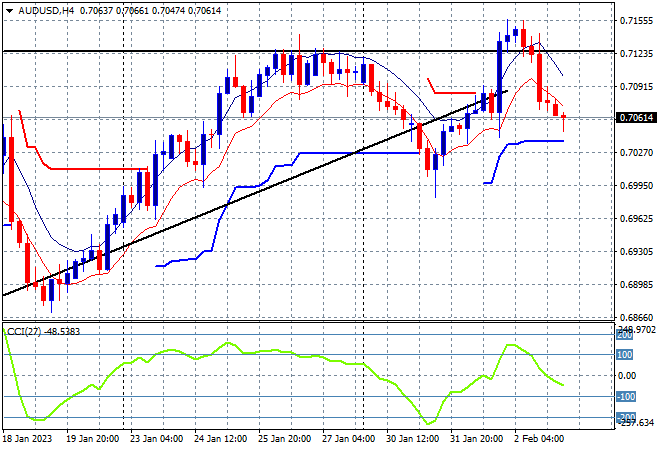

Australian stocks were the best performers in the region, with the ASX200 closing 0.6% higher to extend its gains above the 7500 point level, closing at 7558 points. The Australian dollar has retraced further from its overnight reversal in the wake of the ECB/BOE rate rises, falling further below the 71 handle as it looks to end the week on a lower note:

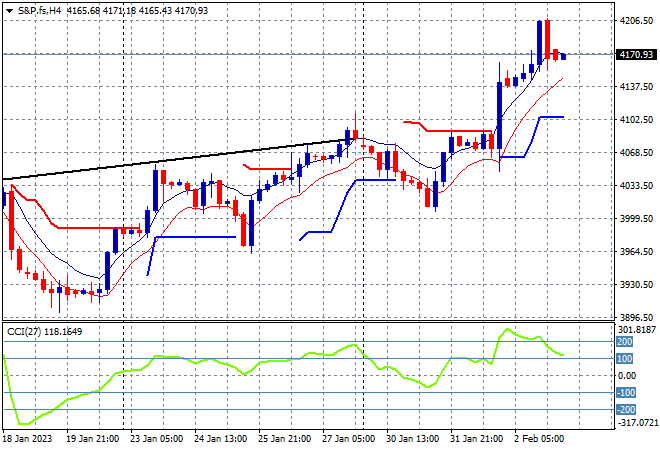

Eurostoxx and US futures are holding on to their respective gains from last night with the S&P500 four hourly chart showing price action still well above the psychologically important 4000 point zone, following the Fed’s dovish moves. Short term momentum is now extremely overbought and could retrace from here:

The economic calendar finishes the week with the most important release on the calendar, US unemployment AKA non-farm payrolls.