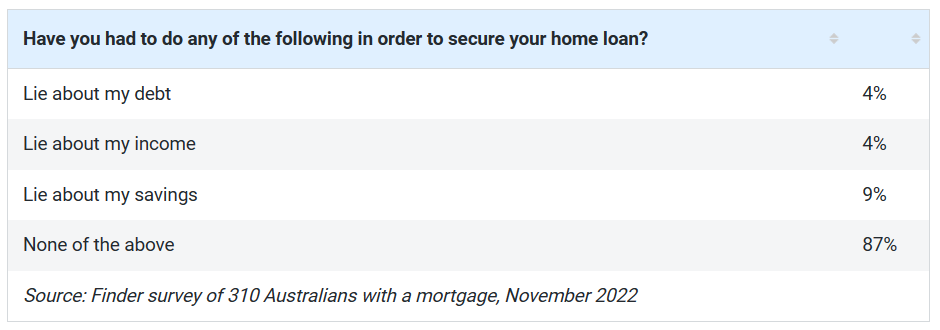

A Finder survey of 1114 respondents found that at least one in eight lied on their home loan application forms, with 310 of these respondents holding a mortgage.

If the survey results held across the population, it would mean roughly 430,000 mortgage holders falsified information pertaining to their home loan application.

Nearly one in 20 mortgage holders that admitted they falsified their application lied about their income or the amount of debts they are carrying.

Finder home loans expert, Richard Whitten, warned that these ‘liar loans’ increase the risk of a mortgage holder falling into stress.

“While the lies might go unnoticed – the financial burden of an unaffordable loan could create a lot of stress”, Whitten said.

“Legality aside, you’re putting yourself in a risky position if you lie on your application and borrow more than you can afford”.

It also increased the chances that if a borrower fell behind in their repayments, they could lose their homes.

“While small inaccuracies may not be the end of the world, if a lender finds a big discrepancy in the figures you’ve given them or you’ve outright lied about your financial position, the consequences could be severe”, Whitten said.

“Home loan contracts typically contain wording around providing misleading or incorrect information to a lender. In the worst case, lying on a mortgage application is grounds for a default event, meaning the lender could sell your property”.

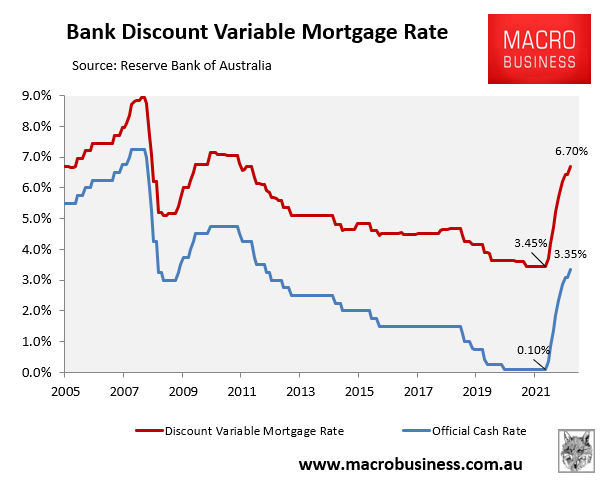

With the Reserve Bank of Australia (RBA) lifting the official cash rate (OCR) by 3.25%, and variable mortgages by a similar amount, the 2.5% mortgage repayment buffer that was in place until October 2021 (now 3.0%) has already been breached:

This means that most households that borrowed in 2021 or early 2022 at rock bottom mortgage rates are now ‘in the red’ from the RBA’s aggressive monetary tightening.

It also means that for every rate going forward, there will be increasing numbers of mortgage holders who are required to make higher repayments than they were tested for when they took out their loan.

Borrowers that took out ultra cheap fixed rate mortgages at around 2% are particularly exposed, as are those who lied on their loan applications to gain a mortgage or increase their borrowing limit.

That said, the bigger factor that will determine whether there is a wave of housing defaults is the strength of the labour market.

If mortgage holders keep their jobs, most will weather the interest rate hikes okay.

But if unemployment spikes, then the number of housing defaults will rise accordingly.

If you are looking to save thousands of dollars in mortgage repayments, try the Compare n Save mortgage comparison tool. It takes less than a minute. And if you wish to refinance, the process is easy.

Compare 100s of loans in seconds, hassle free…..

and when you’re ready to apply, we’ll manage the process for you.

I Want To Refinance

I Need A Loan