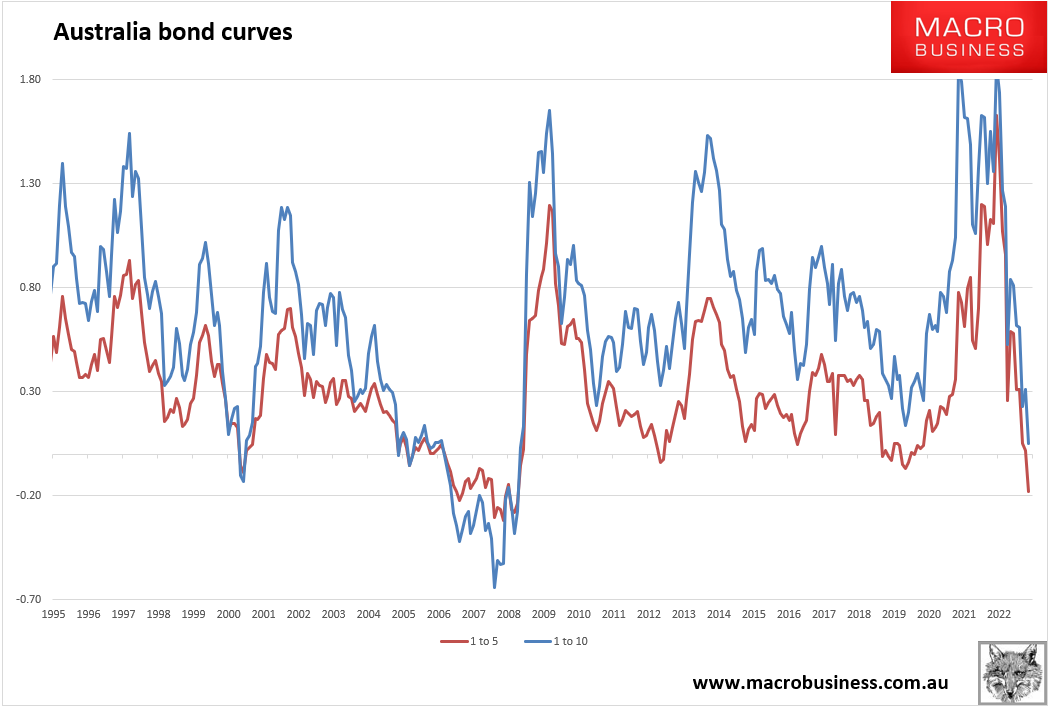

A combination of data releases (weak in Australia, strong in the US) last week squashed yield curves. Australia 1-5 and 1-10 curves are fast pricing worse than per-capita recession:

The 2-20 curve is still lagging but there is no mistaking the trend and it is also at a new low of 17bps:

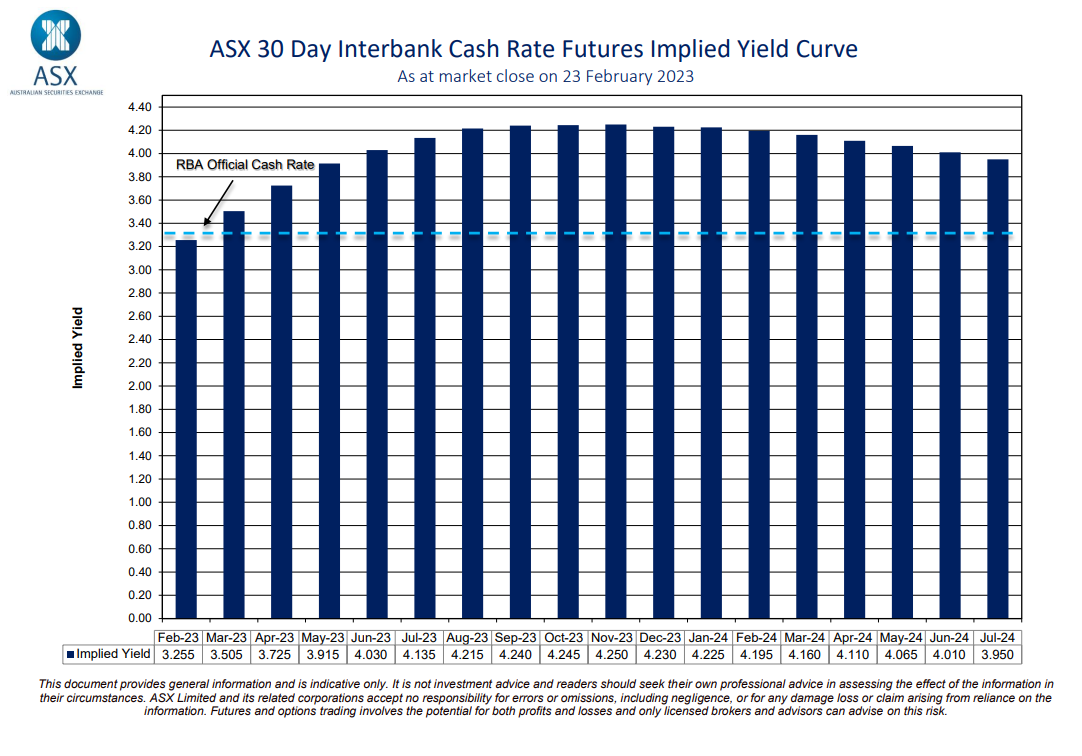

How high will yields go? Short-end Aussie yields have nearly fully priced two more rate hikes. Interest rate futures are pricing another one and a half on top and only very slow cuts afterwards:

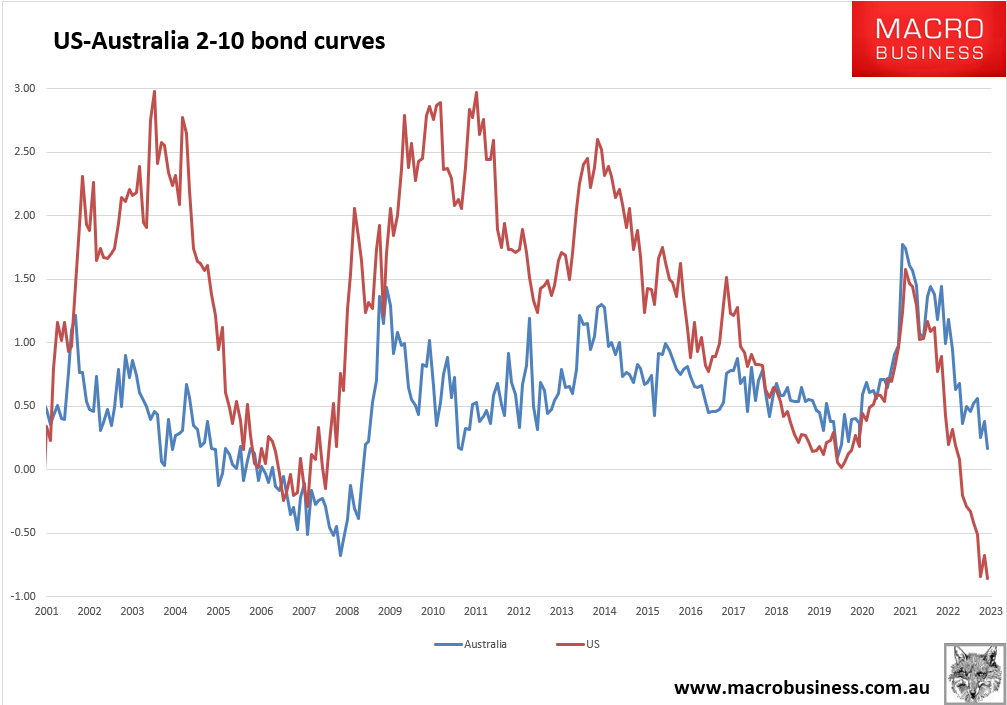

My own view remains that the Australian cycle is swiftly catching down to that of the US. Weakness at home may even overtake the US if the RBA keeps hiking.

Locally, the employment situation has definitely deteriorated. Though how much of that is demand weakness and how much is the influx of cheap foreign labour is an open question. Another is whether the current house price rebound firms up which is unlikely.

Barring that, my view is the short end of the Aussie curve is close to peaking. It has already priced two more hikes going into the fixed-rate mortgage cliff. The long end is more influenced by the US so the curve here could lift a little more until the Fed snuffs out any rebound.

On that basis, Credit Agricole mulls how high duration yields might go.

We expect front-end Treasury yields to march higher, gravitating towards 5.00% as the market seems convinced the Fed will continue hiking at least through mid-year and the prospects of easing later this year have diminished.

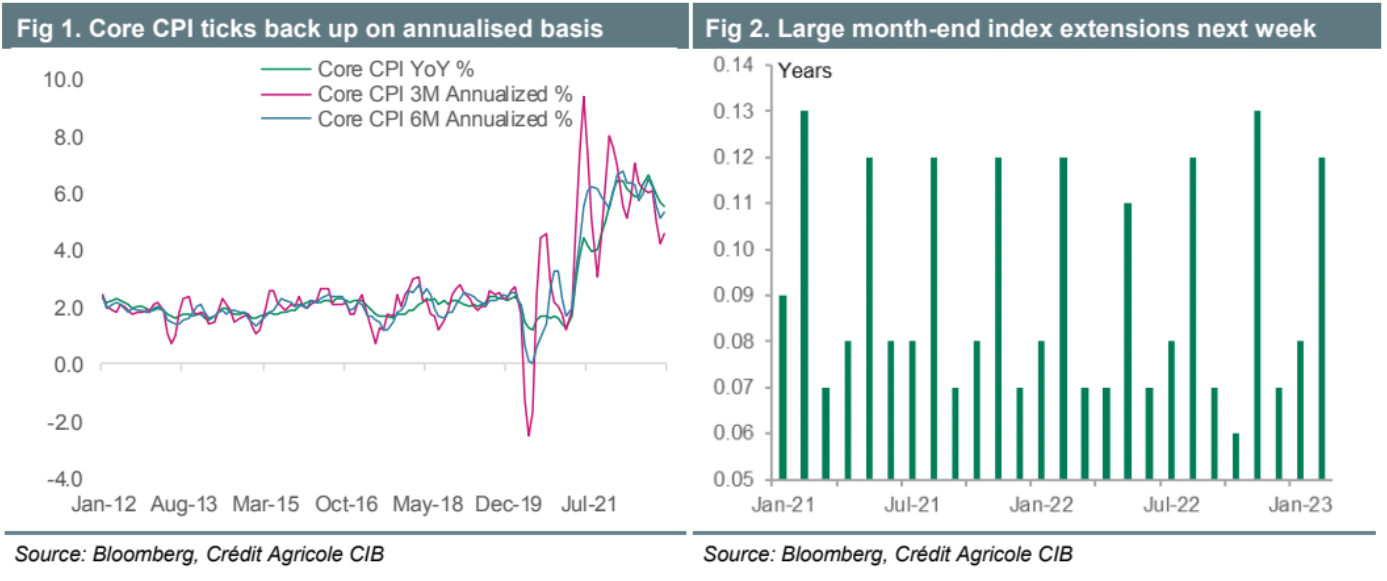

We expect front-end Treasury yields to march higher, gravitating towards 5.00% as the market seems convinced the Fed will continue hiking at least through midyear and the prospects of easing later this year have diminished. Inflation has remained too high for Fed’s comfort, as evidenced in the latest CPI and PPI reports. Although core CPI declined on a YoY basis from 5.7% in December to 5.6% in January, the recent trend is worrisome, as the 3M and 6M annualised figures actually ticked up (see Figure 1).

The inflation-driven nature of this cycle and the lack of labour market slack suggest that the Fed’s job of tackling inflation remains some way from over. The February FOMC minutes showed that “almost all” officials agreed to hike rate hikes by 25bp, with “a few” members favouring a larger 50bp hike. The latter is consistent with the latest comments by Cleveland Fed President Loretta Mester and St Louis Fed President James Bullard, where they saw a compelling case for a 50bp rate increase. The market is now pricing a terminal rate at 5.38%, and still about 20bp easing in H223.

We think 10Y yield will likely trade above 4.00%, as strong growth and stubbornly high inflation pressurise the entire yield curve upwards – less so in the long end than in the short end. While the yield curve inversion is already at record levels, we expect more to come. 2-10Y could go to -100bp under continued hikes. Month-end index extension trades will be a focus next Tuesday, when the Treasury index is projected to extend by 0.12 years, which is in line with a refunding month end (see Figure 2). The TIPS index will extend by 0.13 years, as a result of the new 30Y supply earlier this month.

Expect house prices and stocks to keep falling if that is the case.