DXY broke support last night as the Fed failed to hawk up:

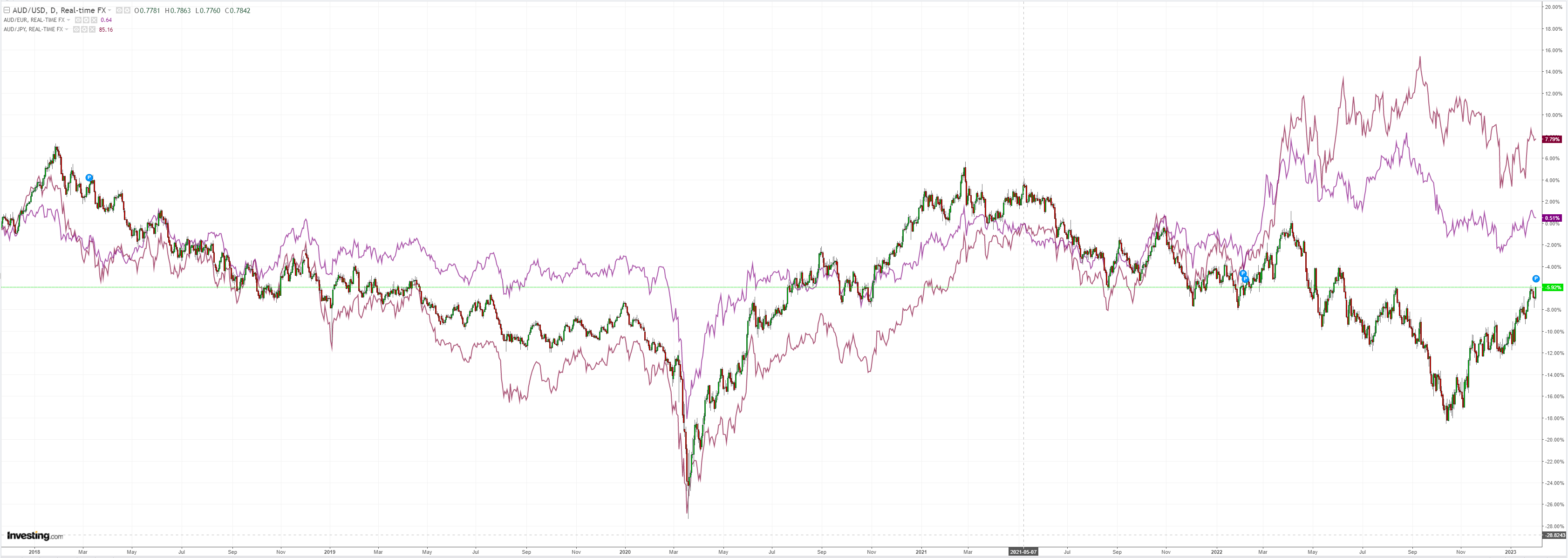

AUD to the moon, outpacing all DMs:

Gold up, oil down:

Advertisement

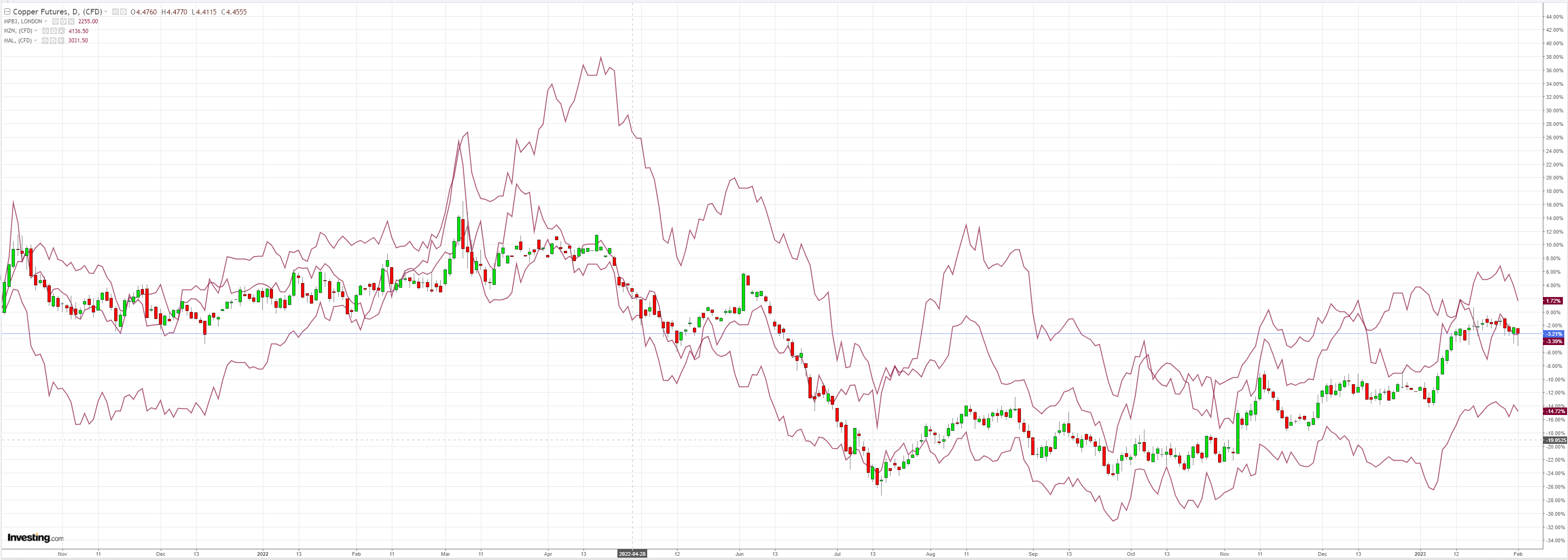

Metals down with oil:

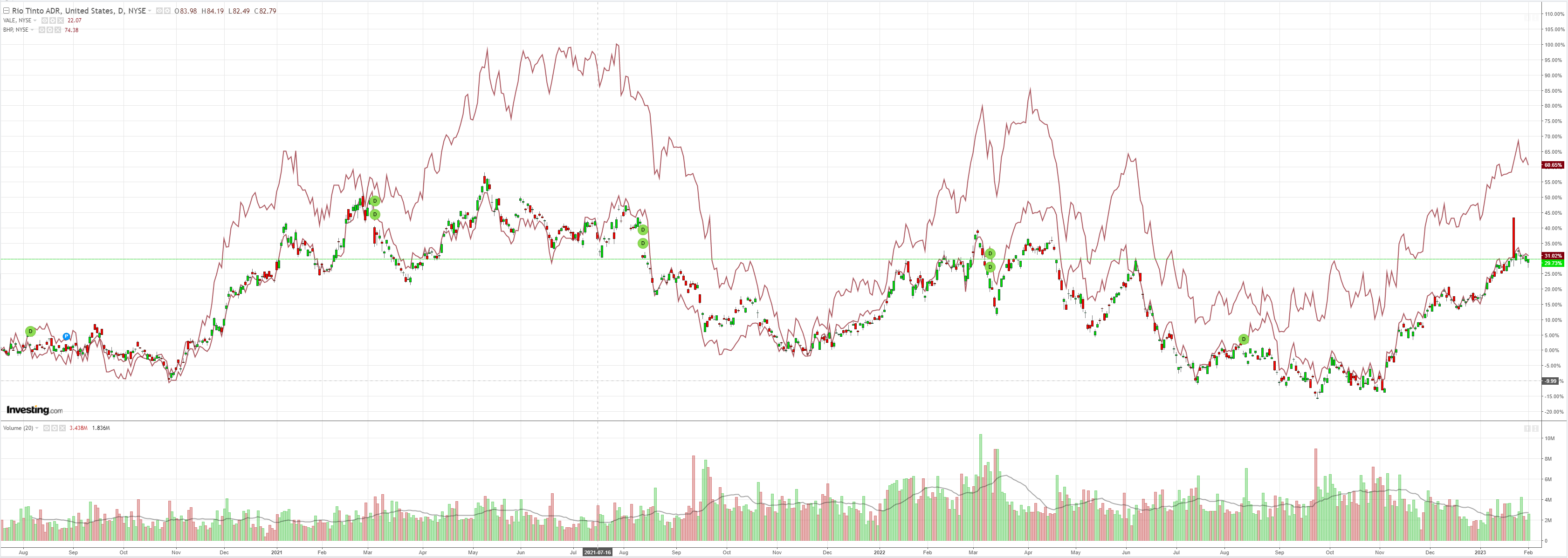

And miners:

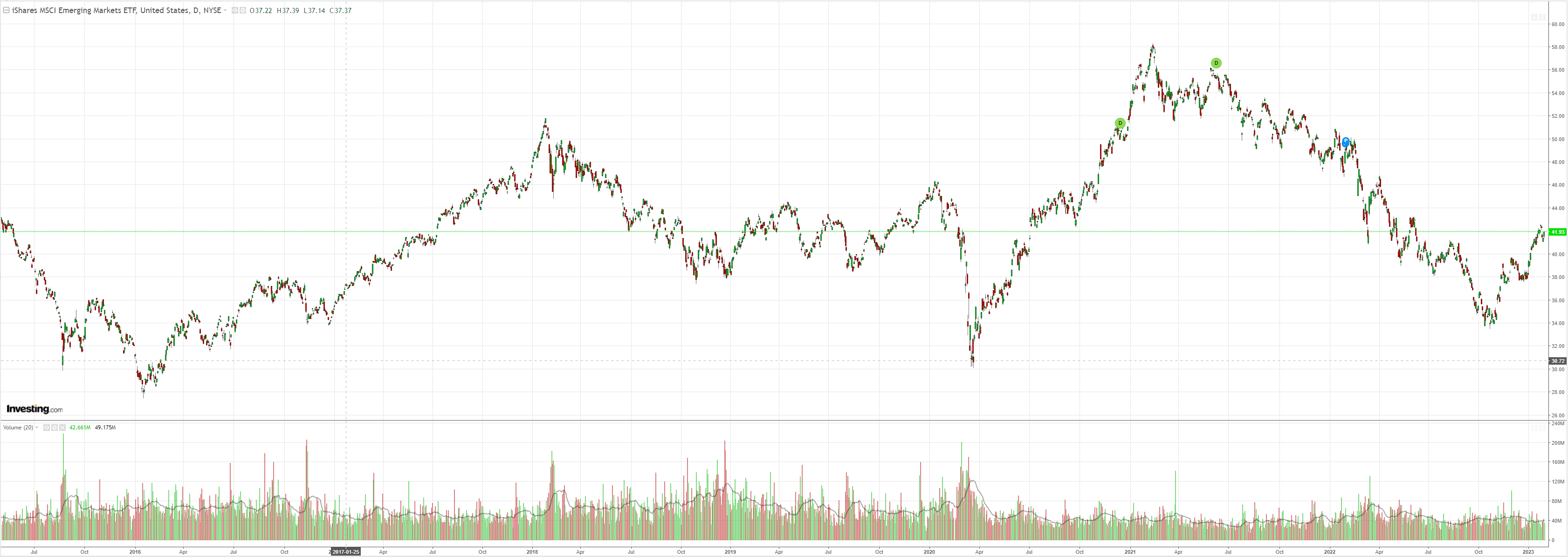

EM stocks firmed:

Advertisement

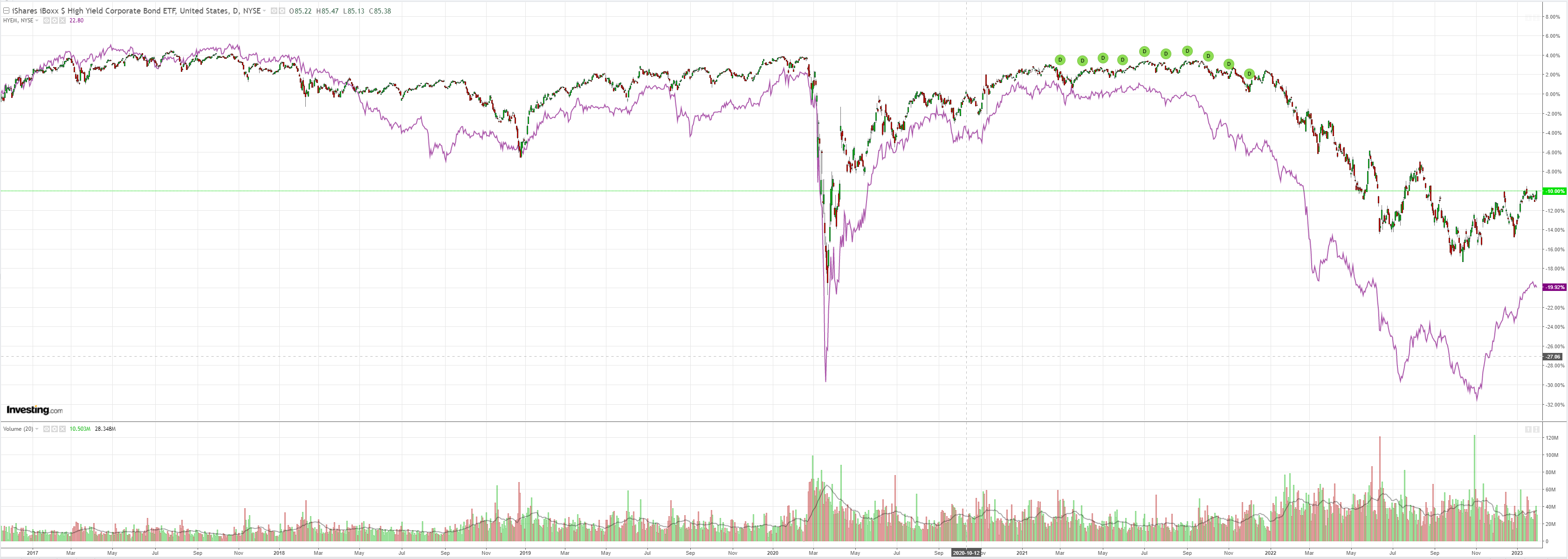

Junk went both ways:

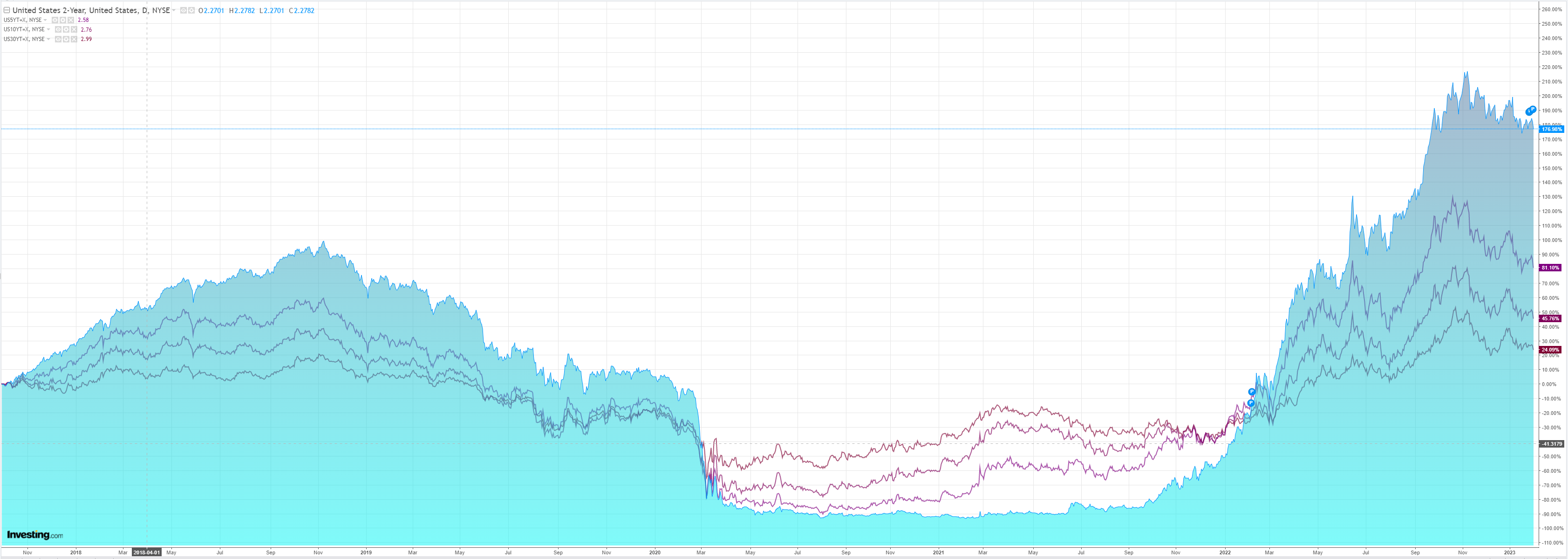

Treasury yields slumped:

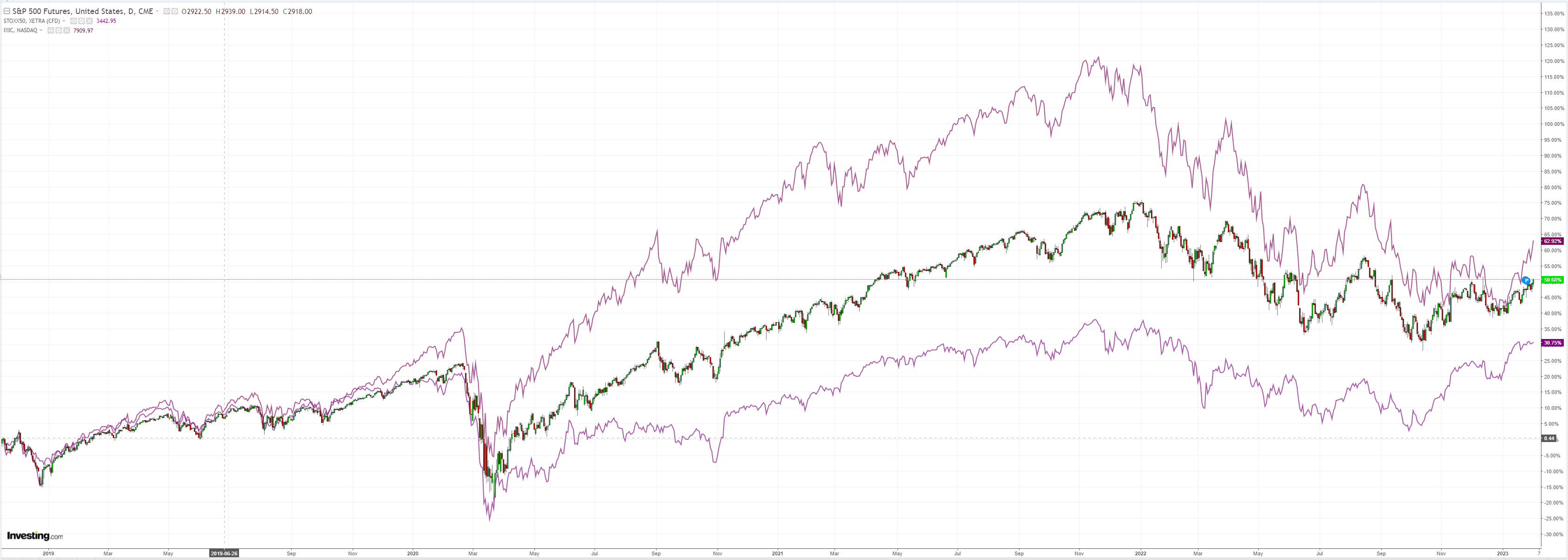

Stocks soared again:

Advertisement

US data was mixed with a weak ADP but strong job openings. The ISM recession deepened:

The January Manufacturing PMI® registered 47.4 percent, 1 percentage point lower than the seasonally adjusted 48.4 percent recorded in December. Regarding the overall economy, this figure indicates a second month of contraction after a 30-month period of expansion. The Manufacturing PMI® figure is the lowest since May 2020, when it registered a seasonally adjusted 43.5 percent. The New Orders Index remained in contraction territory at 42.5 percent, 2.6 percentage points lower than the seasonally adjusted figure of 45.1 percent recorded in December.

The Fed was hawkish in its release:

Advertisement

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to raise the target range for the federal funds rate to 4-1/2 to 4-3/4 percent. The Committee anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time. In determining the extent of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective.

Powell noted that financial conditions have tightened very significantly over the past year, and that “it is important that overall financial conditions reflect” monetary policy (which they don’t), but added that “our focus is not on short-term moves, but on sustained changes.

This is anything but the ‘hawkish’ rhetoric the market was expecting.

And just like that a furiously over-extended bear market rally becomes reflation and AUD shoots to the moon.

Advertisement

That is, until the 200bps of rate cuts priced for 2023/24 start to come out.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.