Australia’s superannuation system has come into the spotlight this year with AustralianSuper, HESTA and Aware Super among large industry players calling for a $5 million limit on account balances in order to improve equity and stem the cost of superannuation concessions to the federal budget.

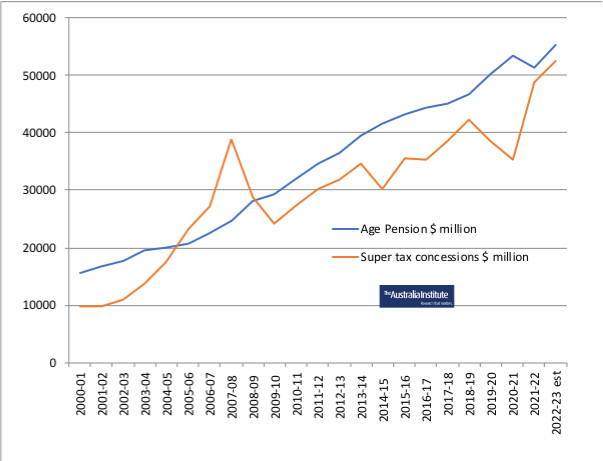

The debate followed analysis from The Australia Institute showing that superannuation tax breaks will cost the federal budget a whopping $52.5 billion in 2022-23. That is only slightly less than the $55.5 billion annual expenditure on the aged pension:

The cost of superannuation concessions is rising fast.

What few commentators realise is that the proposed $5 million limit on account balances is merely tinkering at the edges, and that the entire superannuation system has been designed to fail.

There are eight fundamental flaws in Australia’s superannuation system that have made it ineffective as a genuine retirements scheme, increased costs to taxpayers, and increase inequality.

1) Superannuation misses millions of people:

Compulsory superannuation contributions only apply to employees. It is voluntary for those that are self-employed or homemakers. It, therefore, automatically misses millions of people.

2) Balances at retirement depend on how long one works and how much they earn:

Related directly to point one, superannuation balances at retirement depend directly on how long one works and how much they earn over their working lives.

Superannuation, therefore, largely misses lower income earners and those with broken work patterns (e.g. mothers).

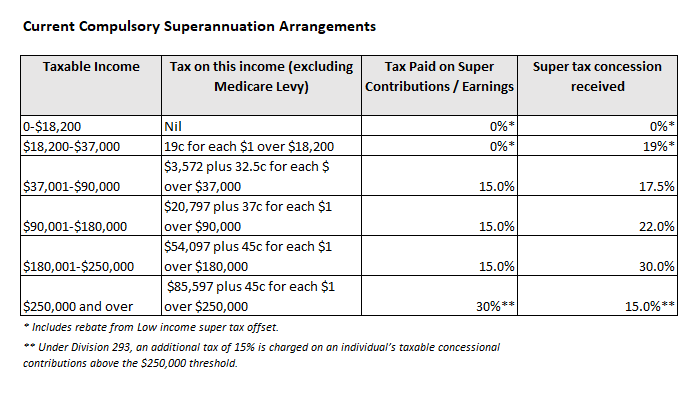

3) Most superannuation concessions go to where they are not needed (i.e. high income earners):

Australia’s progressive personal income tax system means that the 15% flat tax on superannuation contributions and earnings generally means those higher up the income scale receive the largest tax concessions:

Superannuation tax concessions generally favour higher income earners.

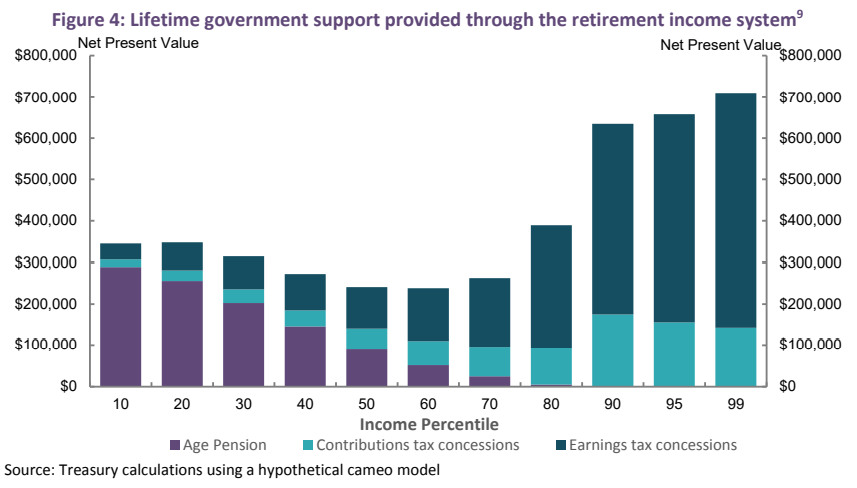

Moreover, because the size of one’s superannuation nest egg is also a function of how long one works and how much they earn (see point 2), the lifetime taxpayer support provided through Australia’s retirement system is heavily skewed towards higher income earners (see below Australian Treasury chart):

The wealthy receive far greater retirement support than the poor.

Australian taxpayers spend more than twice as much supporting the retirements of the top 1% of income earners than they spend supporting someone on the aged pension, according to the Treasury.

The top 1% of income earners are projected by the Australian Treasury to receive more than $700,000 in superannuation concessions over their working lives. That is roughly 14-times the $50,000 of concessions received by the bottom 10% of income earners.

And since men typically earn more and have less interrupted working lives than women, they also accumulate larger superannuation nest eggs.

4) Superannuation can be spent before retirement:

Superannuation can be spent at the age of 60, which is many years before the official retirement age of 66 (rising to 67).

This means that Australians can retire at 60, spend their superannuation, and then fall back on the aged pension.

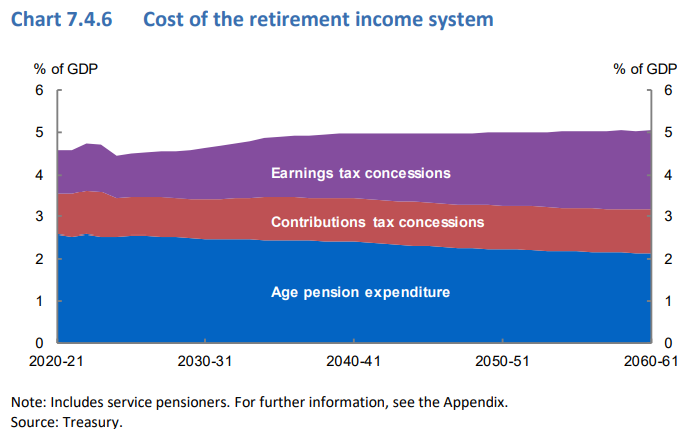

5) Superannuation will cost more than the aged pension over the long-run:

The Australian Treasury’s Intergenerational Report projected the cost of superannuation concessions to overtake the cost of providing the aged pension by around 2040:

Superannuation to cost more than the aged pension.

6) Superannuation locks-in intergenerational inequality:

The Australian Treasury’s Retirement Income Review complained that superannuation has transformed into a wealth accumulation and transfer scheme that is increasing inequality.

“Inheritances are significant, representing the transfer of wealth from one generation to another. They are not distributed equally and increase inequity within the generation that receives the bequests”, the review noted.

“Most people die with the majority of wealth they had when they retired. If this does not change, as the superannuation system matures, superannuation balances will be larger when people die, as will inheritances”, the review warned.

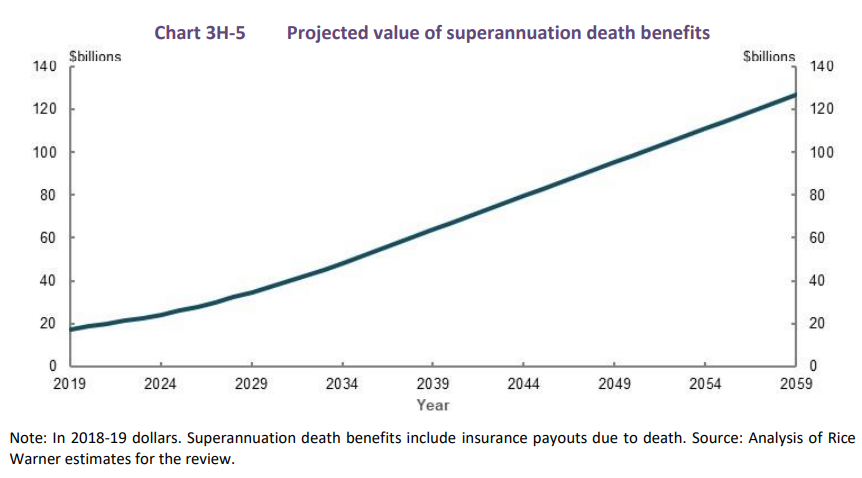

The review included the below chart showing that “superannuation death benefits are projected to increase from around $17 billion in 2019 to just under $130 billion in 2059”:

Superannuation inheritances soaring.

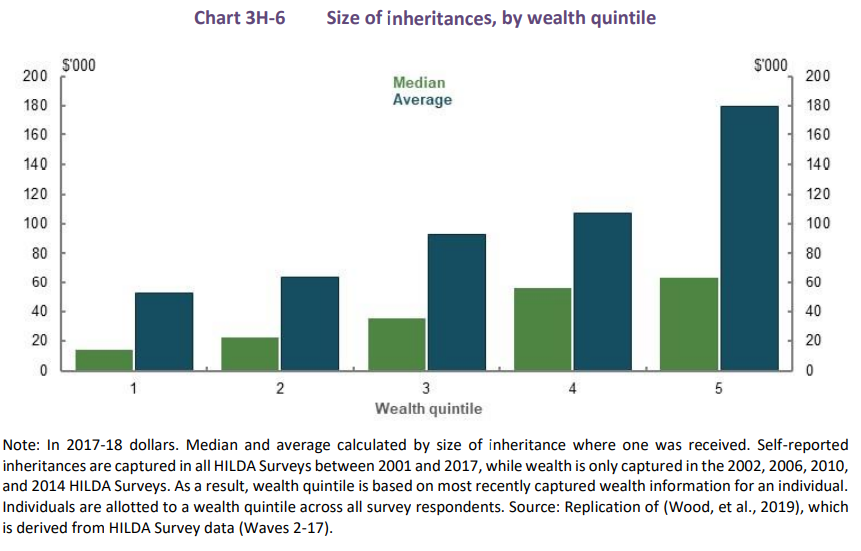

These inheritances are also unequally distributed, with “wealthier people tending to receive larger inheritances than those with lower wealth”. Accordingly, superannuation inheritances “increase intragenerational inequity”, according to the review:

Superannuation inheritances increase inequality.

7) Australia’s superannuation system is highly inefficient:

Management fees are among the highest in the world with Australian households spending far more each year on superannuation fees than they do on electricity.

The number of people employed in Australia’s superannuation industry is also wasteful, dwarfing Australia’s entire welfare system and is on par with the entire defence force and its bureaucracy.

8) Superannuation lowers wage growth:

Compulsory superannuation contributions are paid by employers in lieu of wages. Therefore, superannuation lowers wage growth and is especially troublesome for lower income earners struggling to pay their bills.

Aged pension system far more efficient and equitable than superannuation:

Australia’s compulsory superannuation system misses on almost every policy mark:

- It is poorly targeted and misses those in genuine need.

- It costs the federal budget far more than it saves in aged pension costs.

- It reduces workers’ take-home pay.

- It entrenches inequality by encouraging tax avoidance and wealth accumulation by the rich and their heirs.

The superannuation system effectively takes the disparities in working-life incomes and magnifies them in retirement, enshrining inequality.

By contrast, the aged pension suffers none of these flaws and should be considered Australia’s genuine retirement pillar.

The aged pension is universally available for those most in need. It is not based upon how much one works or earns prior to retirement. And the pension is not subject to market risk.

Given the massive cost, inefficiency and poor targeting of superannuation concessions, it would make sense to unwind these concessions and plough the billions in budget savings into a more generous universal aged pension.

This would never happen of course. The superannuation industry is too large and powerful and would bring down any government that dared tried to curtail it.

So instead, the Labor Party has doubled down and thrown more money into the broken system by raising the superannuation guarantee to 12%.