Westapc’s Red Book is illustrating deeply depressed property sentiment. Typically this matches bottoms in price cycles. I don’t think that price falls are over as 1-2 more rake hikes arrive and the fixed-rate reset causes havoc. But I am also of the view that the economy is going to stall badly as the year progresses, inflation crash, and the RBA be forced to cut deeper than most.

As they say, buy when others will not, and now’s the time to be making lowball offers. Before the market sniffs out the next round of cheap credit and moves higher overnight.

Your major risk is another round of global inflation arising from oil.

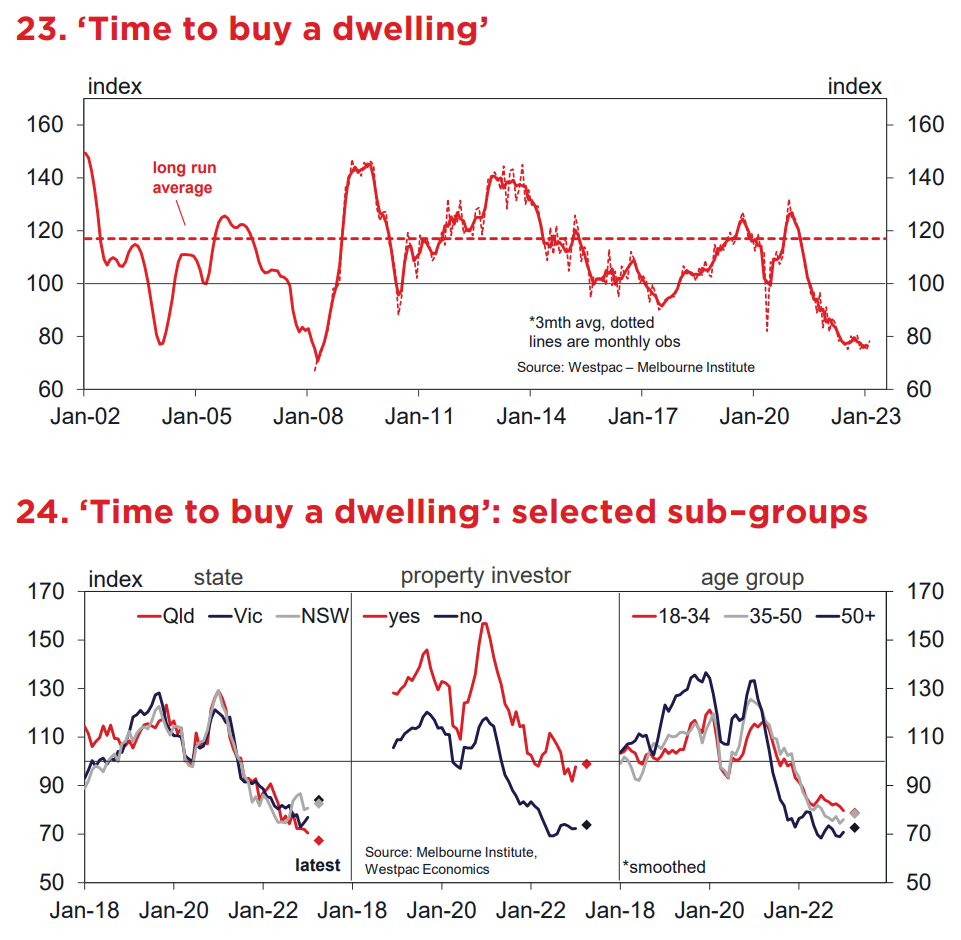

Consumer house purchase attitudes remain extremely weak. The ‘time to buy a dwelling’ index has lifted 3.8% over the last 3mths but remains mired at historical lows below 80.

― The index has been tracking very low levels for exactly a year now, an unusually long period of weakness by historical standards. Since the mid–1970s, most cycle lows have lasted for less than six months. Indeed, the only other instance when the index has been sustained below 85 for this long was during the early 1990s recession. Even then, the run only lasted for thirteen months, albeit with sentiment reads much weaker than we are seeing now (including an all–time low of 44.8!).

― Of course, there is no set time on how long homebuyer sentiment stays weak. As noted in the past, the index tends to track aff ordability, i.e. the income required to raise a deposit and meet mortgage repayments on a new purchase. Despite price falls, affordability has seen little improvement due to the impact of higher rates on repayments. This will remain the case through to mid–2023, suggesting any lift in sentiment will come late in the year.

― Interestingly, the detail shows recent gains have been led by NSW and Vic, where price declines have seen more of an improvement in affordability, and investors, who are less sensitive to affordability considerations.

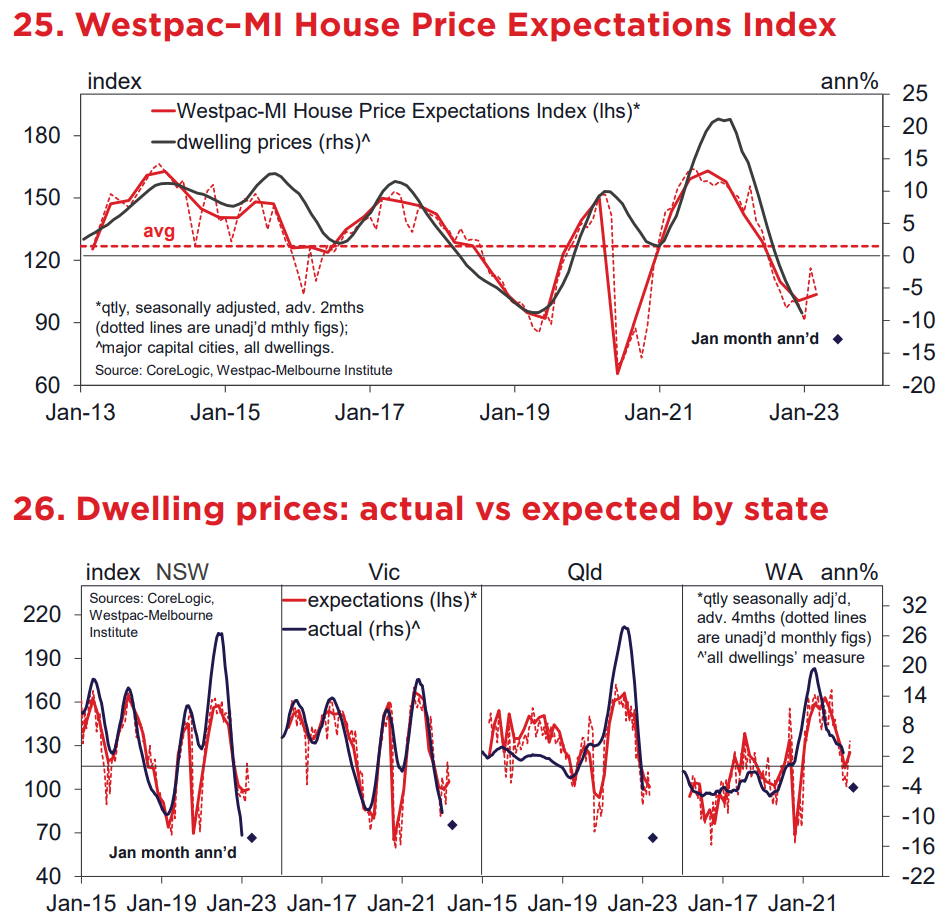

― Consumer house price expectations have lifted slightly since late last year, the Westpac Melbourne Institute House Price Expectations Index up 5.4% to 104.4 over the 3mths to Jan.

― The result is a mix of strong and weak. On the strong side: expectations are back above the 100 ‘gain–line’ – meaning that more consumers expect prices to rise than fall – and well above historic lows in 2020, 2019, 2008 and 2004–05. On the weak side: expectations are still well below their long run avg (126.8) suggesting there is a long way to go before prices are likely to stabilise. Overall, the picture remains consistent with further price declines near term.

― The sub–group detail shows some interesting nuances, particularly around tenure. Gains over the last 3mths have been led by homeowners, but from a markedly weaker starting point. At the same time, price expectations amongst renters have eased a touch. There may be some ‘wishful thinking’ at play here.

― By state, expectations have seen a more meaningful lift in WA, where the price correction has been much milder to date. Consumer house price expectations in the state are only 12.6pts below their long run avg in WA, compared to a 35–40pt gap in other states. Qld is the only major state still recording index reads in net pessimistic territory, below the 100 level.