It is quite something to watch as Aussie house prices crater while the stock of credit is still growing strongly. But that’s the importance of Delta. Oftentimes it is the rate of change that matters in economics and markets, not the levels.

Put another way, it is the flow of credit that matters to prices, not the stock.

Westpac has more on how fast mortgage demand is drying up.

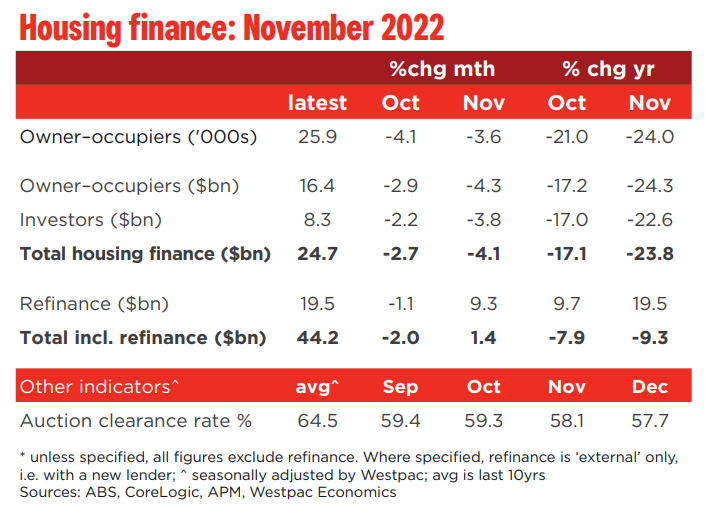

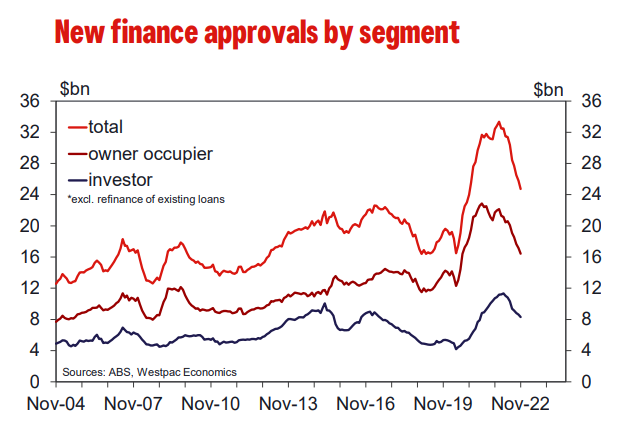

• Housing finance approvals continued to move lower in Nov, the total value of new loans (ex re-finance) down a further 4.1% in the month. Approvals are now 24% below their Jan peak, although they remain well above their pre-COVID levels and previous peaks in 2017. The result was a touch softer than our expectations.

• The detail showed broad weakness with all major segments and states recording declines in the value of new finance. Refinance was a notable exception, approvals for external refihitting an all-time high of $19.5bn, up 9.3% in the month and 19.5%yr – likely reflecting both borrowers seeking out better deals to cope with sharply higher interest rates and intense competition between lenders.

• The value of owner occupier loans fell 4.3%mth to be down 24.3%yr. The detail showed slightly bigger falls for construction loans (–7%), loans for the purchase of newly built dwellings (–5.5%), and loans to first homebuyers (–5.7%). Interestingly, additional data shows a much higher take-up of fixed rate loans amongst first homebuyers in recent years, accounting for 45% of the value of loans to the segment in 2020 and 2021, compared to 34% for non first homebuyers (covering both owner occupiers and investors). This implies recent first homebuyers have a higher exposure to ‘reset shock’ as loans roll off fixed rate periods.

• The value of new investor loans fell 3.8%mth to be down 22.6%yr, still tracking a slightly milder cycle.

• The state detail showed a slightly bigger decline in Vic (–5.5mth) and slightly milder falls in NSW (–2.9%mth), Qld (–1.6%mth), WA (–2.8%mth) and SA (–2.4%mth). Approvals are showing double-digit declines in all states, led by a 30% fall in NSW, 20-25% declines in Vic and Qld and somewhat milder falls in SA (–17%) and WA (–12%).

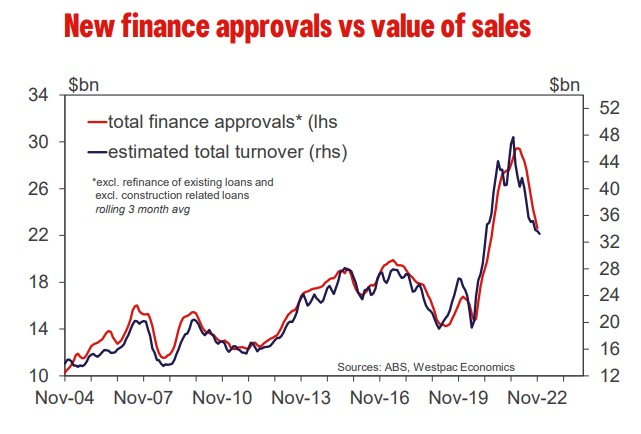

• Overall, the housing finance data remains in line with the broader picture of a deepening and broadening housing market correction. There is little let-up in sight with other updates showing the housing market correction remains firmly entrenched and the RBA expected to continue ratcheting rates higher in early 2023. In terms of the stock of housing credit, the new lending data suggests the slowdown in credit growth from a peak of 7.9% in mid-2022 to 6.9% in Nov will extend to the low 4s by mid-2023.

The only way I can see Westpac’s forecast of the stock of credit bottoming out at 4% is if the RBA cuts sharply in H2. The great fixed-rate mortgage reset is about to begin.