The global gas crisis is over. European gas inventories are huge and economic stress is about to unwind. John Kemp:

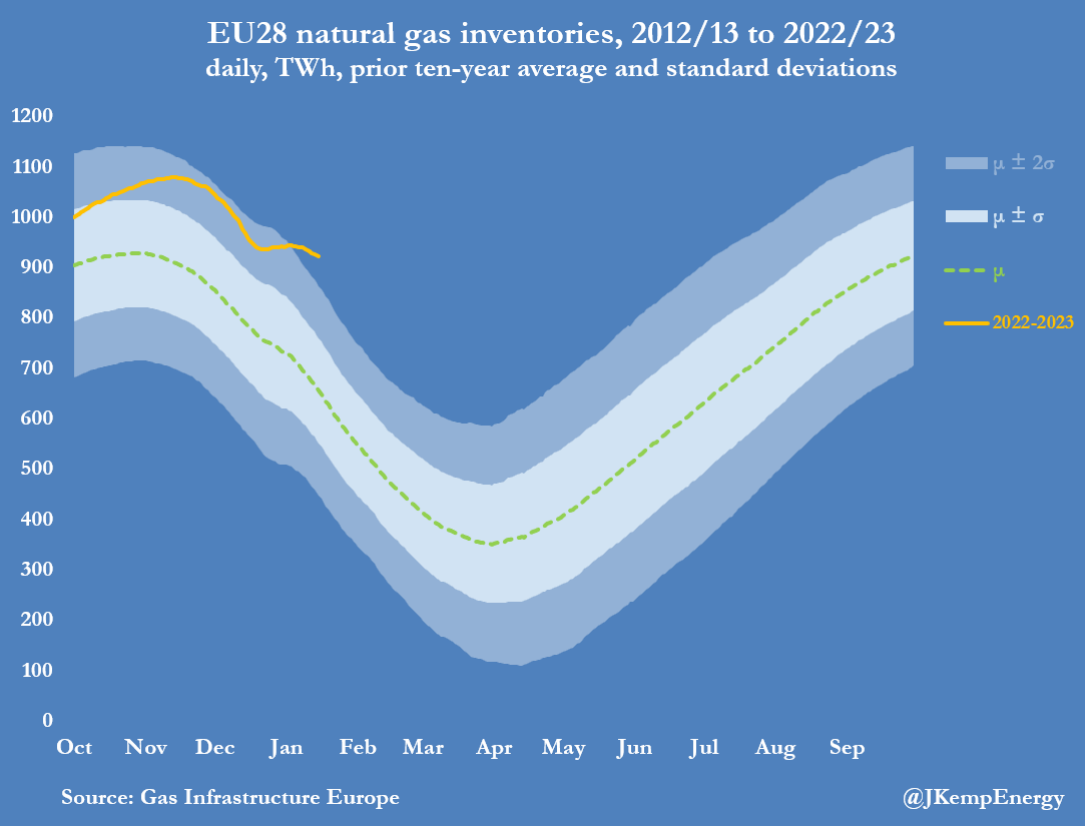

Inventories are on course to end the winter at the highest level on record, with storage sites still more than 54% full.

Prices have already slumped to redirect more liquefied natural gas (LNG) to other regions of the world, encourage more consumption in Europe and stem inventory accumulation.

Futures prices for deliveries in March 2023 have halved to €56 per megawatt-hour from €110 on December 19 and €177 at the start of winter.

Lower prices will buy back some consumption lost earlier this winter from the most price-sensitive customers directly exposed to wholesale markets, mostly power producers and energy-intensive industrial users.

Gas-fired electricity generators are likely to operate for more hours at the expense of coal-fired and fuel oil-fired competitors, absorbing some of the surplus.

Manufacturers of fertilizer, iron and steel, ceramics, glass and chemicals, as well as non-ferrous smelters, are likely to restart some idled capacity if prices remain lower.

Futures for gas delivered to Northwest Europe are now trading at a discount to gas delivered to Northeast Asia, from a premium over €11 per megawatt-hour on December 19 and almost €43 at the beginning of winter.

Relatively lower European prices should reduce the incentive to maximise LNG inflows and redirect more gas to importers in East and South Asia, which will also limit the further build up of a surplus in Europe.

It is one-way traffic for Asian LNG futures:

US gas prices have crashed back to normal ranges:

Advertisement

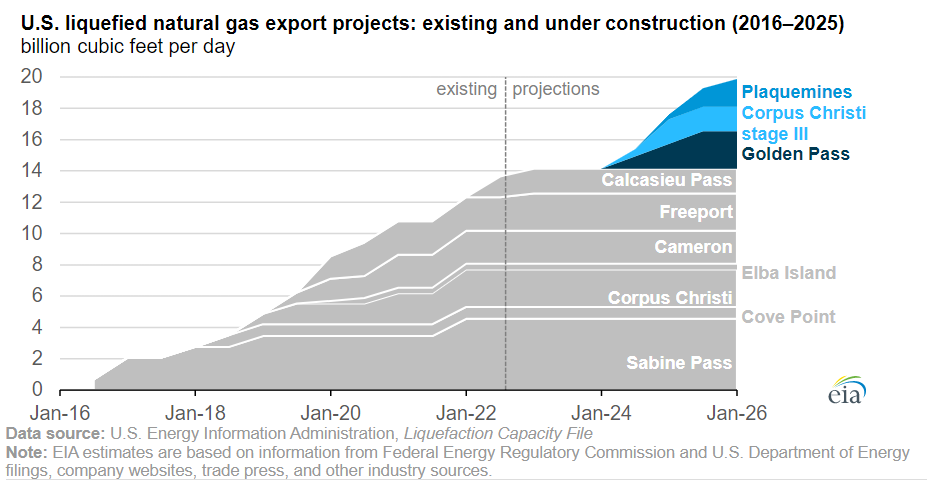

And there is more gas coming. Over the next 18 months, the US will pump out an additional 42mtpa in supply:

Plus the return of Freeport in H1 this year meaning a supply surge of 57mtpa. There are more than 100mpta of further US projects in development.

Advertisement

Qatar then adds another 50mpta in 2027.

All Russia has achieved is the stranding of its second-largest commodity asset. But even it has more LNG coming via the Arctic project of 20mtpa starting this year.

Then there are multiple Floating LNG projects around that can ramp as well.

The Ukraine War gas shock occurred amid a global gas glut. All that was required to fix it was a reorientation of supply chains. That is already largely achieved thanks to US LNG shifting to Europe and some Russia to Asia.

Advertisement

There is still a risk of a price pop next winter in the northern hemisphere if it is cold, but it will be brief, and everybody, everywhere suddenly has gas and lots of it.

The most competitive household gas prices on the east coast are already as high as Jim Chalmers’ worst-case scenario, as retailers hike prices by a further 20 per cent from next month.

The Australian’s analysis of current market offers from Origin, AGL and EnergyAustralia shows prices have increased by 30 per cent in Queensland, 22 per cent in NSW, and 19 per cent averaged out across those states, Victoria and SA over the past year.

Households are set to come under even more pressure, with EnergyAustralia on Tuesday announcing its residential gas customers in Victoria on variable market contracts would see their bills increase by an average of 26.7 per cent from February 1.

…The price revelations come as top gas producers say they won’t finalise new supply contracts for 2024 until the Albanese government unveils its controversial mandatory code of conduct.

The government failed to ease industry concerns about its energy market intervention after the consumer watchdog released new compliance guidelines for the temporary gas price cap on Tuesday. Gina Rinehart-controlled Senex warned that uncertainty over the mandatory code of conduct could hobble gas deals spanning nearly two decades.

Advertisement

Gina also dropped Netball Australia over symbolism. The evidence suggests that her decisions are ideological.

The ACCC is now out with its governance regime for the gas cartel:

The ACCC has today published interim compliance and enforcement guidelines for the gas industry on the new Gas Market Emergency Price Order and explaining how the ACCC intends to exercise its enforcement role.

In December 2022, the Australian Government’s Gas Market Emergency Price Order introduced a temporary price cap of $12 per gigajoule (GJ) that principally applies to gas sold by east coast and Northern Territory gas producers and their affiliates to wholesale customers in Australia. The price cap will apply for 12 months.

“Our guidelines are intended to support the gas industry with their obligations to comply with the new laws, so the country experiences the intended benefits from these emergency measures,” ACCC Chair Gina Cass-Gottlieb said.

“While our primary objective is to achieve compliance with these laws, we are ready to exercise our enforcement powers in response to any alleged contraventions, particularly if we become aware of conduct that may be intended to circumvent the price cap.”

The maximum penalty for a company that breaches the emergency price order is the greater of $50 million or three times the value of the benefit obtained, or, if that value cannot be determined, 30 per cent of the company’s turnover during the period it engaged in the conduct.

The price cap generally does not apply to supply contracts entered into before 23 December 2022 but may apply if a price provision in an agreement for supply in 2023 is varied. The price cap does not apply to sales of gas intended for international export.

The Gas Market Emergency Price Order allows gas producers and their affiliates to apply to the ACCC for a price cap exemption. Any parties that are granted an exemption will be listed on the ACCC’s public register.

As the ACCC hears from gas producers and users about their commercial negotiations with the price cap in operation, or observes matters of relevance to the operation of the new laws, it may update the guidelines if there are aspects that warrant refinement or clarification.

Advertisement

This is how toxic the gas cartel is. Everybody, worldwide, now has gas and can buy it for years at ever-decreasing cheaper prices. In Australia, one of the most blessed cheap gas jurisdictions in the world, you can’t buy it at all.

Apply the fines now. Pull the lever on the ADGSM. Threaten imminent export levies. Whatever it takes.

If it were up to me, these baleful firms would be rounded up and hanged for treason.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.