The last time I wrote about Aussie yields in mid-December, I suggested that it “was a brave man that bets against further curve flattening”.

Markets immediately made that brave man richer as China let COVID rip, Europe’s warm winter crashed energy prices, and the BOJ edged towards an exit from YCC.

Cripes!

Thanks to these three events, AUD yields sprang higher before the new year brought relief given the temptation of 4%+ yields:

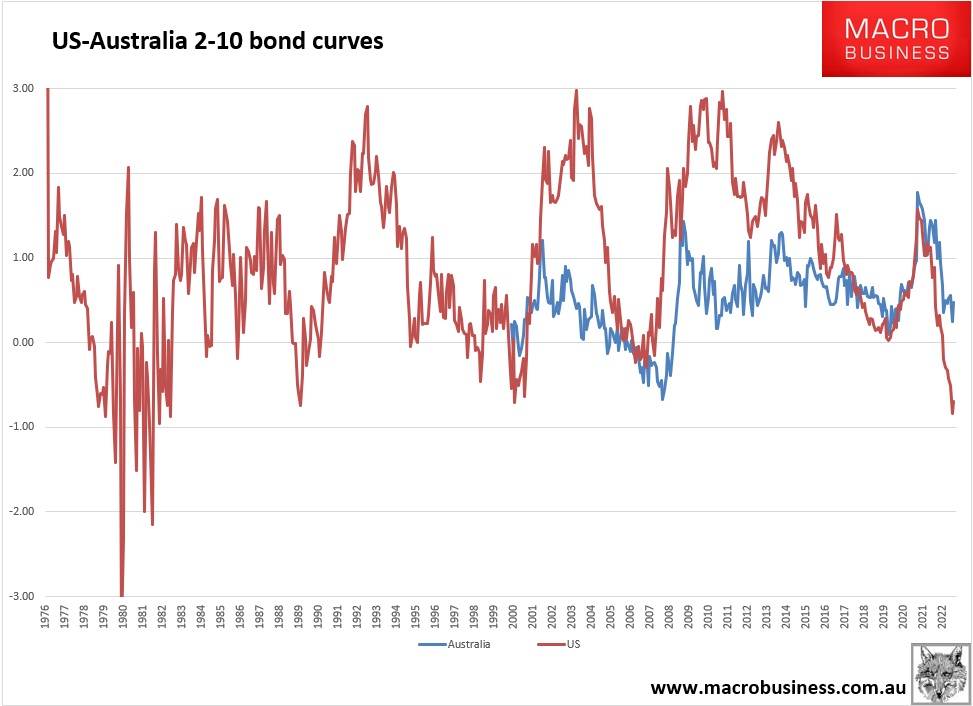

In turn, this steepened the yield curve:

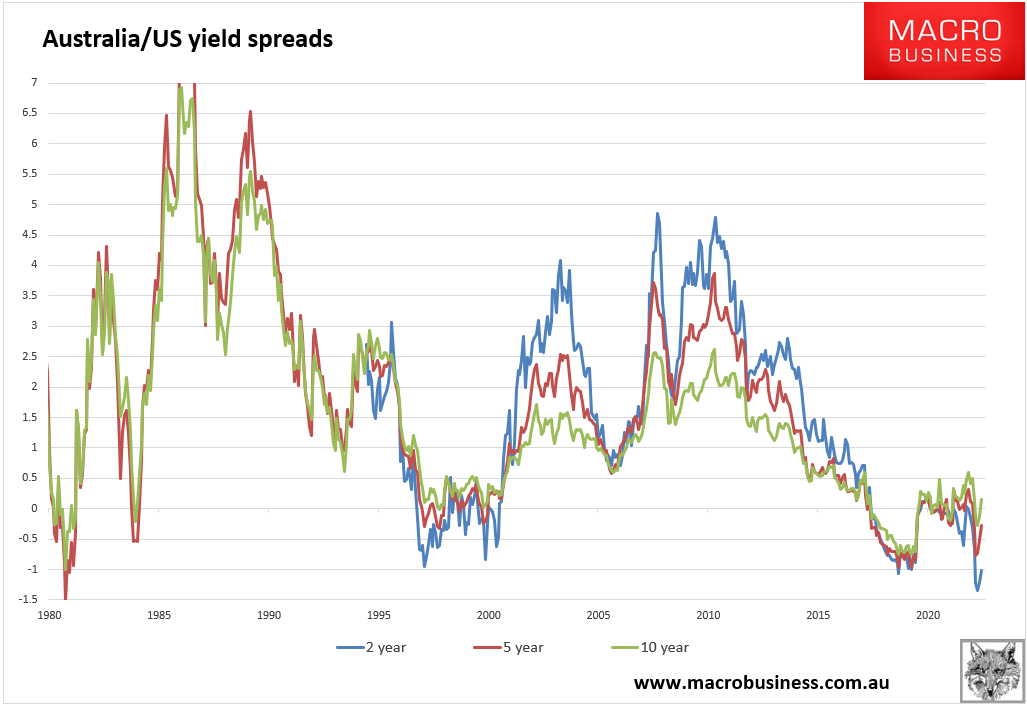

And widened spreads to the US:

I do not see this as a trend change. Global disinflation is gathering pace and will land on the BOJ in due course. European energy price relief helps that too but the ECB remains hawkish. Finally, I expect the Chinese reopening to be consumer not investment led so Australia will benefit less via commodity prices than a typical cycle.

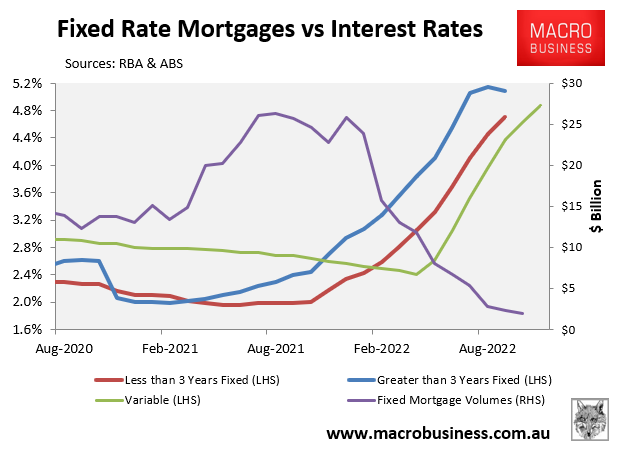

Moreover, Australia is unique this year in that its domestic demand is now entering an intense rate shock for households thanks to the fixed mortgage rate reset. This has embedded a monetary shock of a magnitude not experienced in modern times by Aussie households with new mortgages:

This is going to smash discretionary consumption which will already be under intensifying pressure from the rapidly deepening reverse wealth effect of tumbling house prices which has much further to run.

Along with Australia’s cratered energy prices and renewed cheap foreign labour supply, these disinflationary shocks are likely to overwhelm any external positives arising from China reopening, and Aussie growth and inflation will fall away sharply. Whether we slump into actual recession is immaterial.

Since the RBA jackknifed out of its own YCC last year, markets have treated it with a barge pole:

UBS strategist Giulia Specchia says investors hate surprises, and the Reserve Bank should therefore aim to be as predictable as possible if it wants international investors to return as buyers of Australian government debt.

Offshore-based private buyers have stayed on the sidelines in Australian government bond auctions for the past year, waiting for a clearer direction on interest rates

Treasury has around $900 billion of debt in circulation, and just under half is in the hands of non-Australian residents – down from 57 per cent before the pandemic, and well below a peak of 76 per cent in 2012. Japan is the largest offshore holder of Australian government debt.

There is a good reason for the Reserve Bank to heed Specchia’s warning: there is a risk Australia’s federal and state borrowers may have to offer the bond market more attractive terms, particularly on longer-dated bonds.

“The RBA is definitely aware that the way they handled forward guidance created issues of credibility and reputation, and they are becoming more predictable,” Specchia says, with a nod to the dramatic turn of events leading up to the November 2021 policy meeting.

…She argues the situation in Australia is very different: with 70 per cent of mortgages based on variable interest, higher borrowing costs are immediately felt by home-owners compared to other economies, where the majority of home loans are set by fixed rates.

…“The RBA does not need to go that hard and that fast and that gives Australia a better shot at achieving a soft landing compared to other economies.”

I don’t think so. The bank has already overcooked it and it is only a matter of time before the house price crash sucks down the economy.

Ironically, this will restore the RBA’s credibility with markets as it is forced to lead the global easing!