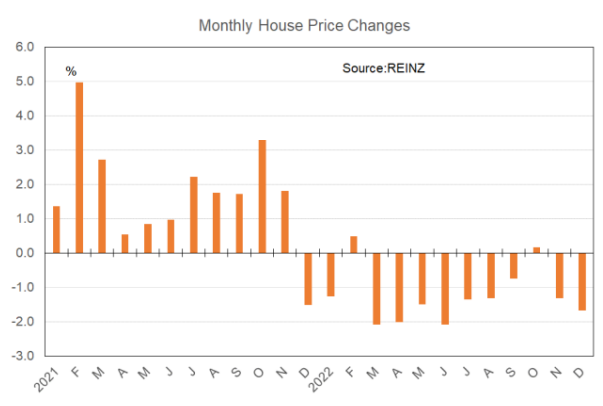

Below is independent economist Tony Alexander’s analysis of the latest plunge in New Zealand house prices, where value declines nationally accelerated to -1.7% in December 2022 to be down -15.1% from their November 2021 peak.

Alexander argues that “things got a lot worse” for the housing market in late November when the Reserve Bank “lifted the official cash rate by a record 0.75% to 4.25%, raised their pick for its peak from 4.1% to 5.5%, and said that the country would enter recession in 2023”.

In response, “business and consumer sentiment readings plunged anew and there has been further worsening in my housing market survey results”, according to Alexander.

__________________________________________________________________________________________

The REINZ released their monthly data on the NZ residential real estate market this week and just in case you’ve not seen these following words before let me repeat them. The only house price data I look at, analyse, and comment on are the REINZ House Price Indexes. They are based on sales which actually happened in the month – in this case December – and not title changes based on sales which happened potentially many months ago.

They adjust for changes in the mix of dwellings sold from one month to another so do not get distorted if one month lots of expensive houses sell and the next only the cheap one’s turnover, or one month mainly the sales are of apartments and the next they are mainly standalone houses.

I think a reporter forgot that on Monday when he was asking me about the small 0.2% decline in prices reported by an alternative data provider this week. I said I had nothing to say because the data were meaningless and I don’t track them. I’m waiting for his call about the REINZ stuff. To whit.

On average around the country in December house prices fell by 1.7%. This was more than the 1.3% decline in November and the strange 0.2% rise in October.

Why did the improving trend in price declines suddenly reverse in November and December and make my talk about the market entering the endgame for price declines from late-2021 look premature? Because inflation has turned out to be a lot higher and more persistent than any of us were expecting.

On October 18 when the September quarter data were released we were all set up for Statistics New Zealand to report an annual change of 6.6%, down from 7.3% three months earlier. But the result was a shock 7.2% and the hopes most of us had about inflation responding well to weak business and consumer sentiment readings were dashed.

The financial markets immediately factored in monetary policy having to tighten more and stay tight for longer and the higher cost of funds for banks caused fixed mortgage rates to jump up about 0.5% or so across the board.

These rate rises produced immediate weakness in the many readings of housing market sentiment garnered from my monthly surveys.

Things then got a lot worse on November 23 when the Reserve Bank had its first official opportunity to respond to the bad inflation news. They lifted the official cash rate by a record 0.75% to 4.25%, raised their pick for its peak from 4.1% to 5.5%, and said that the country would enter recession in 2023 as part of their requirement for inflation to be beaten.

Mortgage rates for fixed terms again went up about 0.5% across the board, people started forecasting much higher rates, and the talk of recession being needed scared everyone back into their shells. Business and consumer sentiment readings plunged anew and there has been further worsening in my housing market survey results.

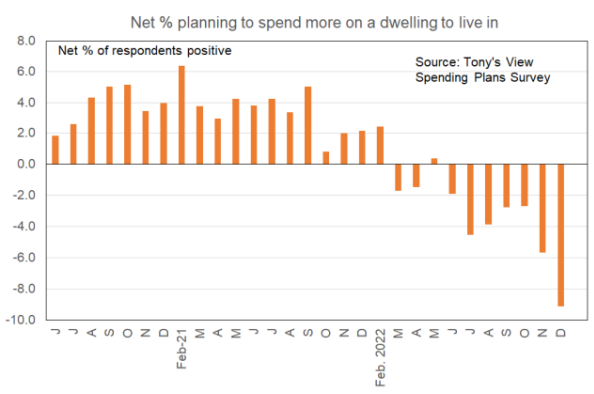

This graph shows the fresh decline in people’s plans for buying a house to live in, garnered from my monthly Spending Plans Survey. The decline in December is quite stark.

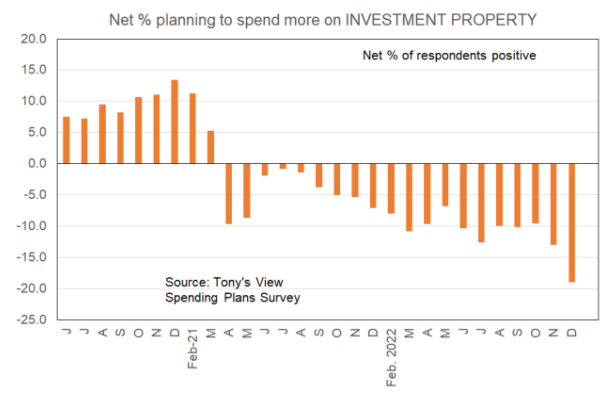

This one shows the fresh decline in property investment plans.

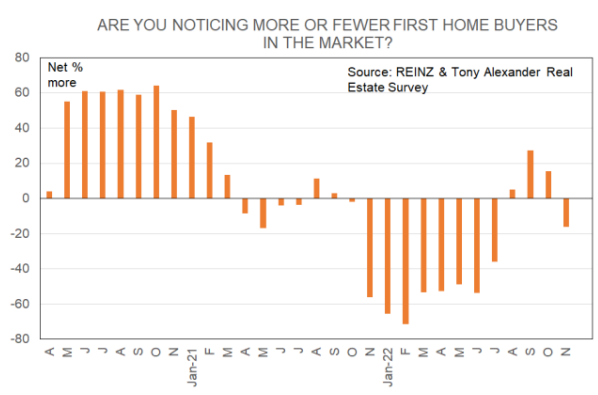

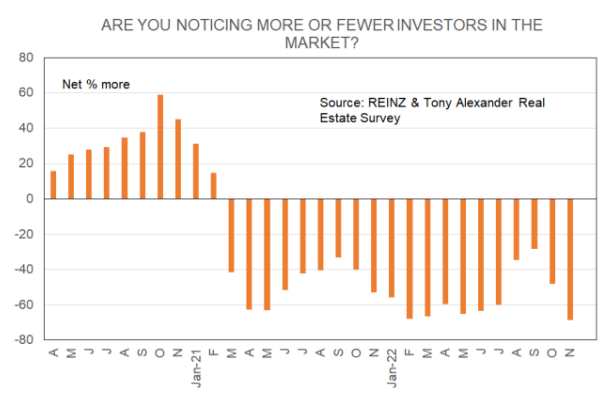

These next two come from my monthly survey of real estate agents undertaken with REINZ. They show the new downturn in observations of first home buyers and then investors.

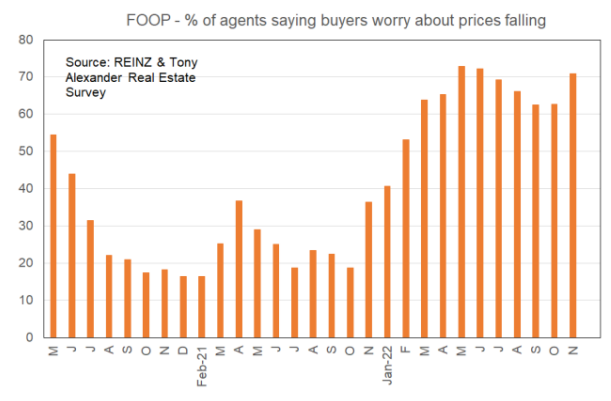

This graph reveals the rise in people’s concerns that prices will fall after they might make a purchase.

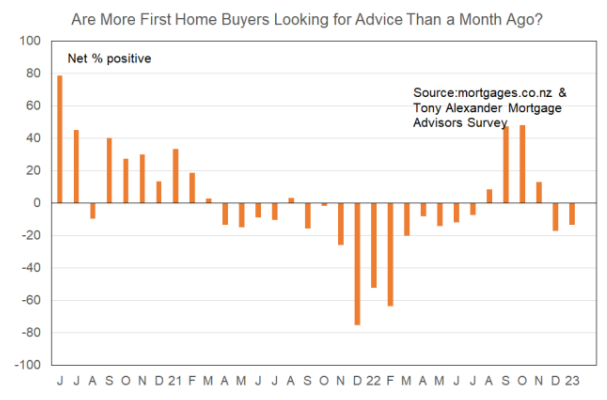

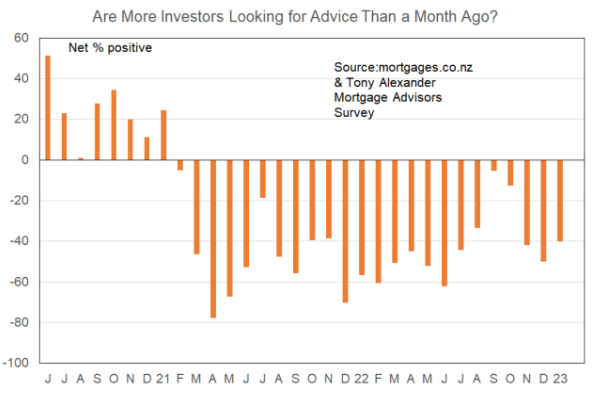

These next two are my most up to date and they come from my monthly of mortgage brokers undertaken with mortgages.co.nz. They show that the pullback of late last year has continued in the middle of January.

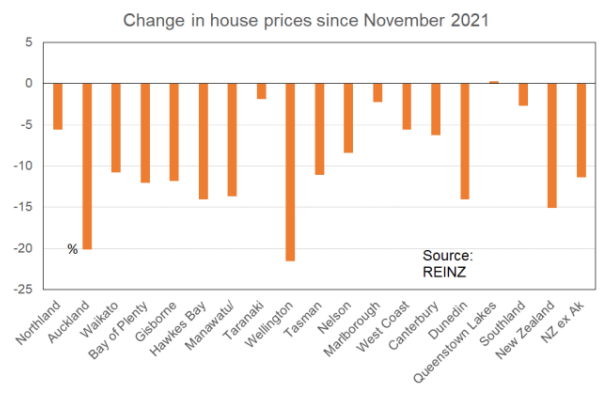

Now, let’s switch back to looking at the REINZ data released this week. With average prices falling in December by 1.7% they now sit 15.1% below their November 2022 peak. Auckland prices have declined by 20%, Wellington 22%, and Canterbury 6.3%. Queenstown is unchanged.

This next graph shows regional price changes since the late-2021 peak.

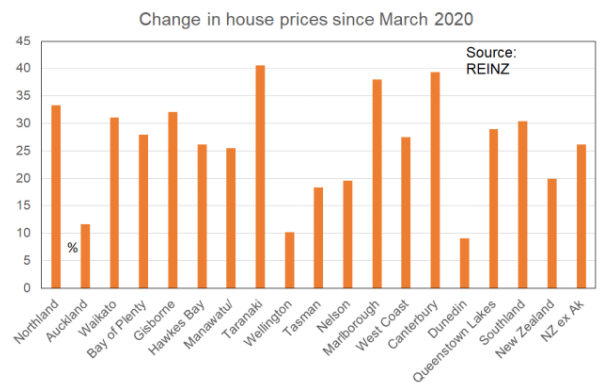

This next graph shows how prices compare with where they were in March 2020. Prices are well up everywhere but with relatively small gains for Auckland, Wellington, and Dunedin.

What is likely to happen to prices from here? I have sufficiently proven to myself that I cannot predict house price change so will refrain from anything too specific. But with such crushed levels of consumer and business sentiment and strong worries about recession and interest rates, it seems safe to assume that prices will keep falling towards the middle of the year. By then the worst is likely to be over and the interest rates outlook could be quite different.

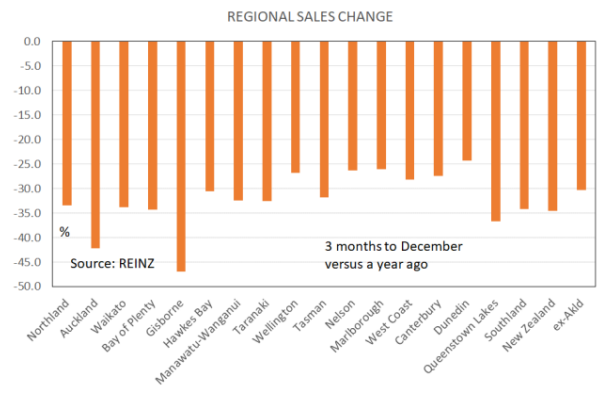

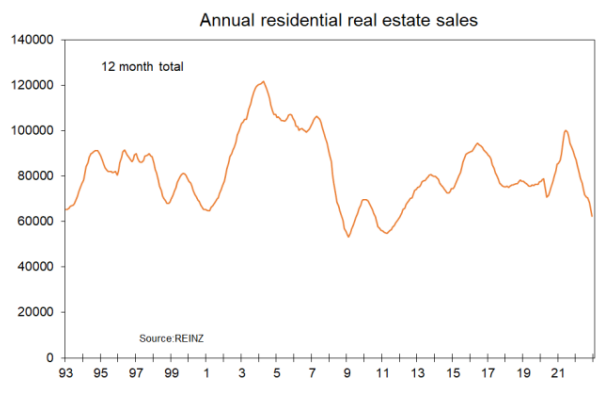

With regard to the number of property sales, activity in December was 39% weaker than a year earlier and the annual number of sales has fallen to 62,400 from a peak of 100,000 in June 2021. And 88,700 a year ago. A decline towards 55,000 is now looking very likely.

Sales have fallen everywhere around the country as shown by this graph where sales for the December quarter are compared with a year back.