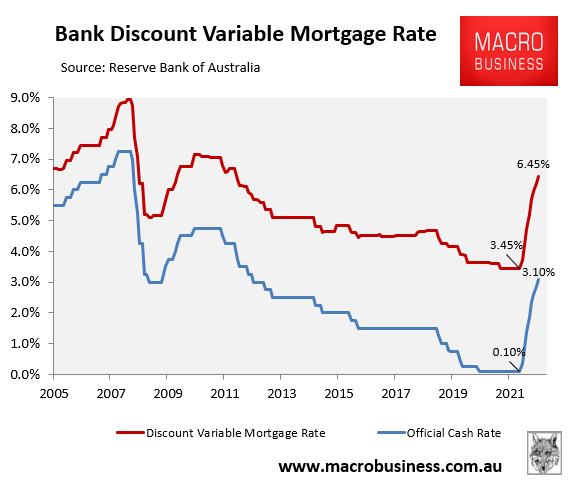

Everybody with a mortgage knows that the latest interest rate cycle in Australia is one for the record books.

In only seven calendar months, Australians saw the official cash rate (OCR) climb by 3.0%, which has nearly doubled variable mortgage rates:

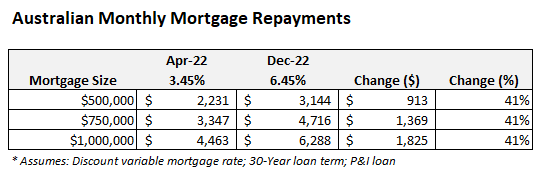

In turn, average variable mortgage repayments have soared by around 40%, adding around $900 a month in repayments to a typical $500,000 mortgage:

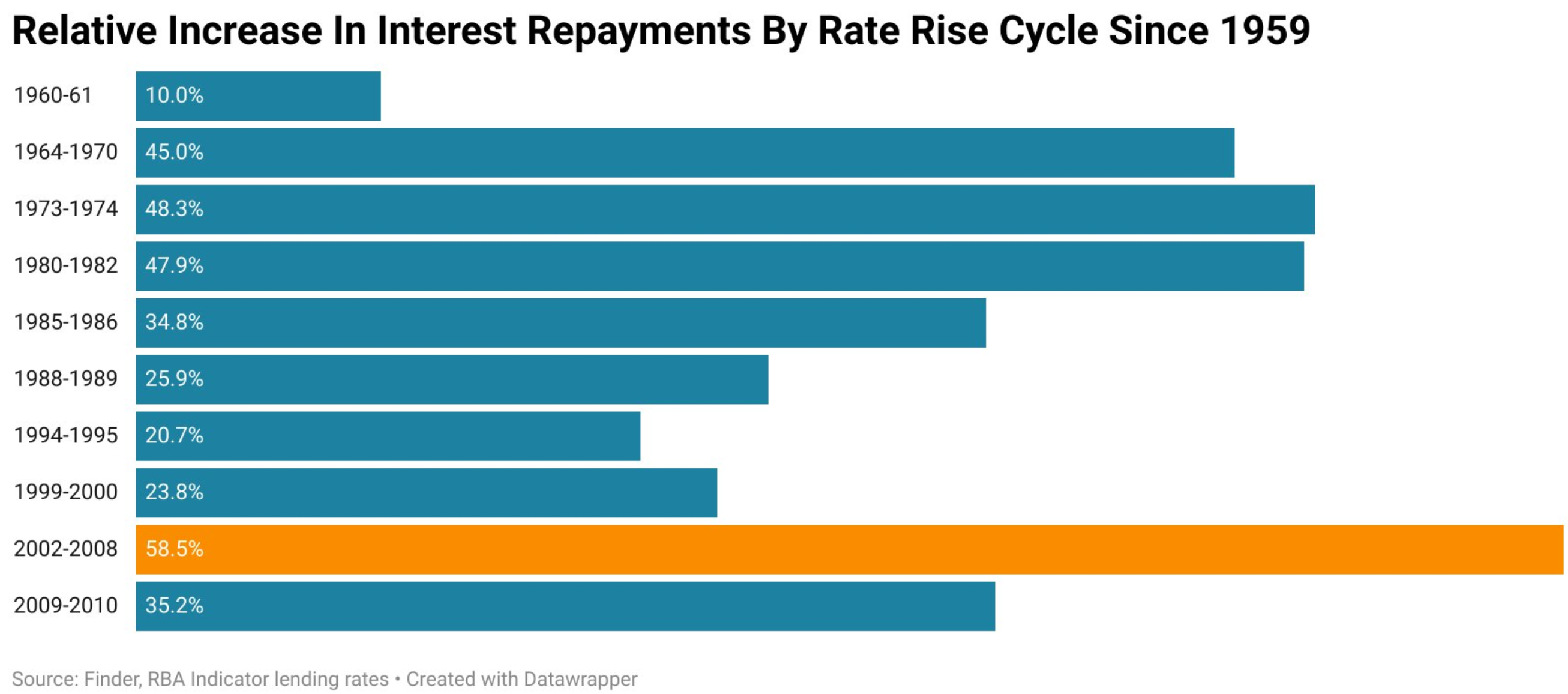

Freelance economist and journalist, Tarric Brooker, has posted the below information on Twitter estimating how Australia’s current interest rate cycle compares with historical experience.

Rather than examining raw interest rate increases, Brooker has instead calculated the percentage change in mortgage interest repayments from the trough to the peak of the interest rate cycle.

It turns out that this interest rate cycle is by far the most aggressive in records dating back to 1959.

According to Brooker, “the current Aussie rate rise cycle is unlike any other seen since records began in 1959. The largest increase in interest repayments over that time was 58.2%. In this cycle interest repayments are set to more than double over ~1 year vs 6 years in largest previous cycle”:

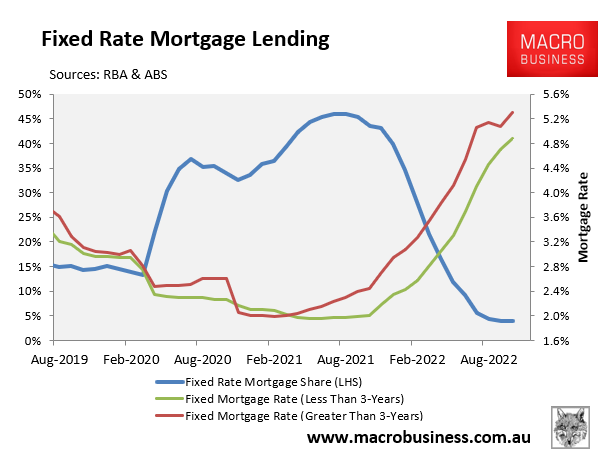

A record share of mortgages was taken out at fixed rates over 2020 and 2021, and these borrowers are yet to be impacted by the RBA’s aggressive rate hikes:

The situation will change in 2023 when nearly one-in-four mortgages (by value) will switch from their ultra-low fixed rates originated at around 2% to rates that are more than double these levels.

When this happens, the share of household income used to service principal and interest debt repayments will soar to their highest level in history, placing many households under severe financial stress.

That is when the fallout from the RBA’s unprecedented interest rate tightening will take full effect.