Chris Joye at his lyrical best:

Martin Place has a big, mother-trucking sledgehammer – a veritable Thor’s hammer as far as monetary policy tools go.

And that’s because the huge preponderance of floating-rate debt in the Aussie economy, which is unusual globally, makes it extraordinarily interest-elastic. This elasticity was seriously impaired during the pandemic by the advent of the RBA’s exceptionally powerful term funding facility (TFF).

…The proportion of fixed rate loans as a share of all mortgages jumped from a trivial, circa 15 per cent before the pandemic to 46 per cent after it because of the wave of cheap money precipitated by the TFF.

This has been a key reason the domestic economy has yet to be nuked by the RBA’s unprecedented 3 percentage points of interest rate increases. The TFF temporarily denied Thor’s hammer much of its power.

But…as 2 per cent fixed rate mortgages transform into 6 per cent variable rate loans. Hammer time will once again return.

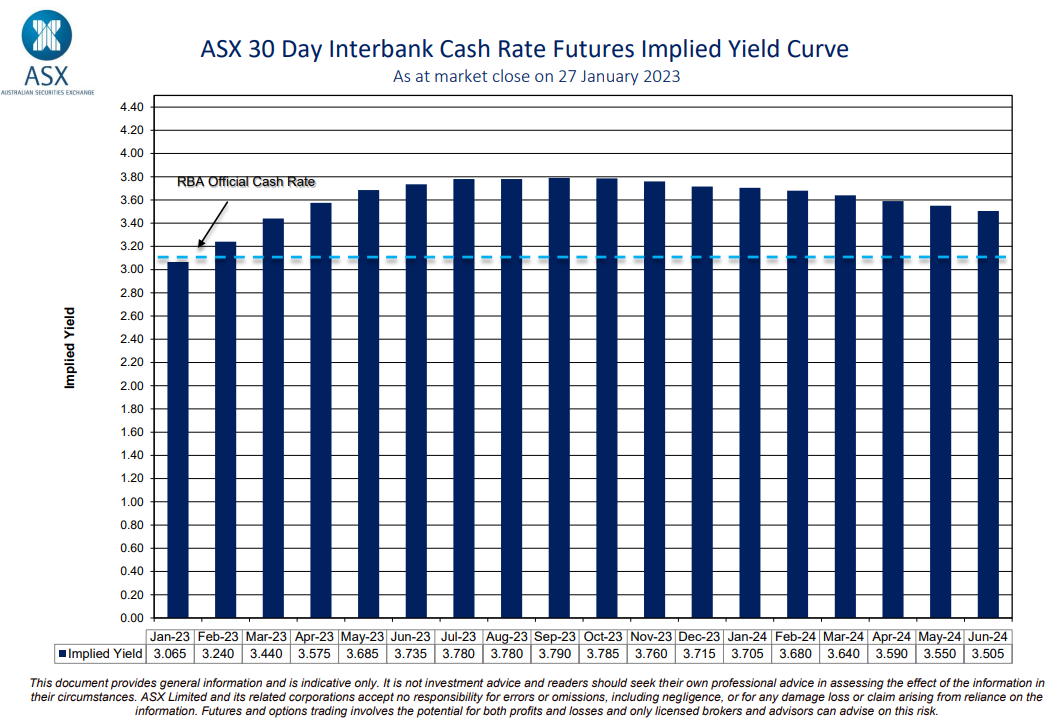

Indeed it will. Yet the RBA is caught between Scylla and Charybdis. It has to raise rates at least twice more to save its own tattered credibility. Three times according to interest rate futures:

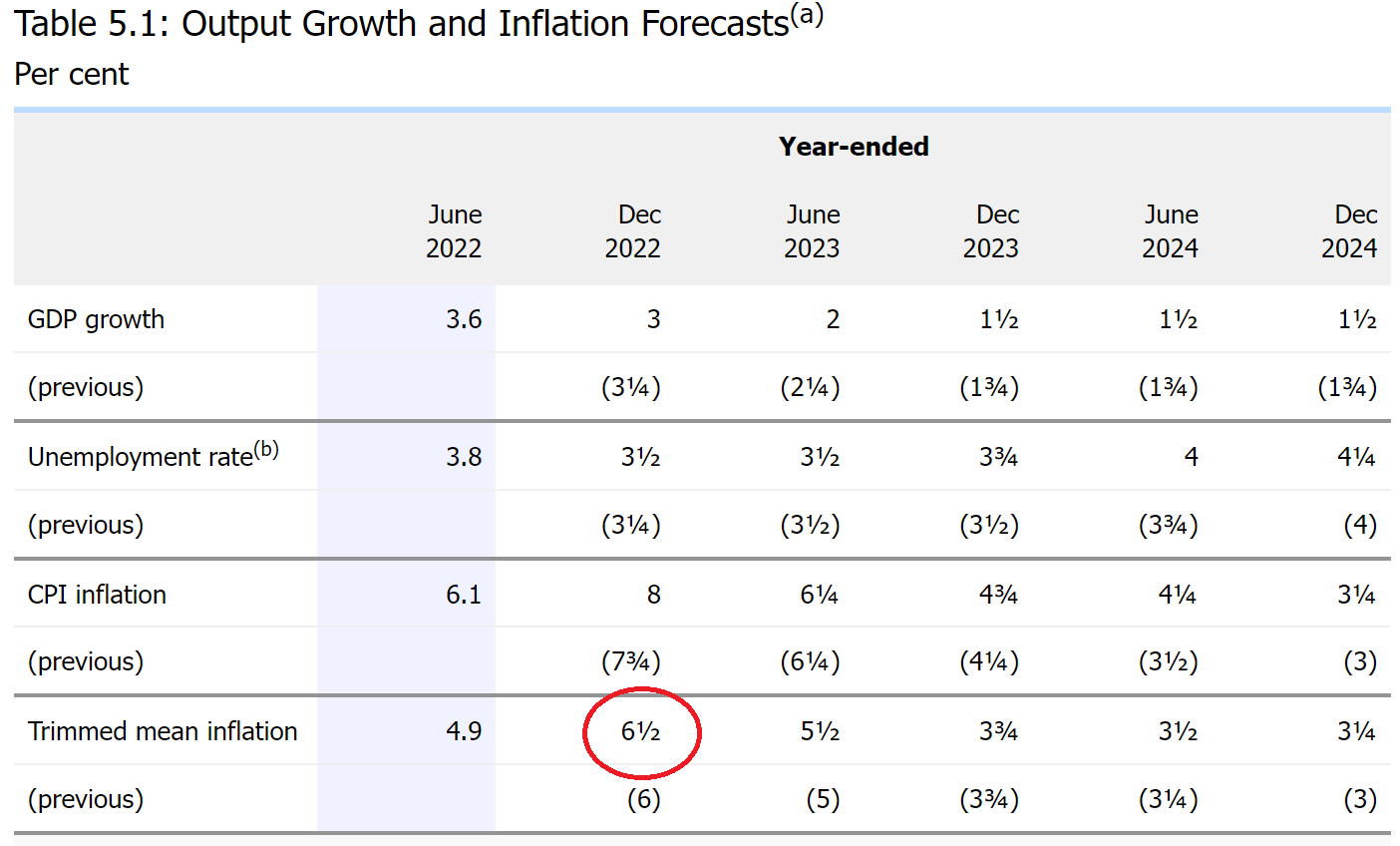

The breadth of inflation is far above its own outlook of 6.5%, which was only just revised up:

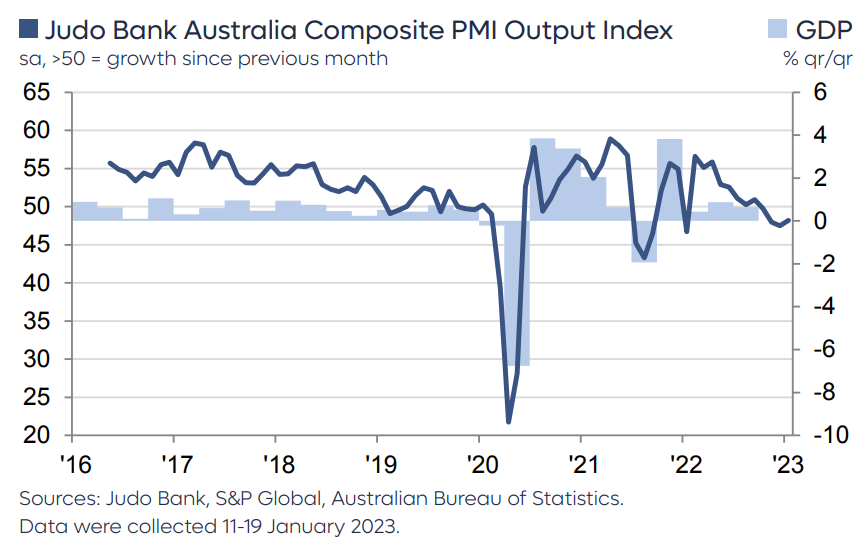

Yet it will trash the economy by doing so. Australia is close to recessionary conditions right now. The latest flash PMI was clear:

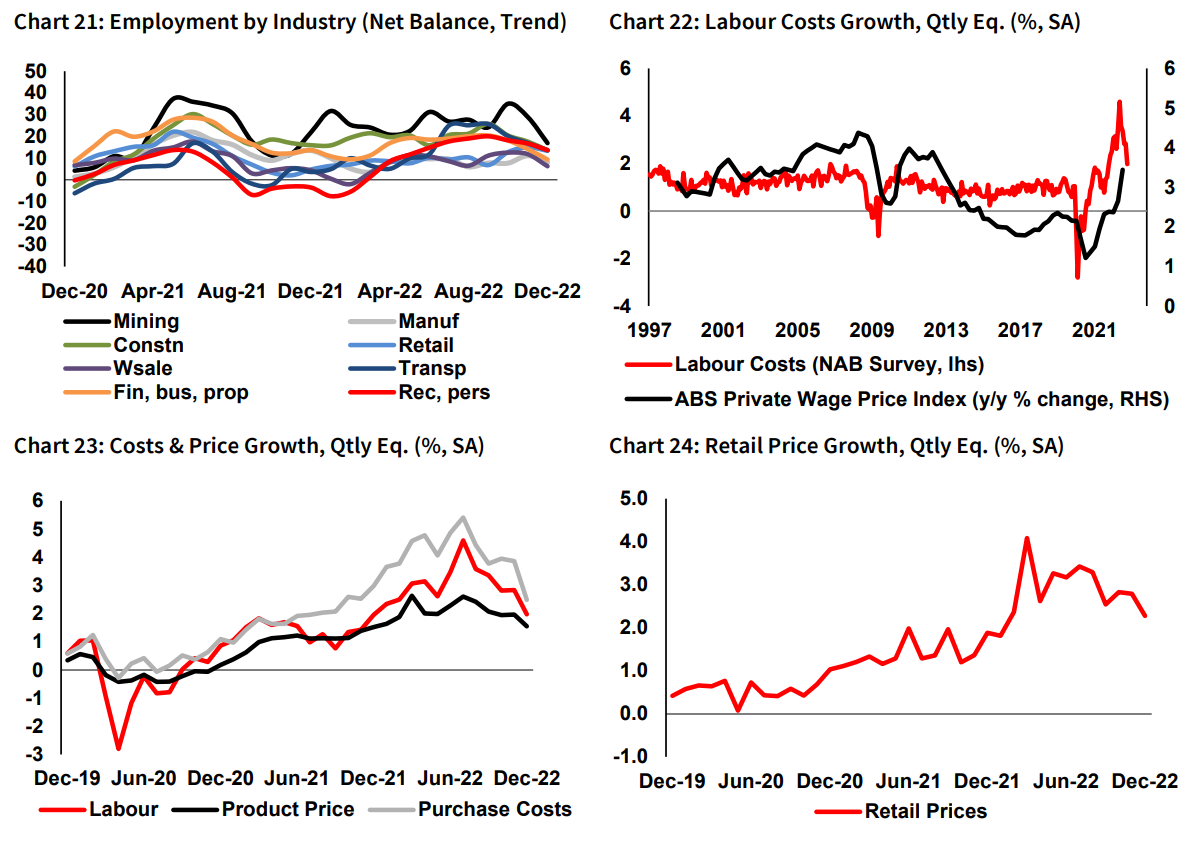

And leading price indexes have clearly turned:

Thor’s hammer is going to land on an already reeling foe and smash Australia into recession.