Independent economist Tony Alexander has published his first “Tony’s View” report for 2023, which examines what the latest batch of surveys are saying about the New Zealand economy.

Based on these results, “things do not look good for the New Zealand economy over 2023” and point to a possible “deep recession”.

Bad indicators for 2023

Things do not look good for the New Zealand economy over 2023 if we base our outlook solely upon what the many opinion surveys tell us. In this first main article for 2023 I will run through the main survey results released late last year including from my own monthly polling efforts.

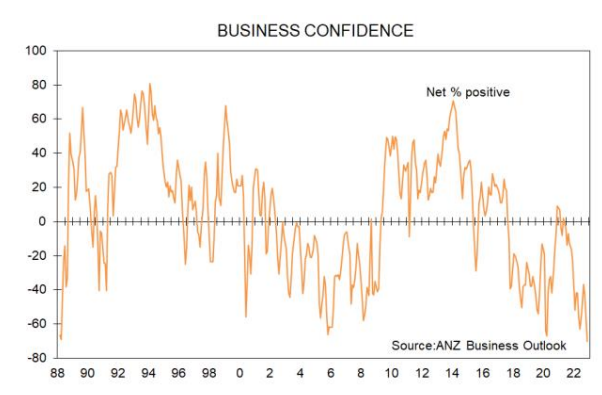

Let’s start with the long-running ANZ Business Outlook Survey for which all late-2022 indicators are bad. A net 70% of business respondents have a negative outlook for the NZ economy over 2023. This is the worst result ever.

A net 26% expect their own business output levels to decline. This is also the worst outcome on record and in normal circumstances would suggest a deep recession.

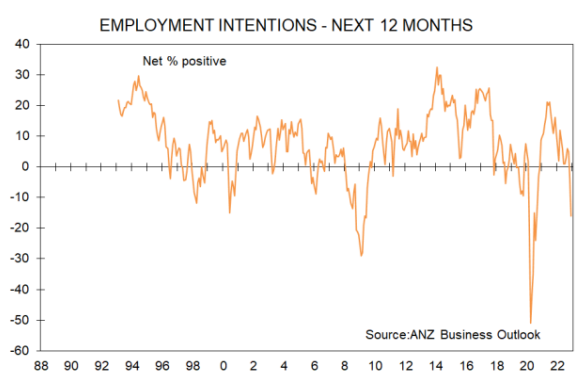

However, the first area of true value from the ANZ survey comes from their employment and investment intentions readings. A net 16% of firms in early-December said they intend laying people off. This is a bad result and a sharp decline from – 4% in November and positive results ever since late-2020.

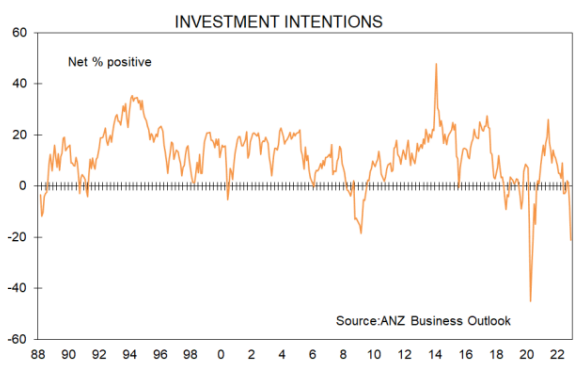

There have been worse readings in the past and it is likely there is a shock component related to the Reserve Bank’s prediction of recession. But the result still bespeaks of a weakening labour market. A net 21% of firms plan cutting their capital spending levels.

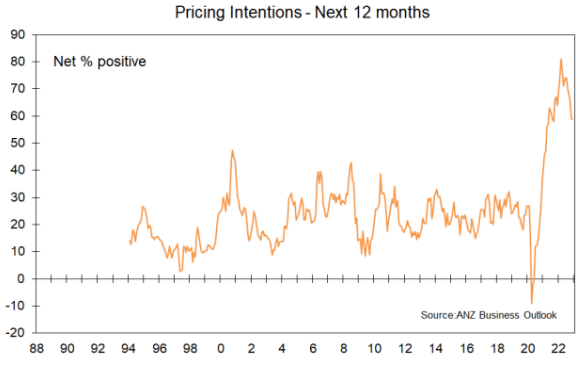

The other area of insight provided by the ANZ survey comes with respect to inflation. The sharp fall in job hiring intentions is a good portent for wage pressures easing – keeping in mind that the labour market changes after the rate of growth in the economy has changed, not before it. So, be wary of making your monetary policy predictions on the back of employment measures. If you do you could be well behind changes already apparent in market pricing of inflation and interest rates. Or, if the markets choose to focus on employment measures, be prepared for a substantial decline in wholesale interest rates at some point when the weakening wage growth stage is reached.

A net 59% of business plan raising their prices in the next 12 months. The trend in this measure is thankfully down, but the level is still much too high for anyone’s comfort and will have the Reserve Bank determined to keep monetary policy tight.

The ANZ survey tells us that it is reasonable to expect recession this year and reasonable also not to expect interest rates to decline for quite some time. But do not ignore the potential for measures in this survey to change quite quickly.

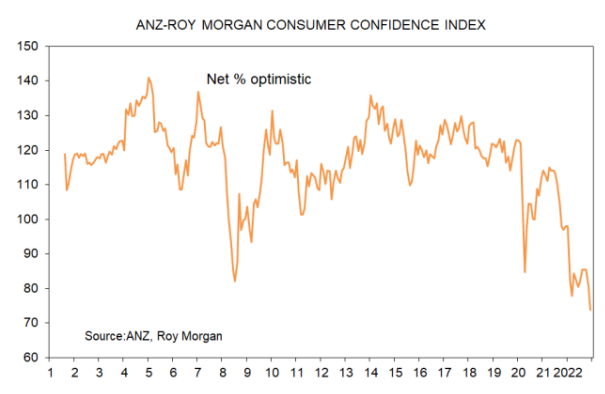

We can gain insight into household spending prospects from a number of surveys. Westpac produce a quarterly one with McDermott Miller but it dates quickly. The ANZ run a survey with Roy Morgan and that one showed an index reading for consumer confidence of 73.8 in December from 80.7 in November.

A reading of 100 is considered neutral and the outcomes have all been below 100 since October 2021. The survey suggests a lot of retail spending weakness in the near future.

The third useful survey available to us (excluding my own monthly ones) is the NZIER’s QSBO. This only comes out every three months so isn’t as optimally useful at this uncertain point in the cycle as it could be. But the next one comes out on January 17 and will give us insight into capacity and cost pressures in the economy.

The trouble however is that the results will largely reflect responses sent in not long after businesses responded to the ANZ Business Outlook Survey so there will be shock value captured in the data which like the ANZ survey could easily overstate the extent of upcoming weakness in the economy.

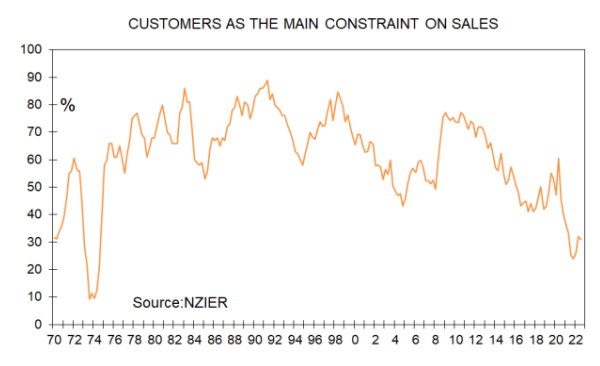

Nonetheless, it can be market and opinion moving so keep an eye out for that next Tuesday. For the record, the area in which the QSBO adds unique value is with regard to capacity pressures in the economy. The survey from three months ago showed only a slight easing in business difficulties sourcing skilled and unskilled labour.

The survey tells us a lack of customers is not much of a problem for many firms.

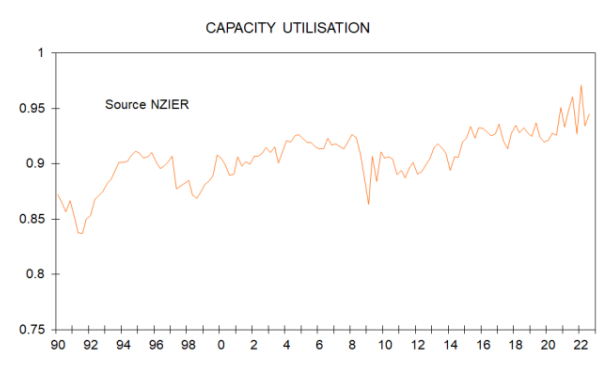

And the capacity utilisation rate which can indicate cost pressures has eased but remains relatively high. These are the things we will be looking at next Tuesday, alongside the direct survey outcomes regarding business plans for raising prices and expectations regarding cost changes.

The surveys show us an economy short of capacity with elevated inflation pressures, and recession imminent because consumers are depressed, and businesses plan sacking staff and cutting capital expenditure.

This makes forecasting sound easy, doesn’t it? Not so fast. Keep in mind:

- the faster than expected recovery in the inbound tourism sector so far underway,

- the early opening of China’s borders set to send many people our way soon,

- the stronger than expected net migration inflows,

- good prices being received by primary exporters (by and large),

- the lowish Kiwi dollar,

- the coming fiscal policy easing from a government looking to minimise the rout in this year’s general election,

- the high level of job security, and

- a household savings buffer built up during the pandemic period.

The surveys tell us a recession is virtually guaranteed. A wider and unemotive analysis of the factors in play tells us it is the toss of a coin as to whether we enter recession or not. And from a monetary policy point of view, recession is only relevant for the extent to which it leads to a reduction in inflationary pressures. An economy can enter recession yet still require smashing in order to get inflation down.

So, pay closer attention to cost and pricing measures in the next few months than to actual measures of business and household spending and hiring.