The demand for mortgages has taken a severe hit in response to the Reserve Bank of Australia’s (RBA) aggressive monetary tightening.

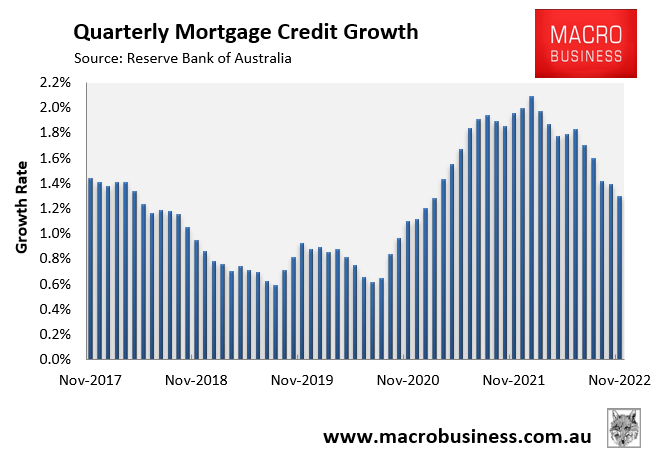

Quarterly mortgage growth fell to 1.3% in the November quarter of 2022, down from a peak of 2.1% in the January quarter:

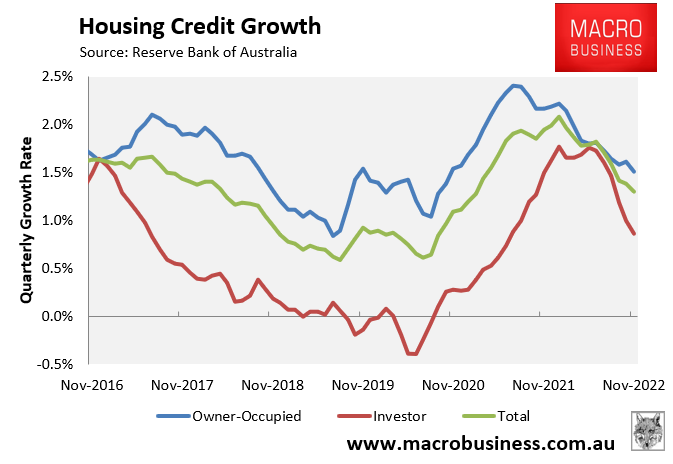

As shown below, the decline in mortgage growth has occurred across both owner-occupiers and investors, with both well down from peak:

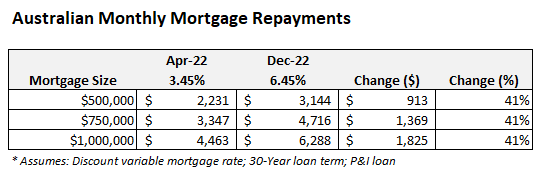

Given this data is only current to end-November, it does not account for the 0.25% rate hike by the RBA in early December.

Once the RBA’s 3.0% of cumulative rate hikes are fully passed on to mortgage holders, monthly repayments will rise around 40% above their April 2022 pre-tightening level:

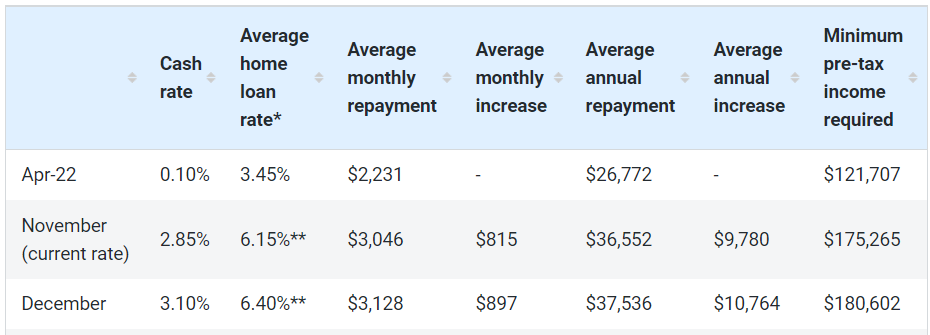

In turn, borrowing capacity will decline by around one-third. According to Finder, the amount of pre-tax income required to service a $500,000 mortgage will rise from around $121,000 in April 2022 to $181,000 following the RBA’s 3.0% of rate hikes:

Source: Finder

Lower borrowing capacity equals reduced mortgage demand and lower house prices. The equation is that simple.

And the further the RBA tightens, the more mortgage demand will soften and house prices will fall.