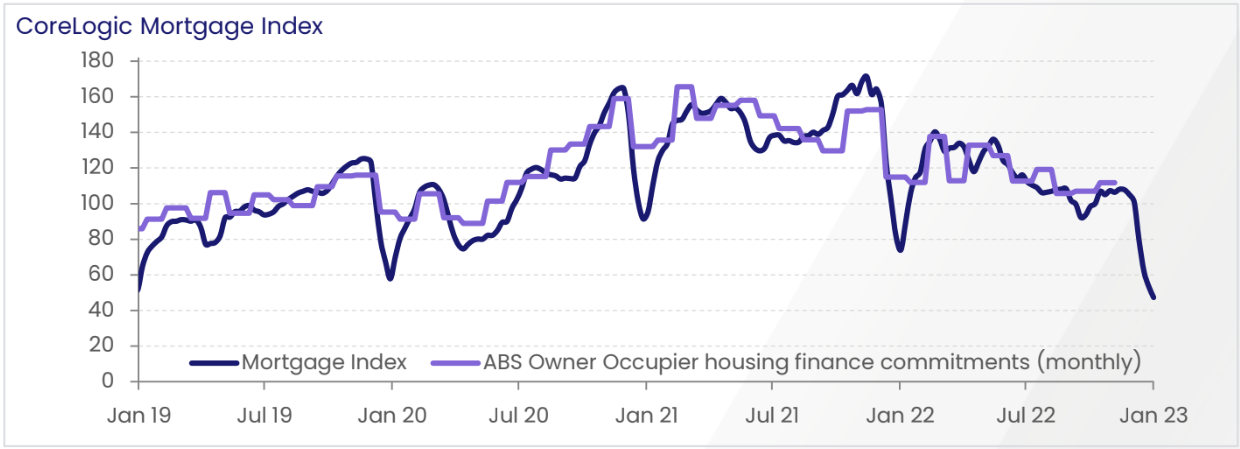

The latest leading mortgage indicator from CoreLogic showed that mortgage demand has collapsed across Australia to levels not seen since the last property correction in 2018-19:

CoreLogic claims its leading mortgage index, which is based on “more than 100,000 mortgage activity events every month across our 4 main finance industry platforms”, has “an 81% correlation with the ABS housing finance data series (88% using the seasonally adjusted series)”.

Therefore, based on this data, the official ABS housing finance series should record heavy falls once the December and January results are posted over the next two months.

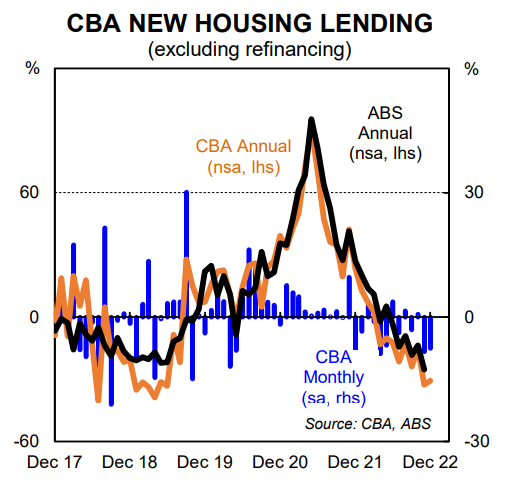

Interestingly, CBA’s latest housing lending data has also been released, which “fell again in December 2022” with “lending to purchase existing dwellings the key driver of the annual decline”.

As shown below, CBA’s series shows a very strong correlation with the official ABS housing finance series, and signals a further decline when December’s ABS data is released early next month:

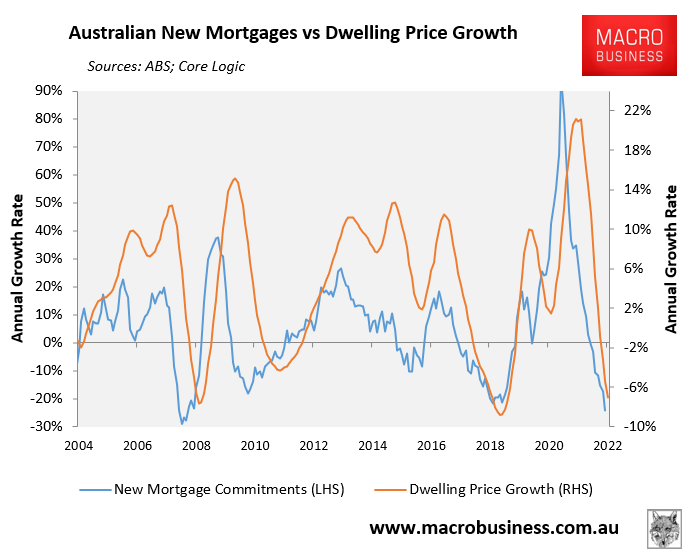

The ongoing decline in housing finance commitments is bad news for Australian dwelling values given the growth in new mortgages (excluding refinancings) has historically been a strong leading indicator for price growth:

That is, should mortgage growth collapse, so too will Australian house prices.

For what it is worth, I expect Australian dwelling values to bottom out in Q3 before starting to rise late this year after the Reserve Bank of Australia begins cutting interest rates to ward-off recession.

But there is also the non-trivial risk that the fixed rate mortgage reset, which will this year see large volumes of mortgage holders switch from ultra-cheap loans at around 2% interest to rates that are at least double this level, causes a wave of distressed sales.

If this happens, then Australian home prices could fall more steeply and for longer.