Wall Street fell again overnight taking European shares with it as more data pointed to a forthcoming US recession, setting up a potential hard landing up ahead for 2023, . The USD pulled back against some of the majors, with Euro bouncing back above the 1.08 level while the Australian dollar clawed its way back above the 69 cent level. US bond markets loosening up a tiny bit with 10 year Treasury yields gaining just 4 basis points to finish at 3.41% while the commodity complex saw prices bounceback as Brent crude returned to the $85USD per barrel level. Gold had the best session, surging over $30 to finish above the $1930USD per ounce level.

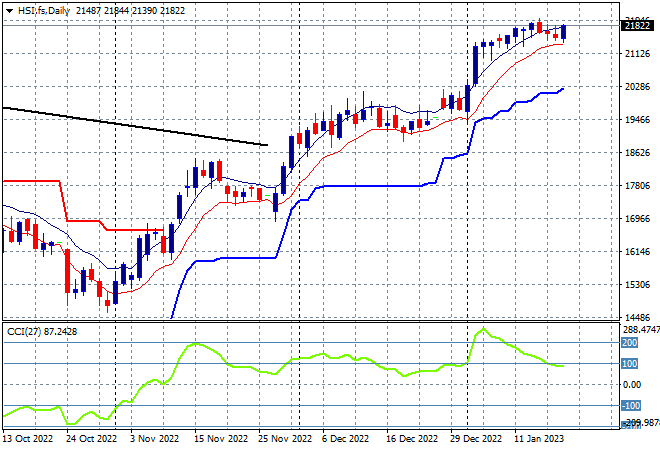

Looking at share markets in Asia from yesterday’s session where mainland Chinese share markets put on more gains with the Shanghai Composite lifting nearly 0.5% higher to remain above the 3200 point level while the Hang Seng Index tread water, down 0.1% at 21650 points. The daily chart was looking over extended so this slowdown is not unexpected, with a series of step ups since the nadir in October last year easing off. Daily momentum is getting out of its recent extreme overbought mode which is a good sign but not yet an indicator of a complete top:

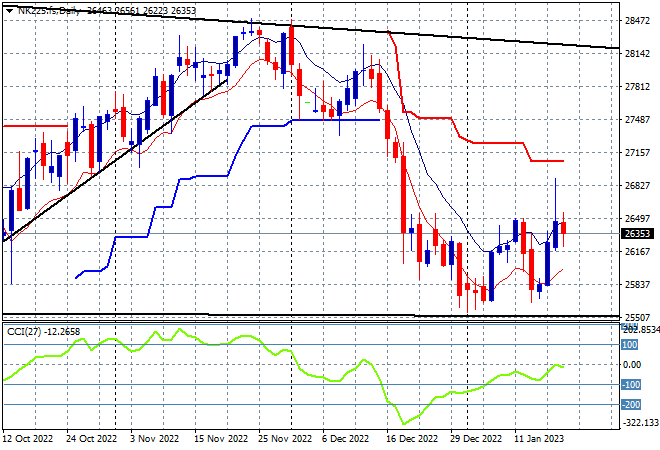

Japanese stock markets pulled back with yet another volatile oscillation with the Nikkei 225 closing 1.4% lower at 26404 points. There remains the potential for a bottom to develop here at the 25000 point level but this continued oscillation around the BOJ and bond market problems will be exacerbated by Wall Street’s inability to gain traction with daily momentum swinging higher but remaining negative: