Risk markets finished the trading week in relative calm after a muted response to the latest US inflation data as everyone still assume the US Federal Reserve will ease off on its rate rise agenda. Wall Street rose with tech stocks leading the way on Friday night as the USD only moved lower against Yen due to the BOJ’s attempt to short up the domestic bond market. US bond markets saw yields reverse their recent gains with 10-year Treasury yields lifting up towards the 3.5% level on the latest consumer confidence figures while the commodity complex saw oil prices also rise as Brent crude broke through the $85USD per barrel level. The shiny undollar gold broke through the $1900USD per ounce level and then some in a big blowout against USD.

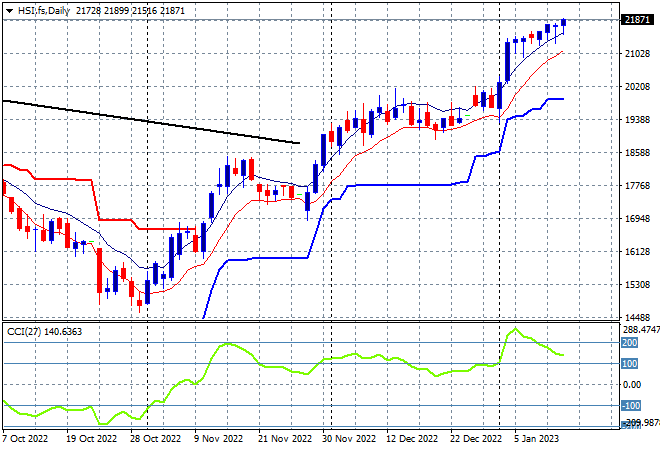

Looking at share markets in Asia from Friday’s session where mainland Chinese share markets moved higher on the latest trade numbers with the Shanghai Composite closing up 1% to remain well above the 3100 point level, finishing at 3195 points while the Hang Seng Index almost put in a scratch session before a late surge also saw it move 1% higher to close at 21738 points. The daily chart continues to look quite boisterous here with a series of step ups since the nadir in October last year as daily momentum tries to moderate out of its recent extreme overbought mode. It looks like weekly support at the 19000 point level is quite firm as traders bet on a post zero-COVID economic liftoff, but the question is this move sustainable:

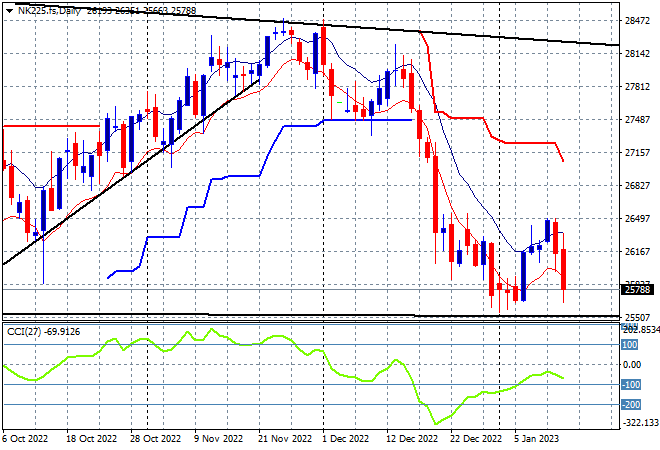

Japanese stock markets however pulled back sharply as the BOJ tried to shore up the bond market amid a much stronger Yen with the Nikkei 225 closing 1.2% lower at 26119 points. There was the potential for a swing long trade to develop further here after bottoming out at the 25000 point level but it failed after only one close above the high moving average with a return to the recent lows on the stronger Yen trade. Daily momentum never went positive with futures indicating a mixed open to start the trading week on a very cautious note: