Very sensible stuff from Goldman. Clear implications for iron ore, coking, and copper in due course.

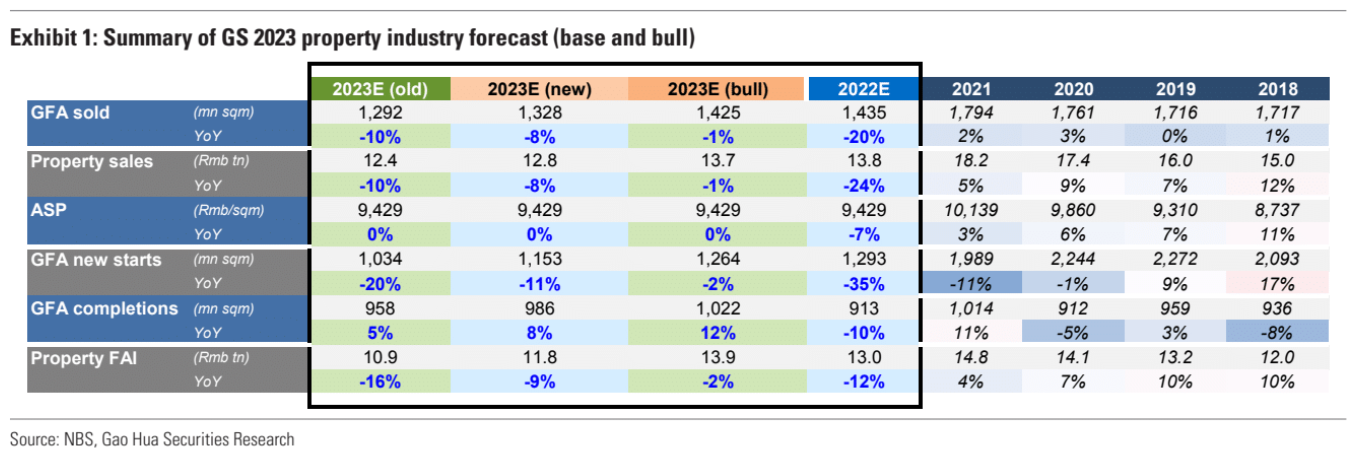

Despite still low visibility on how much liquidity will be actually injected into the property industry, we see clearer policy directions on the back of the “16 measures” announcement, and as a result, we expect property construction to contract less, leading to higher saleable resource and smaller yoy property sales decline in 2023E vs. our prior base-case. We revise up our 2023E industry forecast and fine-tune our 2022E-24E estimates for our coverage to reflect our positive take on the government’s “16 measures”.

Having said that, we see no signs of an outright turnaround of the industry in sight and believe debt extension and restructuring requests from developers facing high liquidity pressure (FHLP) will likely continue. By end of Dec-22, we estimate developers/private developers that have got bank credit lines and bond issuance quota is about 39%/16% of total industry in terms of property sales or 42%/19% if using 2020-1H 2021 sales (i.e. before this downturn); the size of projects from FHLP developers that might get additional liquidity support to continue construction is also difficult to estimate.