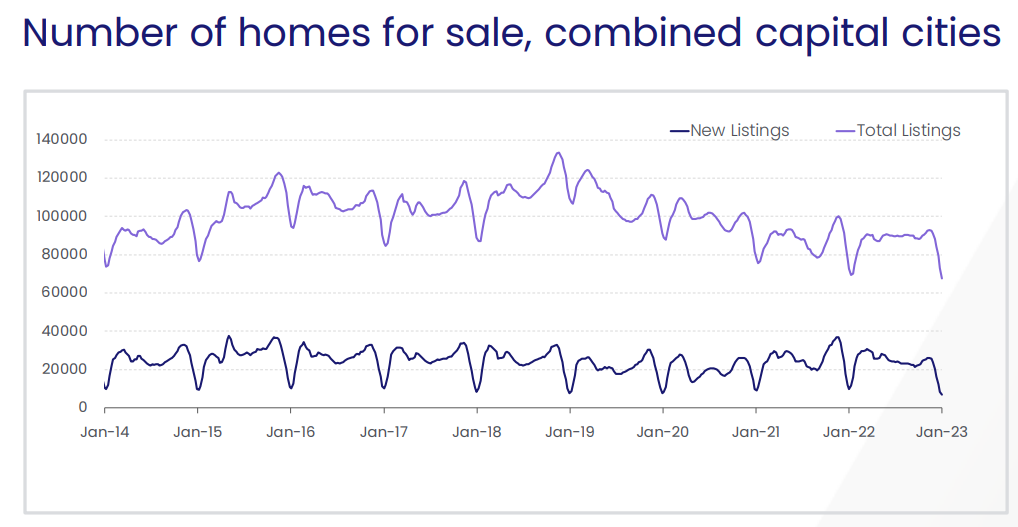

Data from CoreLogic shows that the number of new residential listings fell by more than 22% in both Melbourne and Sydney in the four weeks to 8 January:

Source: CoreLogic.

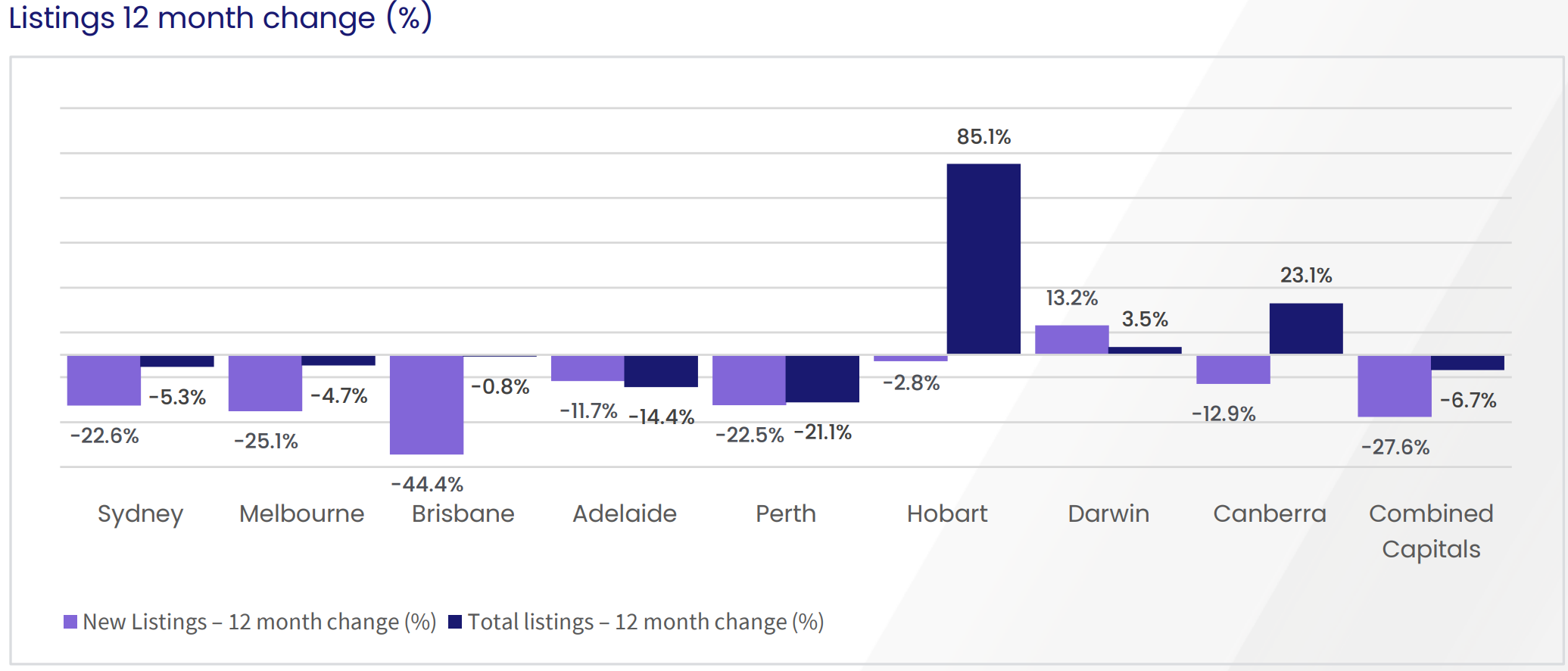

Over the year to 8 January, new listings were down 27.6% across the combined capital cities, while total listings were down 6.7% year-on-year:

Source: CoreLogic

Tim Lawless of CoreLogic believes the below-average flow of new listings suggests that prospective vendors are waiting for the housing market downturn to end. Lawless adds that the low level of listings could help to offset the impact of interest rate rises on house prices.

“Such low advertised supply levels are unusual through a downswing”, Lawless said.

“With the flow of new listings holding well below average across most regions, distressed or motivated sellers remain at relatively low levels in the housing market”.

“The lower inventory levels could provide some support for housing prices, especially if demand drops further as interest rates trend higher”, Lawless said.

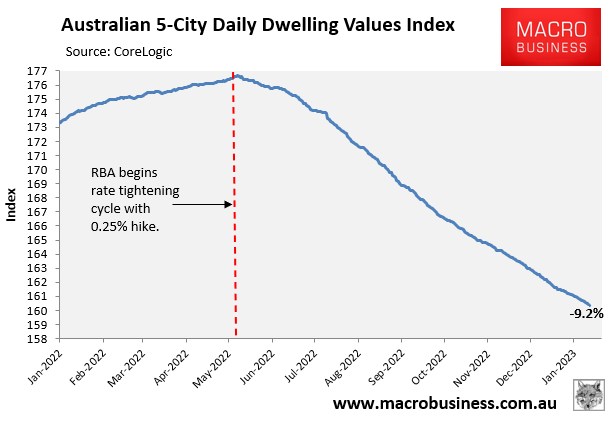

The sharp fall in dwelling values has occurred without a rise in listings or distressed sales. Rather, the price falls have been driven almost singlehandedly by the Reserve Bank of Australia’s (RBA) uber-aggressive interest rate hikes, which have severely limited borrowing capacity and buyer demand:

Ultimately, how Australian far house prices fall will depend on what the RBA does with interest rates, with the volume of listings playing only a secondary role.

If the RBA hikes rates several more times, then price falls will reaccelerate.

But if the RBA soon stops hiking rates, then price falls will moderate. And if it cuts rates, home prices will begin to rise.

That said, there is also the risk that this year’s fixed rate mortgage reset, which will see huge volumes of mortgage holders shift from ultra-cheap loans of around 2% to rates that are at least double this level, could drive a wave of distressed sales.

If that was to occur, then Australian home prices would fall even more sharply.