Chinese economic data came in better than expected. But, given the politically loaded COVID mismanagement, if you believe that you’re a fool. Pantheon wraps the broader data:

- China: Official GDP growth slowed to 2.9% y/y in Q4 from 3.9% in Q3. Consensus was 1.6%.

- Industrial production grew 1.3% y/y in December, down from 2.2% in November. Consensus was 0.1%.

- Retail sales fell 1.8% y/y in December, improving from a 5.9% drop in November. Consensus was -9.0%.

- Fixed asset investment growth slowed to 5.1% ytd y/y in December from 5.3% in November. Consensus was 5.0.

China’s official GDP growth was 2.9% y/y in Q4, beating market expectations of 1.6% and down from 3.9% in Q3. This was a much better figure than 0.4% growth in Q2 2022 or -6.9% in Q1 2020. This means that the economic hit from a mammoth Covid exit wave on a 90% vaccinated population turns out to be much smaller than that of broad lockdowns under zero-Covid policy. Industrial production, in particular, was much less disrupted by Covid exit waves than under the severe restriction periods.

By contrast, the consumption decline in Q4 was similar to that during the Q2 2022 lockdown, though much more moderate than the initial, devastating Covid outbreak in Q1 2020. Household expenditure fell 2.4% y/y in Q4, after a 5.5% increase in Q3 and a 2.4% drop in Q2. Household income growth was relatively stable, dipping to 4.2% in Q4 from 6.5% in Q3 and doing considerably better than 2.4% in Q2. We think employers held up better in Q4 than in Q2, with a better GDP performance, but also with the exit path to a normal economy in sight as China relaxed Covid restrictions. By contrast, in Q2, businesses had great uncertainty about future lockdowns, making planning difficult.Consumption spending on goods improved over the course of Q4, though only in goods, not services. Retail sales rebounded in December, with 5.0% m/m growth, after a 4.1% drop in November. At first glance, this is shocking considering the Covid tsunami sweeping across China. In fact, consumer services did take a massive hit, with catering sales falling 5.3% m/m in December, reversing 0.8% growth in November. This was a comparable drop to April, but nowhere near the collapse in the first Covid outbreak in early 2020.The consumption bounce back, therefore, was entirely driven by goods spending. Retail sales of goods rose 6.6% m/m in December, turning around sharply after a 6.8% fall in November. The leading segment was medicines, rising 30% m/m, up from 0.9%. Sales of autos and mobile phones also posted dramatic bounce backs, after several months of declines. Auto sales were likely boosted by the imminent year-end expiry of the auto purchase tax waiver for traditional engine cars as well as the year-end phasing out of electric vehicle subsidies.Industrial production held up better than market expectations, growing 1.3% y/y in December, down from 2.2% in November. This is a much better situation than the -2.9% drop in April 2022, the low point during the Q2 lockdown. Utilities production was the standout performer, however, rising 7.0% y/y in December, after falling 1.6% in November, probably related to extreme cold weather in certain regions. Manufacturing output barely increased, 0.2% in December, down from 2.0% in November and from a high of 6.4% in September. Domestic spending has held up better than expected in sectors like autos and medicines, but exports are falling at about 10% y/y. Finally, mining production growth slowed slightly to 4.9% from 5.9%.Fixed asset investment in infrastructure and manufacturing have been been the key stimulus channels. Manufacturing investment actually accelerated, to 7.4% y/y in December from 6.2% in November, while infrastructure investment slowed to 10.4% from 13.9%. These are impressive growth rates considering the potential disruption from massive Covid infection numbers. Construction companies have implemented closed-loop systems to prevent transmission. In addition, many builders probably kept operating even if workers had mild infections. The construction activity increase is borne out by m/m rises in construction material production volume for cement, crude steel, pig iron and caustic soda in December, though plain glass output dipped. The weak investment area remained property, with real estate investment plunging 10.0% ytd y/y in December, worsening from a 9.8% drop in November.We think the worst has passed for China’s economy in Q4. The Covid exit wave crested in big cities in December and probably many other regions since then. The billions of trips over the imminent Chinese New Year period is likely to bring secondary waves to largely unscathed rural areas and smaller cities. The economic hit from secondary outbreaks in regions that have already weathered the major exit waves should be smaller considering that immunity levels will be higher among the general population.China’s reopening period is likely to see a moderate economic recovery starting as early as March and from Q2 onwards. We expect the PBoC to cut rates in March or April to boost private-sector demand. The new premier is likely to announce consumption-support measures and incentives for private companies to invest at the National People’s Congress in March. Local governments have issued fairly bullish economic plans for 2023 and, unlike last year, will focus on growth rather than Covid containment. We see this as stepped up targeted support rather than a massive, broad stimulus in the vein of that following the Global Financial Crisis, which drove up debt and resulted in a pre-Covid decade of policy headaches related to financial risk. The chief headwinds for GDP this year are falling exports on soft global demand and the weak property sector which is set for a drawn-out recovery, even with additional support.

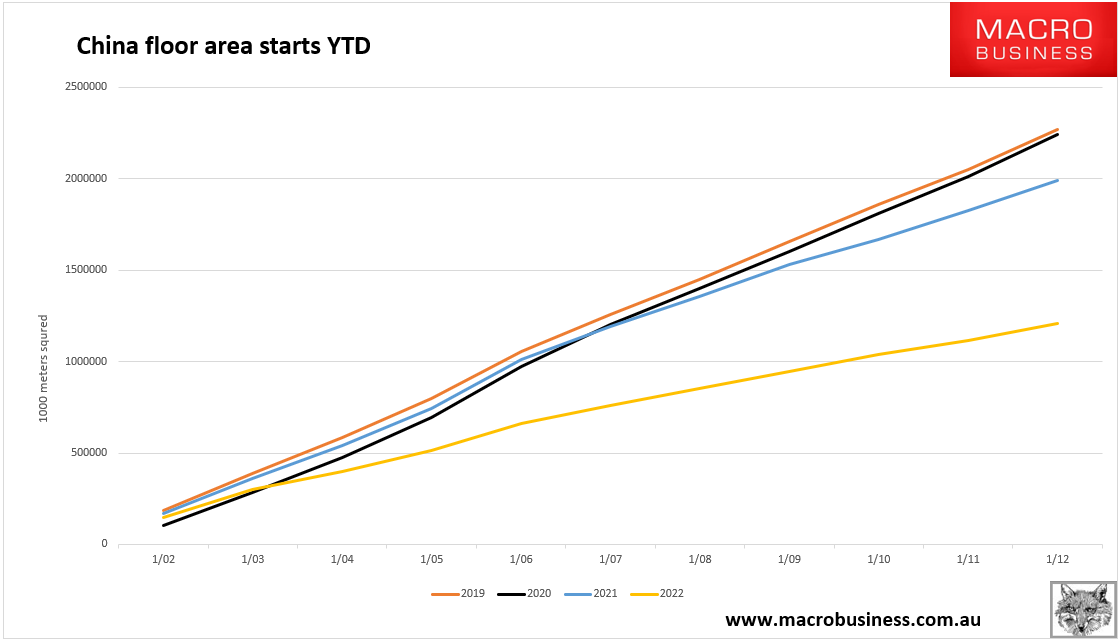

Let’s dig into the commodity-centric data. The property crash is the greatest building bust in global history. Starts were down 47%:

Advertisement