By Gareth Aird and Stephen Wu, economists at CBA:

Key Points:

- We expect the headline CPI to increaseby 1.7%/qtrin Q422 (7.7%/yr).

- The trimmed meanCPI on our forecasts will rise by1.5%/qtr(6.5%/yr).

- An outcome in line with our forecasts for both headline and underlying CPI will see us retain our call for the RBA to raise the cash rate by 25bp at the February Board meeting.

Overview

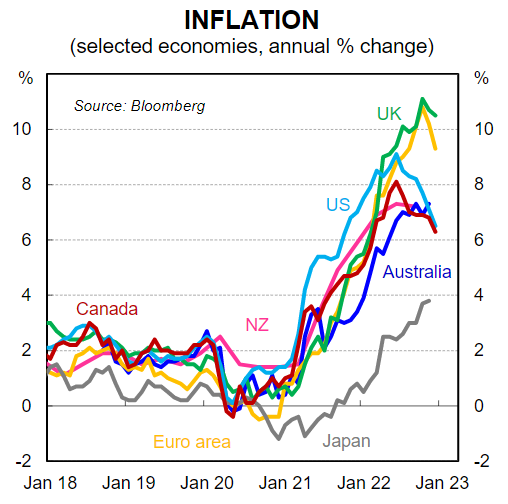

High inflation is the main issue for central banks globally. Most major central banks, including the RBA, have tightened monetary policy swiftly and aggressively in an effort to put downward pressure on aggregate demand and in turn inflation. But monetary policy operates with a lag and inflation takes time to respond to changes in interest rates.

The RBA is currently an inflation fighting central bank having delivered an incredible 300bp of tightening since May 2022. But the RBA became the first major central bank to reduce the size of rate rises to a ‘business as usual’ amount in October when the Board increased the cash rate by 25bp. The Board settled on 25bp because of the risks to global and domestic growth and the potential for inflation to subside quickly. Since then the RBA has increased the cash rate by a further 25bp in both November and December.

We expect inflation pressures to abate relatively swiftly in 2023. But the annual rate still has further to rise and we expect the peak in Q4 22 (i.e. the upcoming quarterly inflation report due to print on 25 January).

We expect this data to show that inflation pressures remained very strong over the December quarter, albeit we think the headline data will not be as strong as the RBA’s implied profile. Notwithstanding, we anticipate thatmonetary policy will be tightened again at the FebruaryBoard meeting. We consider our forecasts for both headline and underlying inflation to be consistent with the RBA increasing the cash rate by 25bp at the FebruaryBoard meeting.But it is not a done deal, particularly as the RBA has indicated they are willing to pause in the tightening cycle.

A brief recap of the Q3 22 inflation data

Inflation surged in Australia over the September quarter, as was widely expected. The headline CPI increased by 1.8%/qtr and the annual rate popped higher to 7.3%. For context the headline CPI also rose by 1.8%/qtr in the June quarter.

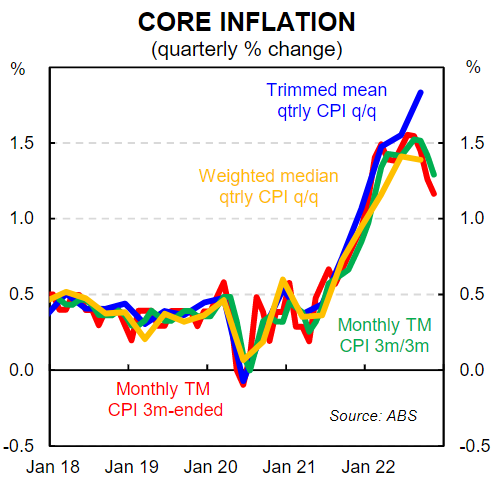

The trimmed mean, the RBA’s preferred measure of underlying inflation, rose by 1.8%/qtr over Q3 22 to sit 6.1% higher through the year. Interestingly, the other measure of underlying inflation, the weighted median, came in at 1.4%/qtr. The annual rate of the weighted median sat at 5.0% in Q3 22, which means there is a large spread between the two measures–this is unusual.

Tradables inflation (i.e. imported inflation) rose by 1.5%/qtr to be 8.7%/yr. A fall in petrol prices kept a lid on tradables inflation over the quarter. Non-tradables prices rose by a stronger 2.0%/qtr to sit 6.5% higher over the year.

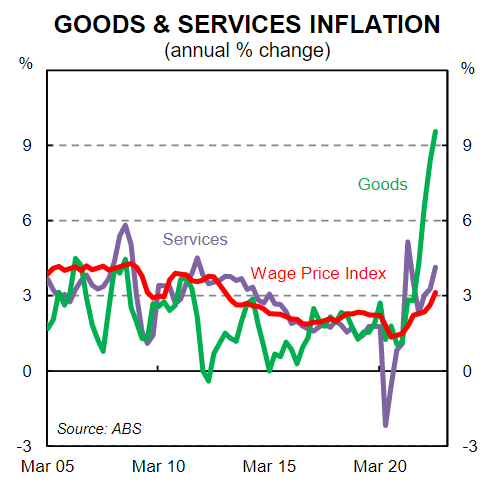

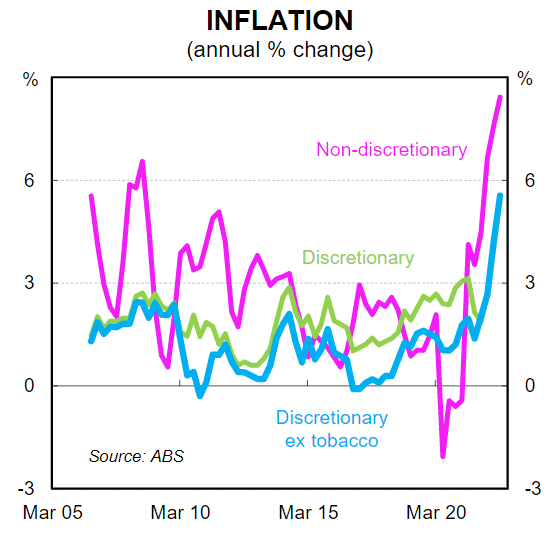

Goods accounted for a little over three quarters of the 7.3% rise in the CPI over the year to Q3 22, reflecting high freight costs, supply constraints and prolonged elevated demand. Goods inflation was 9.6% higher over the year, while services inflation was 4.1% through the year. Services inflation has a strong positive correlation with wages –there is no wage price spiral in Australia like it can be argued is being observed in some other jurisdictions.

What to expect in the Q4 22 CPI

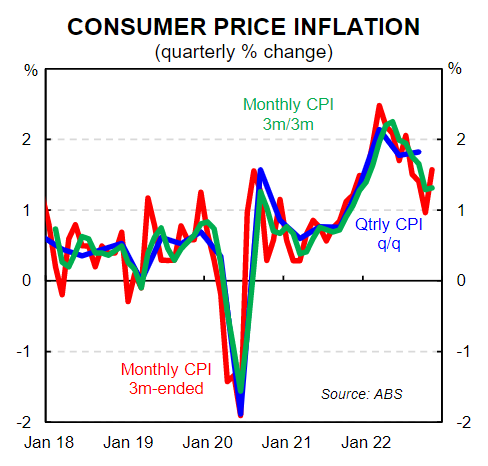

The ABS has already released partial inflation data for the month of October and November by way of the new monthly CPI indicator release. In some respects, these releases should make it easier for economists, including us, to forecast the Q4 22 CPI. Inflation over the year to November 2022 was 7.3%/yr, according to the monthly CPI indicator. But there are some key expected price changes in December to incorporate into our forecast.

Our forecast is for the headline CPI to increase by 1.7% in Q4 22, a decrease from the 1.8% pace in Q3 22. The annual rate would rise to 7.7%/yr, a step up from the 7.3%/yr pace in Q3 22. Underlying or core inflation, as measured by the trimmed mean CPI, is expected to have eased from 1.8%/qtr in Q3 22 to 1.5%/qtr in Q4 22.

Such an outcome would mean that the headline rate of inflation did not accelerate on a quarterly basis. Indeed, we expect core inflation too to have decelerated in Q4 22. The worsening in the annual rates of inflation largely reflects base effects from price increases that occurred earlier in 2022.

To be clear, the expected inflation outcome over Q4 22 is still well above the RBA’s 2-3% inflation target. But the upshot is the worst of the inflation ‘problem’ is likely behind us.

The global picture very much supports this view. Inflation is moderating across many economies, albeit to varying degrees. A key driver has been the retracing of goods inflation, which has been most notable in the US and has occurred to a lesser extent in the UK and the Eurozone. Easing commodity prices from their mid 2022 highs, dissipating supply chain disruptions, and slowing goods demand have been important factors. We expect this dynamic to play out in Australia too.

Offsetting easing goods inflation will likely be a pick-up in services inflation. We anticipate services outpaced goods inflation in Q4 22. The lift in services inflation would be consistent with a continued increase in wages growth, which we expect accelerated to 3.4%/yr in Q4 22. That level of wages growth is consistent with inflation returning to the RBA’s inflation target (annual wages growth with a 3-handle on it is consistent with the inflation target).

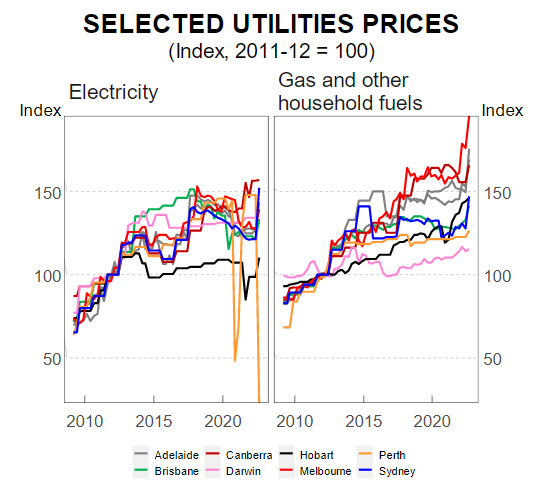

A key source of uncertainty is the extent to which state government electricity rebates have affected measured utility prices. In particular, the WA Government introduced a $A400 household electricity rebate. The measured electricity price rise in Q3 22 was 3.2%. But absent these state and territory government rebates, electricity prices would have risen by 15.6%/qtr. Measured electricity prices in Q4 22 will additionally be affected by the Tasmanian Government’s $A119 Winter Bill Buster discount.

Though there is a lot of uncertainty, we have pencilled in a very large 11% increase in utilities prices. This alone contributes almost 0.5 percentage points to the expected quarterly increase in the CPI. Energy prices and government policies to contain price rises will continue to have an outsized impact on the CPI over this year.

The ABS will also release the December 2022 monthly CPI indicator alongside the Q4 22 CPI. This will take a backseat to the quarterly release, which remains the benchmark measure of inflation in Australia. We expect the monthly headline figure to print a touch stronger than the quarterly figure because of the way the increase in utilities prices is recorded. The monthly CPI will record the price change in the month it is measured, whereas in the quarterly CPI the price will apply for the whole quarter.

The detail

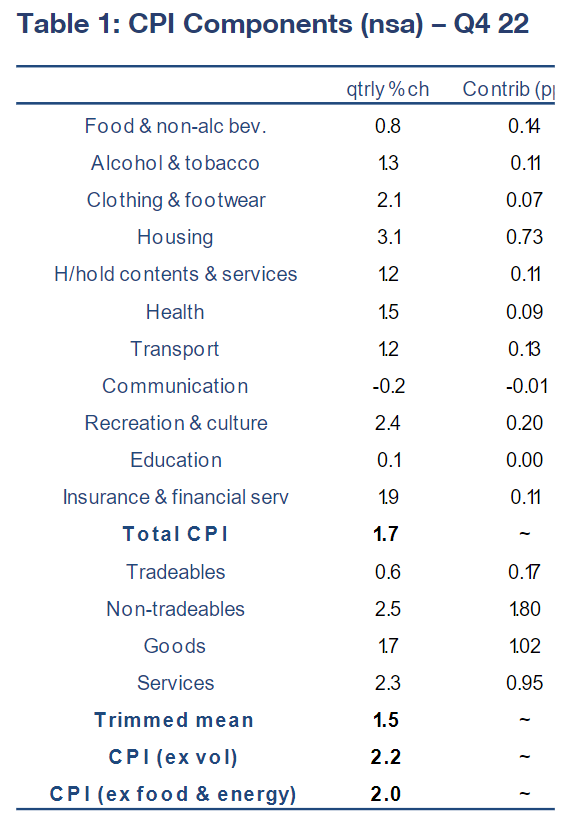

See Table 1 below for our detailed forecasts for the Q4 22 CPI basket. The main features of our call are as follows:

- food inflation steps down to 0.8%, down from the 3.2% increase in the prior quarter largely on the back of increased fruit & vegetable supply that saw prices in September and October;

- clothing & footwear prices rebound after edging lower in Q3 22;

- utilities prices spike higher by 11%/qtr as government rebates in some states delayed the impact of electricity and other household energy price rises to Q4 22;

- rent inflation continues to increase because of very tight rental markets across most capital cities, with the rising flow of net overseas migration adding to housing demand;

- new dwelling purchase inflation moderates further as new building activity slows and supply chain disruptions ease;

- household contents prices decrease by less than the usual Christmas period seasonality, while household services prices rise further;

- petrol prices increase by 2%/qtr, driving a majority of the expected 1.2% increase in transport prices;

- recreation & culture prices lift by 2.4% owing to a big increase in holiday travel & accommodation prices over the final two months of the year; and

- insurance & financial services prices lift by 1.9%.

Overall, our expectation is that goods inflation moderated while a modest increase in services inflation occurred in Q4 22. Fewer and dissipating supply chain disruptions combined with an easing in goods demand will see goods inflation ease. Wages growth owing to still-tight labour markets and a rotation into services consumption will drive a continued lift in services inflation. The 300 basis points of interest rate hikes delivered by the RBA over 2022 will more materially affect demand from here.

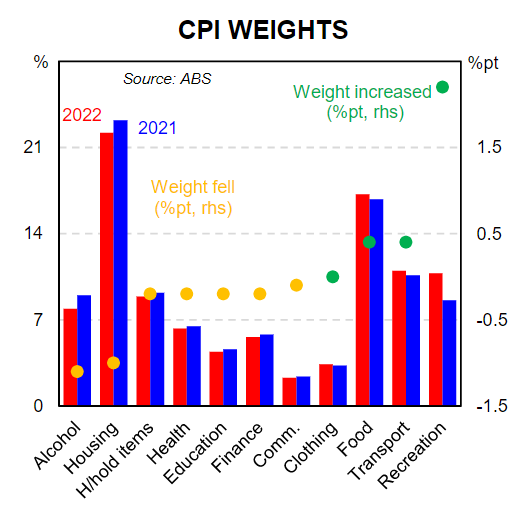

Annual reweight of the CPI

The ABS annually reweights the CPI to ensure the basket remains representative of actual spending patterns by households. The ABS previewed these new weights in the October 2022 monthly CPI indicator release.

There were some large changes in weights between 2021 and 2022 which had a larger than usual impact on the CPI. These shifts in weightings were not surprising given there were long periods of restrictions and lockdowns through 2021 that affected on spending activity.

The largest change was to the recreation and culture group, which increased its weighting by 2.2ppts. The weighting for domestic holiday travel (+0.48ppts) and international holiday travel (+1.77ppts) both increasing significantly as travel resumed post lockdowns. The weighting for alcohol and tobacco fell by 1.1ppts, largely driven by a 0.8ppt fall in the weighting for tobacco. The weighting for tobacco fell because the rate of excise tax has been reduced. The weighting of the housing group was down by 1.0ppts with a smaller weighting for rents and utilities contributing.