I don’t know if the BOJ will ultimately decide to let go of its YCC policy. What I do know is that those arguing it is unsustainable are selling an outrageous lie. After decades of it, it is obviously entirely up to the BOJ where YCC goes – a lesson the cowardly RBA should learn. I have my doubts we’ll see much more reform this year given JPY has ripped higher at astonishing speed, with inflation to crash soon afterward.

Pantheon has more.

- Japan: BoJ Policy Balance Rate was left unchanged at -1.00%. Consensus was -1.00%.

- Japan: BoJ 10 Year Yield Target was left unchanged at 0.00%. Consensus was 0.00%.

Governor Kuroda hints that the BoJ will offer negative rate funds to reinforce YCC effectiveness

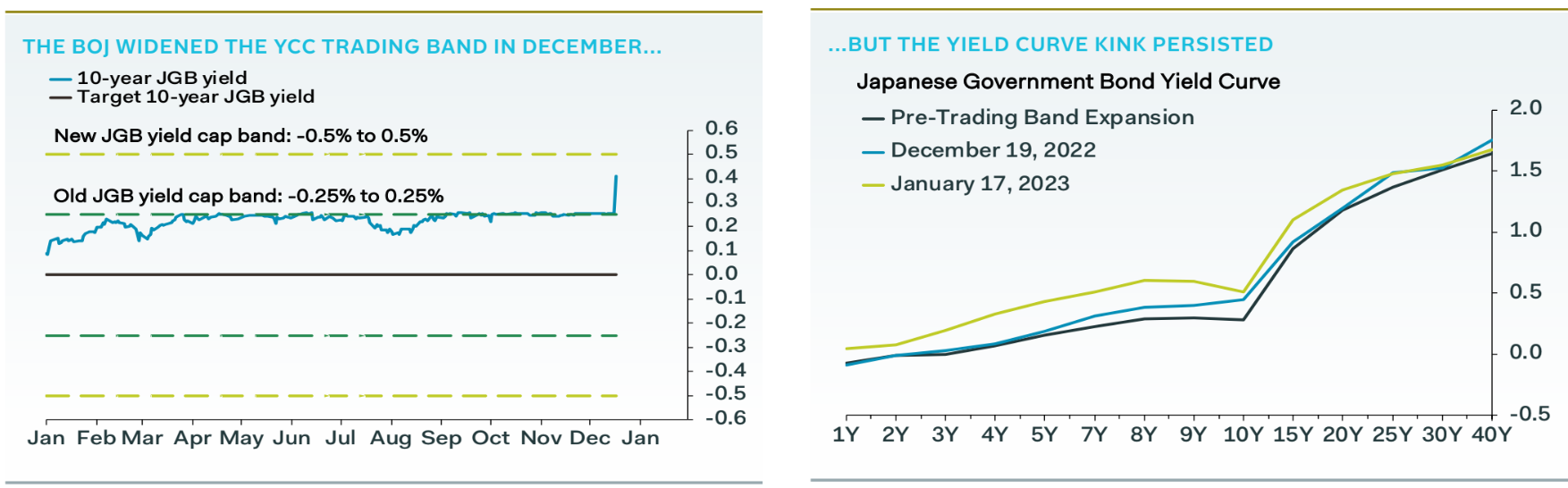

The BoJ refrained from making another adjustment to its yield curve control policy this time, after broadening the trading range for 10-year bond yield around the zero target to 0.5% from 0.25% last month. 10-year yields have traded above the 0.5% ceiling in the four trading sessions leading up to the meeting, indicating strong market bets that the Bank would shift policy and forcing it to buy bonds to defend the target. The BoJ also left the short-term policy balance rate unchanged at -1.0%.

The BoJ’s official reason for widening the trading band last month was to reduce the distortionary effect on financial markets of its yield control curve policy framework. The policy change allowed a 50bp hike in the 10-year bond yield, which should have smoothed out the yield curve kink. But Governor Kuroda today admitted that the improvement in market functioning is not yet clear. The bond market responded to the 50bp 10-year yield increase by driving up yields by 25-to-31bp for bond durations from 6-to-20 years over the last month. Bond yields for all durations except 3 months and 40 years rose over the last month. Governor Kuroda today insisted that no more widening of the yield band is needed, in an effort to establish credibility.

The Bank also responded today with a rule change that should reinforce the effectiveness of its yield control curve policy. Under the previous rule, the BoJ could provide collateralised loans to banks at up to 10 years in duration at a fixed rate, which was 0%. The change allows the Bank now to offer variable rate loans too. This means the BoJ can steer down market rates by offering negative interest rate funds to banks, and Governor Kuroda today hinted that the Bank will make use of this option. In addition, the Bank can offer cheap funds at shorter terms than 10 years, to smooth out the yield curve kink. The current yields for 8-year bonds, at 0.61%, and the 9-year bonds at 0.57%, are both above the 0.5% yield cap for 10-year bonds.

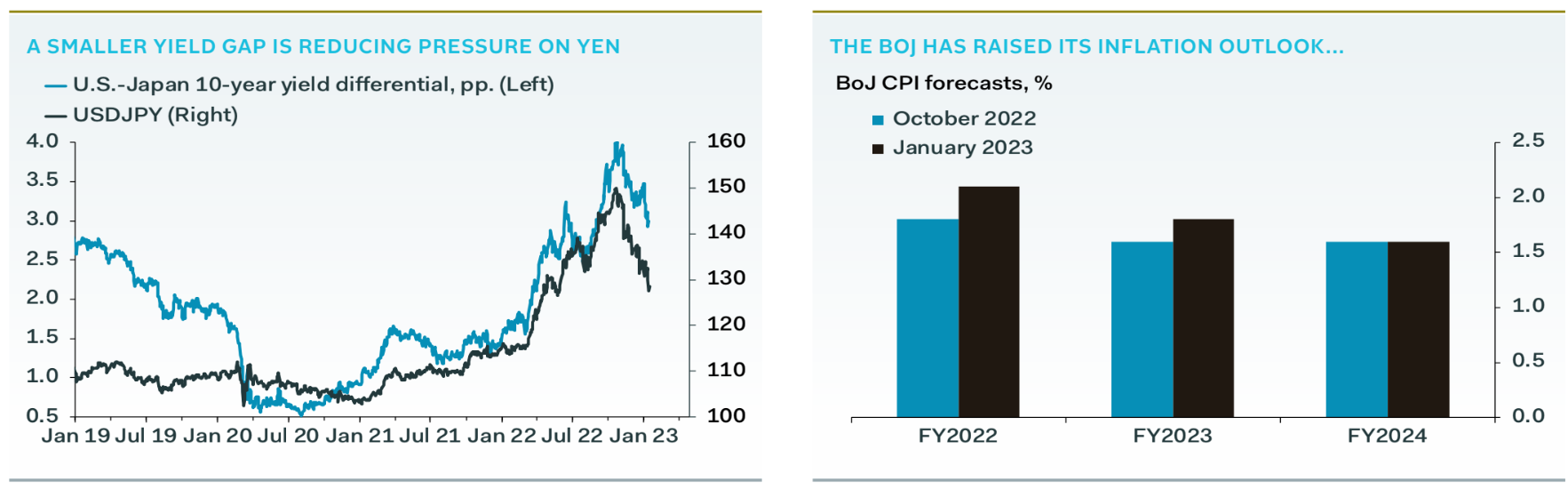

We think the BoJ will remain in a holding pattern at least until the economy recovers, likely later this year. Governor Kuroda said Japan is still in the middle of a pandemic recovery. Both domestic demand and exports are weak, and wage increases have not kept up with consumer inflation. The pressure on the yen has eased, as the broad dollar index has weakened since November, though import inflationary pressure is still driving up consumer inflation. Inflationary expectations are creeping up, and China’s economic reopening should support Japanese economic recovery from March onwards, though against the backdrop of tepid global demand.

Advertisement

The next BoJ meeting in March will be Governor Kuroda’s last one, and likely candidates for his successor have been careful not to indicate policy preferences in public. On balance, we still think that the underlying economy is relatively weak, and a rate hike is unlikely this year.

Advertisement