With the Australian dollar surging nearly 15% higher against the USD in the last three months, there’s been a lot of spin and gabbing over the Pacific Peso turning into a “safe haven” against the US economy, or alluding to the economic strength down under recently.

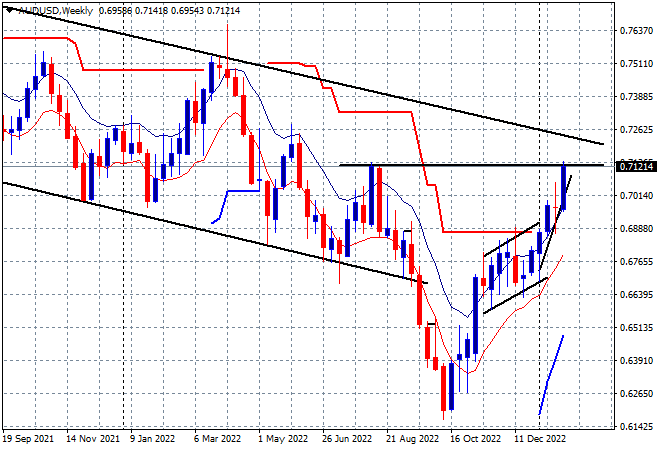

Once you take a step back away from short term charts and look at a weekly view going back a year or more, the notion that the Australian dollar is powering ahead is very questionable:

Current price action should be seen as an extreme swing from the October 2022 lows, which were equally extreme in lobbing below the monthly downtrend channel from the post COVID highs. The Australian dollar has passed through the midzone of that channel around the 69 handle and may yet move higher to touch or push through the upper zone at the 72 cent level in the coming weeks, as traders bet on a more hawkish RBA in February.

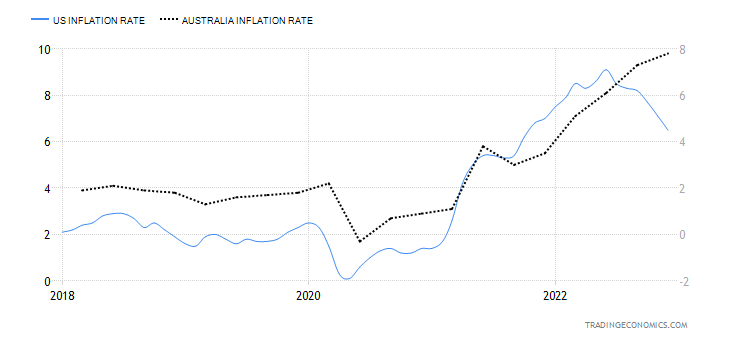

And indeed, the current weekly price action does indicate a nascent bullish inverted head and shoulders pattern with the neckline fast approaching. But that’s the problem – its too fast approaching, as this recent trend has accelerated far too fast on the recent nexus between inflation seemingly peaking in the US and not slowing down in Australia:

The US Federal Reserve is meeting next Wednesday, with the RBA not adjourning until the following week (after a very long holiday) with the all important US jobs data in between and the next inflation print shortly thereafter. If the following monthly CPI print from the ABS shows any slowing down of inflation locally post a 25-50bps rise by the RBA that has already been cooked into recent price action, expect sharp falls and a reversion to the mean monthly downtrend.