Australia, we have a rent inflation problem

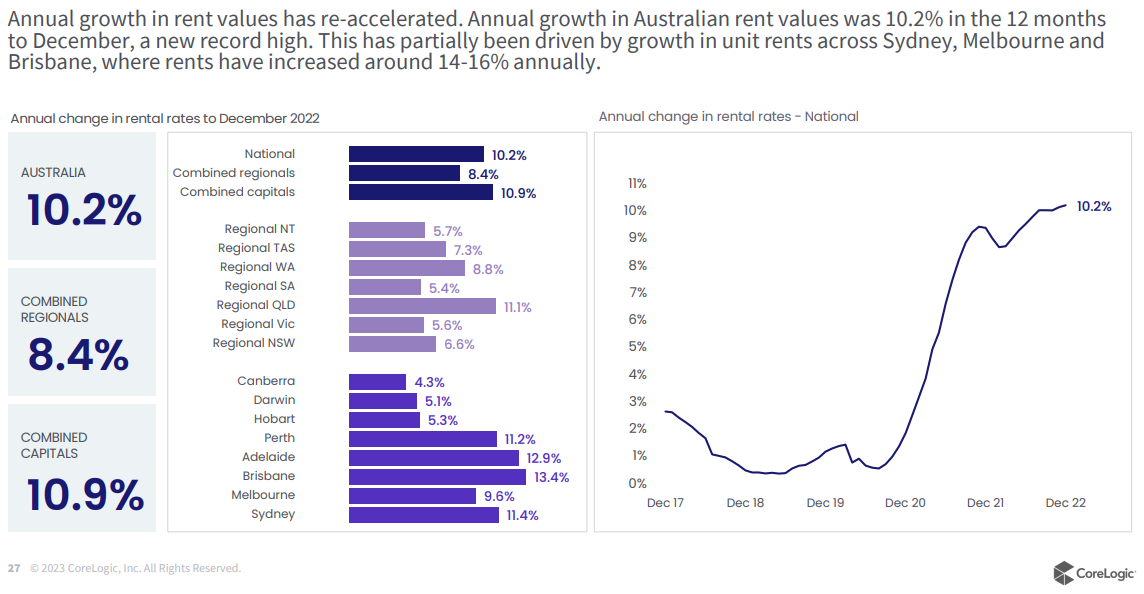

CoreLogic’s latest monthly chart pack shows that “annual growth in rent values has re-accelerated” with rents nationally up “10.2% in the 12 months to December, a new record high”, driven in part by “growth in unit rents across Sydney, Melbourne and Brisbane, where rents have increased around 14-16% annually”:

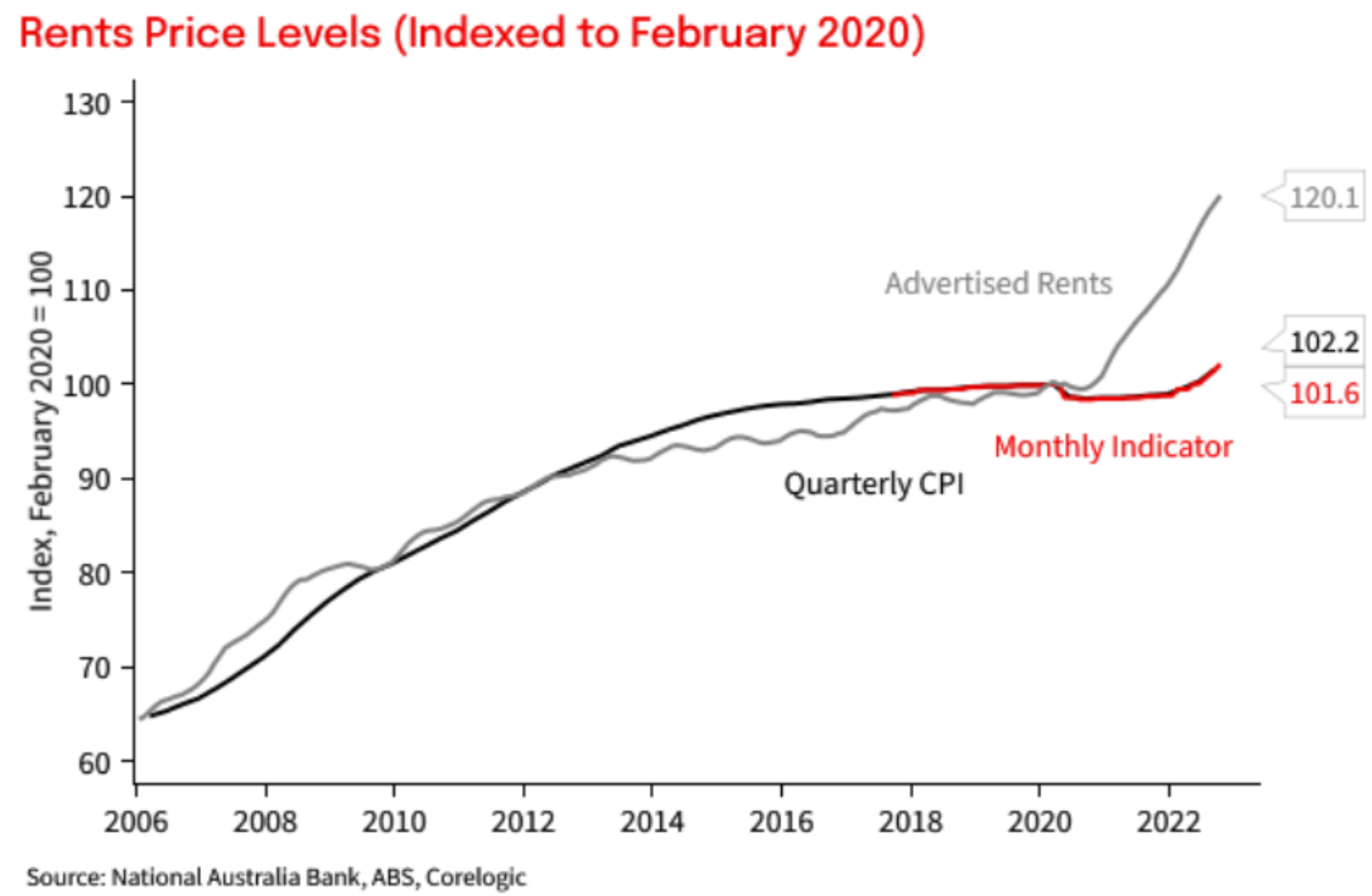

The record increase in advertised rents comes at the same time as the Australian Bureau of Statistics’ (ABS) monthly CPI indicator reported only 3.6% year-on-year rental growth, which was less than half the 7.3% headline rate of inflation recorded in the year to December 2022.

As shown below by independent journalist and economist Tarric Brooker, the gap between advertised rents (as reported by private data providers like CoreLogic) and wider rents (as reported by the ABS) has hit a record wide margin:

This means that Australia could be looking at years of high rental inflation as the wider ABS rental series gradually adjusts upwards to meet the higher new advertised rents hitting the market.

As explained by the ABS, its rental series “is updated monthly and includes approximately 480,000 rental properties that are used to produce the CPI Rents series across all capital cities”.

The ABS’ rental series measures “the current ‘price’ being paid by all types of households that rent including new and existing renters”. It differs from private “measures of rental inflation that are based on newly advertised rental properties only measure changes in the asking or advertised price of rental properties for new tenancies”.

“At any given time, newly advertised tenancies represent a relatively small proportion of properties being rented in Australia”, according to the ABS. “Advertised rents tend to reflect the dynamic end of the rental market where the price change for new tenancies can be more volatile than that being experienced by renters with existing tenancy agreements”.

This means that “price changes observed in advertised rents series are expected to eventually flow through to the CPI Rents series. However, the small share of rental properties leased to new tenants each quarter means that it takes some time for changes in advertised rents to impact price change observed in the CPI Rents series”.

In short, Australia is facing a rental inflation shock in 2023 as the CPI rental series catches up with the already recorded hyper growth in advertised rents.

Other things equal, this will pressure the Reserve Bank to hike interest rates further, or at least keep rates on hold for longer (rather than cutting).