According to ANZ’s latest Property Focus, New Zealand’s house price crash is around two-thirds of the way through ANZ’s forecast 22% peak-to-trough decline.

Ongoing falls in house prices are expected as “supply and demand dynamics continue to swing in favour of buyers”.

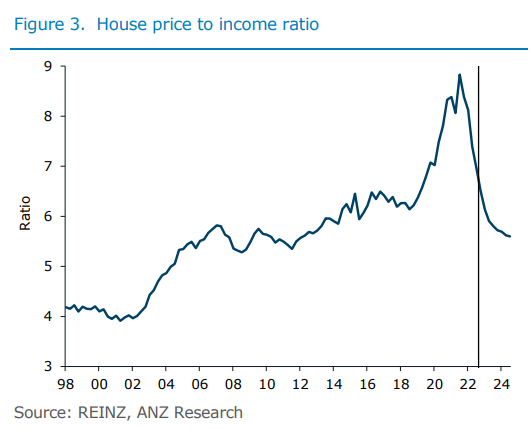

Housing affordability, as measured by the house price to income ratio, is also forecast to improve to around 2013 levels; although the sharp rise in mortgage rates will blunt the benefit for many home buyers.

____________________________________________________________________________________________

The REINZ HPI shows house prices finished 2022 around 15% below their November 2021 peak – that’s 13 months of back-to-back declines, putting the market around two thirds of the way through our forecast for a 22% peak to trough decline. We’re comfortable that risks around our forecast are fairly balanced, but as we note in our feature article, 2023 still has plenty of potential to throw us a few curve balls.

The December housing data certainly suggested more price declines are looming as 2023 gets underway.

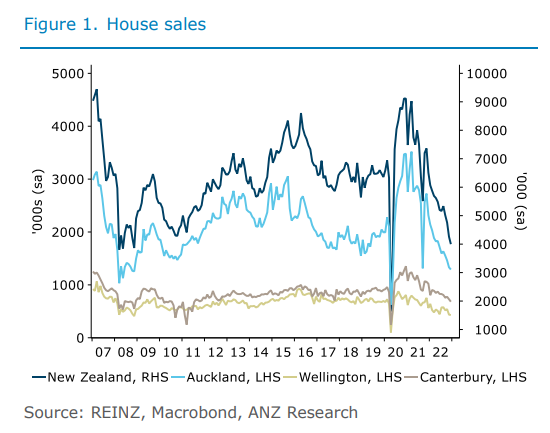

House sales, which tend to lead prices by a few months, fell 6.2% m/m, with the trend still clearly southbound.

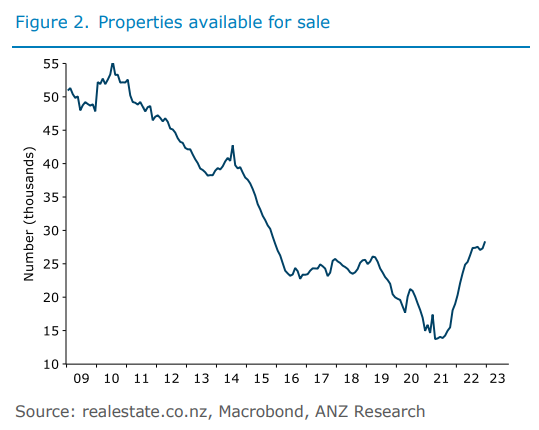

As sales fall, the number of properties available for sale continues to rise, meaning greater competition for those selling, and more options for those looking to buy.

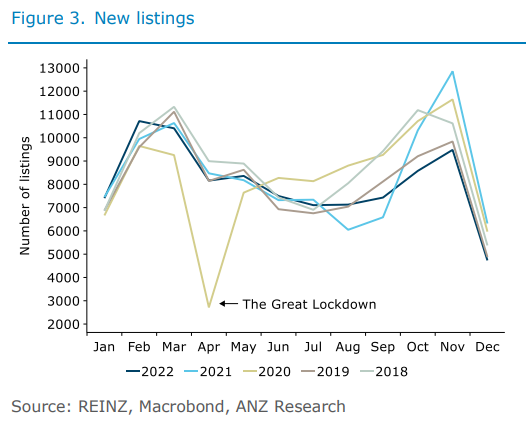

This lift in available properties for sale comes even as new listings over the spring/summer period has so far undershot the past few years.

All in all, the December housing data was practically a straight flush when it comes to the housing market pulse: momentum is still softening. Given the direction of travel in mortgage rates these past few months, that should hardly come as a surprise…

But in the absence of a material pick-up in forced house sales, we’re hopeful that the correction underway will remain relatively orderly. Indeed, with prices down just 15% so far, we’re still very much in the soft-landing zone given prices lifted more than 45% in the wake of the pandemic stimulus…

Clearly, higher mortgage rates are dampening demand for housing, and as OCR hikes come to an end over the coming months (which is very dependent on the inflation outlook), this driver of downside momentum is expected to dissipate. Thereafter, the health of the household sector will determine if the housing downswing still has further to go or if it’s finally petering out – our forecast assumes the market finds a floor in the second half of 2023…

Falling house prices mean housing affordability is improving. But if our forecast for a 22% peak to trough decline in house prices is correct, affordability, as measured by house prices relative to incomes, won’t be anything to write home about any time soon.

On our outlook, house prices relative to household incomes are expected to improve (fall) beyond the levels that prevailed just before the pandemic, but not meaningfully (figure 3). In an absolute sense, this ratio is still high, and that means there are many kiwis who will still be locked out of the market.