I’m not sure where they find their press-release recyclers these days, but the worst paper in Australia is busy today creating a panic where there is none:

Home loan borrowers face the threat mortgage rates will rise by even more than official increases this year, as funding costs soar and banks repay $188 billion of emergency money borrowed from the Reserve Bank during the pandemic.

Smaller non-bank lenders have already increased variable mortgage rates more than the central bank’s 3 percentage points of rate rises since last May – passing on up to 20 per cent more each month – while some, including Nano Home Loans and Volt Bank, have been forced to stop writing new loans or close altogether.

Judo Bank boss and former National Australia Bank executive Joseph Healy said the big banks could be forced to follow suit this year.

“The major banks will have to protect the margins because otherwise the investor community gets very upset,” Mr Healy said.

“I think out-of-cycle interest rate increases are not something that should be discounted in the world that we’re in – or heading into – because the banks’ cost of funds will start to rise and particularly deposit funds, given the demand that’s going to be on funding sources to replace the TFF [Term Funding Facility provided by the RBA].”

…the cost to big banks for borrowing money on international markets has jumped by almost 1 percentage point above the benchmark bank bill swap rate since 12 months ago, excluding the general increase in interest rates caused by central banks.

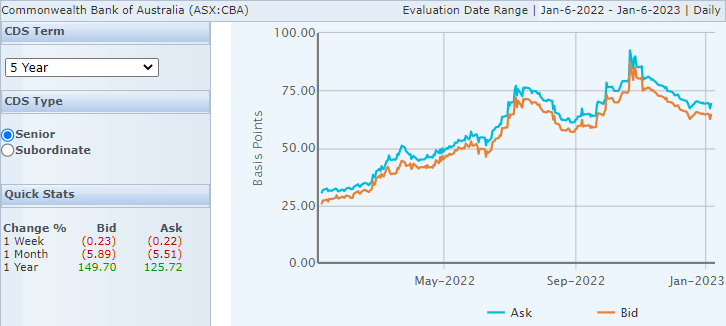

Well, yeh? But if we consult the chart we can see that funding margins have been materially compressing for the last quarter and haven’t moved in nine months:

These are not especially wide spreads. Interbank rates are calm as well.

It is true that free money from the RBA will have to be refinanced but there is 3% of new margin in the rate hike cycle to do so. Credit demand is falling fast so there will not be any pressing need to raise funds from that front. The same goes for deposits which are flowing nicely amid household anxiety about asset markets.

Aside from anything else, any move to hike out-of-cycle by the banks will, I suspect, be greeted negatively by the equity market as its worries turn swiftly from margins towards bad debts while the fixed rate reset smashes into the economy.

For that matter, any out-of-cycle moves will be factored into RBA cash rate moves anyway.

Yes, the RBA’s overly aggressive tightening and fixed rate reset steamroller are coming to crush consumption and I expect house prices to keep on falling to boot. This might result in funding cost pressures for the banks if it is mismanaged. But, for now, that is not something to worry about.

The mind boggles a bit when we consider that just one month ago this same paper fought tooth and nail against the energy price caps without which mortgage rates would skyrocket to 10%!

It appears whichever interest was last on the blower sets the editorial direction for the AFR.