TD Securities with the note:

Key Points:

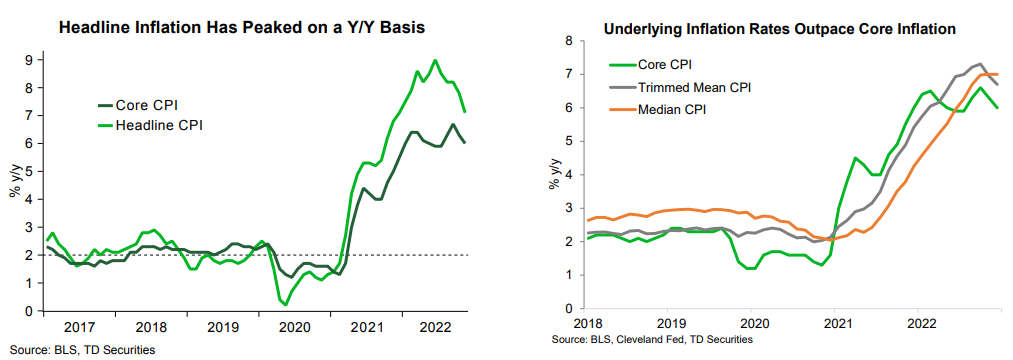

- The 2022 inflation surge in the US was widespread not only in headline and core inflation, but also was reflected in proxies for underlying inflation rates. While core goods inflation slowed toward the end of 2022, core services inflation remains persistently strong, keeping core inflation elevated.

- Wages have caught up with higher household inflation expectations. We believe that wages will cause services sector prices to keep rising at an elevated pace. We use a Phillips curve framework to interpret the recent inflation moves and show that labor market tightness has become a dominant driver behind elevated core and core services inflation. This will happen despite a gradual slowing of the labor market next year.

- Therefore, as long as labor markets remain tight, core services inflation will keep US inflation sticky at elevated levels and slow the pace of disinflation in 2023. These insights are reflected in our inflation forecasts, where both core CPI inflation and core PCE inflation will remain above target inflation levels by the end of 2023.

A Long Way From Normal

The 2022 inflation surge in the US was widespread not only in headline and core inflation, but was also reflected in proxies for underlying inflation rates. Even with core inflation possibly peaking recently, these underlying measures continue to outpace core inflation, indicating that inflationary pressures remain elevated.

Advertisement