Will Aussie house prices rebound in 2023?

According to InvestorKit data expert, Arjun Paliwal, Australian house prices could begin to rise as soon as April 2023 due to a rental crisis and, in the case of New South Wales, changes to stamp duty that will improve borrowing capacity and push more first home buyers into the market.

Paliwal believes that limited housing supply would combine with the increase in buyer demand to push up home prices.

“We are seeing roughly the same number of listings for sale as 12 years ago, which is concerning. This supply and demand is what will ultimately drive-up house prices”, Paliwal said.

Paliwal also believes the rising cost of rent could push more people to consider buying while prices are down.

“There comes a time when people see value. I feel that point in time will be next year”, Paliwal said.

“Interest rates could soon hold steady while the 3% assessment buffer used by banks could potentially be wound back. That would enable more borrowers to pull the trigger on their purchases”.

“I feel the biggest increase in interest rates are possibly behind us, especially as we saw the trend of increase change from 0.5% to 0.25%”.

Paliwal has tipped house prices to rise between 5% to 8% in Sydney next year, but said a further softening is likely to occur beforehand.

I agree with Paliwal that Australian house prices should begin to rebound in 2023. However, I do not expect this rebound to occur until the fourth quarter after the Reserve Bank of Australia (RBA) begins cutting interest rates.

I also believe that Australian and Sydney house prices will end the 2023 calendar year deep in negative territory, with losses over the first three quarters far outweighing any small rises at the end of the year.

The biggest driver of house prices over the short-term is the cost of debt (interest rates) and borrowing capacity.

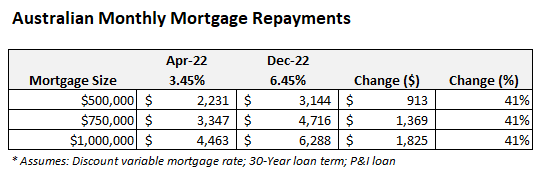

The RBA’s 3.0% of monetary tightening will already have increased variable mortgage repayments by 41% once the rate hikes are fully passed onto borrowers in the new year:

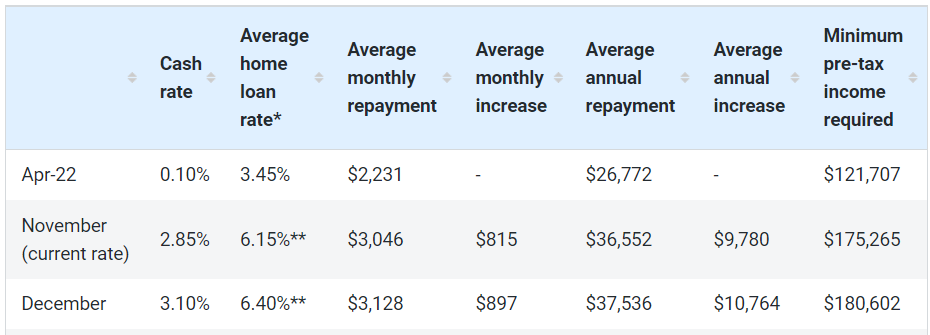

Moreover, according to Finder, the amount of pre-tax income required to service a $500,000 variable rate mortgage has soared from around $121,000 in April 2022 to $181,000 as at December, following the RBA’s 3.0% of rate hikes:

Given most economists and financial markets are expecting further rate hikes early in the new year, mortgage repayments will inevitably rise further, shrinking borrowing capacity. And this will shunt house prices lower.

There is also the risk that the fixed rate mortgage reset, which will see nearly one-in-four mortgages (by value) in 2023 switch from rock bottom 2% fixed mortgage rates to 5% to 6% rates, will cause significant numbers of forced sales, pushing house prices lower.

While these conditions are present, it is premature to talk of a house price rebound in early 2023.

That said, Paliwal does make a good point about a possible wind-back of the 3% mortgage assessment buffer. Will APRA step in to save house prices by cutting the buffer to lift borrowing capacity? I wouldn’t put it past them.